Direct Answer

Payment orchestration is a software layer that connects several payment providers—gateways, processors, acquirers, and payment methods—behind a single integration, then decides how each transaction is processed. Instead of building and maintaining a separate connection to every provider, a payment team integrates once and manages routing, failed-payment retries, and reconciliation from one place.

Payment orchestration is a software layer that connects several payment providers—gateways, processors, acquirers, and payment methods—behind a single integration, then coordinates how each transaction is processed.

Instead of building and maintaining a separate connection to every provider, a payment team can manage routing, order status, reconciliation, and, where supported by the provider, failed-payment retry through one technical layer.

This guide explains what payment orchestration does, where it helps, where it adds unnecessary complexity, and what payment leads, PSP evaluators, and engineers should examine before choosing a provider.

What Is Payment Orchestration?

Payment orchestration is the practice of coordinating multiple payment providers through one technical layer rather than connecting every provider directly to the checkout.

In practical terms, it is the difference between maintaining several independent integrations and maintaining one integration that communicates with several providers on your behalf.

The orchestration layer sits between the merchant application and the providers that process or move money. It can:

- Standardize payment requests.

- Determine which provider or route should handle a transaction.

- Normalize authorization and decline responses.

- Synchronize order status.

- Collect transaction and settlement data.

- Support reconciliation across different provider formats.

The purpose of orchestration is not to replace acquirers, processors, or gateways. Its purpose is to coordinate them.

Businesses rarely adopt orchestration because of one isolated feature. They usually reach a tipping point.

A merchant using one provider in one market may not need an additional layer. The same merchant may later operate across several markets, use multiple payment methods, maintain several provider integrations, and reconcile different reports manually. At that stage, provider management becomes an operational problem in its own right.

Payment orchestration is designed to address that provider sprawl.

It is also important to distinguish orchestration from a payment aggregator. An aggregator generally enables merchants to accept payments within the aggregator’s own commercial and technical setup. An orchestration layer coordinates several payment connections, methods, or processing paths.

A merchant can use an aggregator and still develop an orchestration problem after adding another provider or payment route.

How Payment Orchestration Works

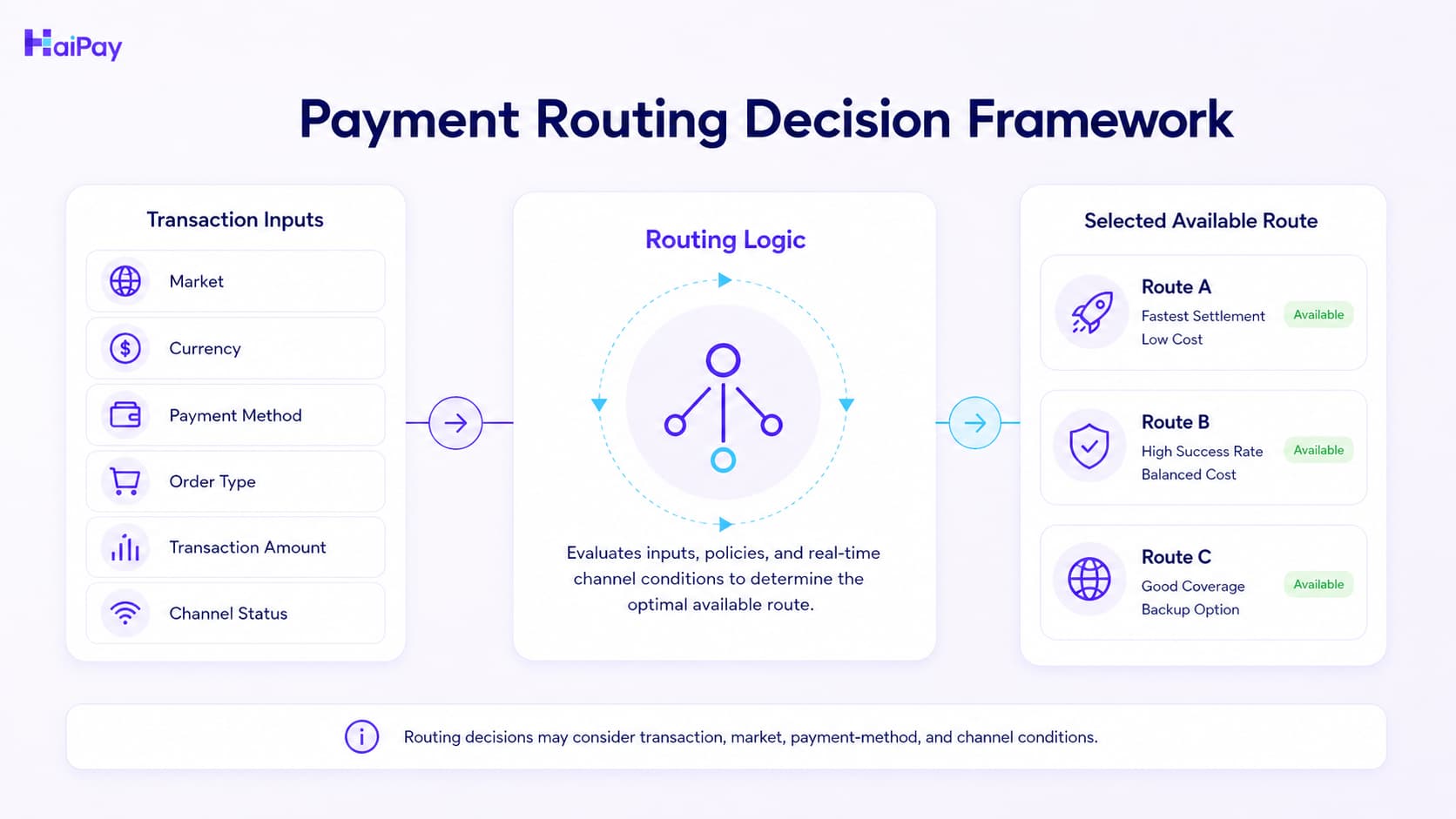

A payment orchestration flow can be understood through three core stages—route, process, and reconcile. Some providers also support failed-payment retry as an optional capability.

1. Route

The orchestration layer determines which available provider or payment path should handle the transaction.

Routing decisions may consider factors such as:

- Customer market.

- Transaction currency.

- Payment method.

- Order type.

- Transaction amount.

- Provider or channel status.

- Merchant-defined or provider-managed routing logic.

The objective is to send the transaction through an appropriate available path rather than directing every payment to one fixed connection.

2. Process

The selected provider authorizes and, where applicable, captures the payment.

The orchestration layer sends the payment request in a standardized structure and translates the provider’s response into a format the merchant’s application can understand consistently.

This normalization matters because providers may use different:

- Request fields.

- Response codes.

- Status definitions.

- Refund processes.

- Settlement formats.

Without normalization, each new provider can create additional engineering and operational work.

3. Retry Where Supported

Some orchestration providers can re-attempt an eligible failed payment under configured conditions. This is a provider-dependent capability, not a universal feature.

Retry is also different from automatic failover. Retry creates another payment attempt under defined conditions, while automatic failover reroutes a transaction when a provider or channel is unavailable.

Where retry is supported, a safe policy should define:

- Which failure reasons are eligible.

- How many attempts are permitted.

- How long to wait between attempts.

- How duplicate charges are prevented.

- How the customer is informed.

- How the final order state is synchronized.

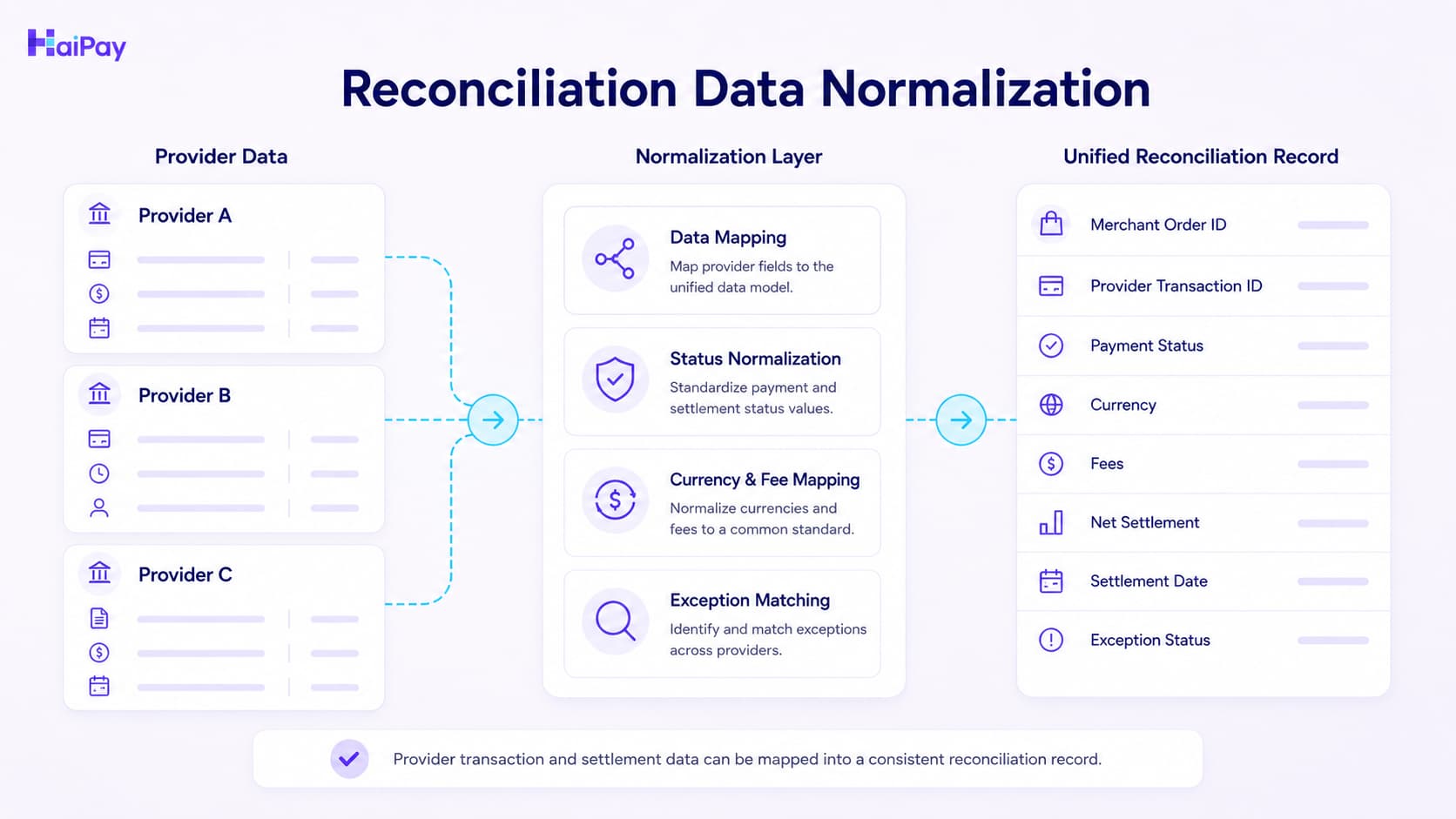

4. Reconcile

After processing, the orchestration layer collects and normalizes transaction, refund, fee, and settlement information.

This gives finance and operations teams a more consistent record across different providers.

Reconciliation is where payment activity, order records, and settlement data are matched so that the business can explain what happened to each transaction.

Order-status synchronization runs alongside the core payment flow. As a payment moves through authorization, capture, refund, or dispute, the merchant’s system needs to remain aligned with the provider’s record.

Where retry is supported, retry attempts and their final outcome should also be synchronized.

Consider a customer paying with a local card.

The orchestration layer first selects a route based on the market, currency, payment method, and applicable routing logic. The selected provider processes the authorization.

The outcome—captured, declined, or refunded later—is synchronized with the merchant’s order system and included in the reconciliation record.

The value comes from managing the complete sequence through one coordinated layer.

Payment Orchestration vs Gateway vs PSP vs Acquirer

Payment orchestration, payment gateways, payment service providers, and acquirers are often discussed as though they perform the same role. In practice, they address different parts of the payment stack.

The terminology is not always rigid. The PCI Security Standards Council glossary treats terms such as payment service provider, payment gateway, and payment processor as overlapping in some contexts.

The distinctions below reflect how the roles are commonly separated in commercial and technical payment discussions.

Role | How It Is Commonly Described | Where the Role Usually Stops |

|---|---|---|

Acquirer or acquiring bank | An entity designated by a payment brand or card network to process card transactions for merchants | Does not, by itself, coordinate routing across several independent providers |

Payment Service Provider (PSP) | Enables merchants to accept payments and may combine gateway, processing, acquiring, or payment-method access | One PSP connection does not automatically provide multi-provider management |

Payment gateway | Transmits payment data between the checkout and a processor or acquirer | Does not necessarily decide between several providers or normalize all provider records |

Payment orchestration | Coordinates multiple gateways, PSPs, acquirers, or payment methods through one integration | Is not necessarily the entity that acquires or settles the underlying transaction |

The practical distinction is that orchestration operates as a coordination layer over payment providers.

For example, a service that enables a merchant to accept payments may be acting as a PSP. An orchestration layer becomes relevant when the merchant has several such services or payment paths and needs to manage them together.

The buying decision changes depending on the problem:

- If the business needs a way to accept payments, it may need a PSP, gateway, or acquirer.

- If the business already has several ways to accept payments and cannot manage them efficiently, it may need orchestration.

Adding another PSP to solve a provider-management problem can simply create another integration that needs to be maintained.

Benefits of Payment Orchestration

The value of orchestration should be connected to specific operational mechanisms rather than broad promises.

One Integration Instead of Many

A standardized orchestration integration can reduce the need to build a separate technical connection for every payment provider.

This becomes valuable when adding a provider currently requires:

- New API development.

- Additional checkout logic.

- New status mappings.

- Separate refund handling.

- Independent reporting work.

- Ongoing provider-specific maintenance.

The main benefit is reduced duplication across integrations, not the elimination of all integration work.

Payment Routing

Rules can direct a transaction down a path suited to its market, currency, payment method, order type, amount, or channel conditions, rather than sending every transaction to one fixed provider.

Routing control models differ between providers. Some platforms allow merchants to configure and edit routing rules directly. Other services, including HaiPay, use a managed model in which routing logic is maintained through the provider’s backend.

Businesses should confirm:

- Which factors influence routing.

- Who controls routing changes.

- Whether the merchant can edit rules directly.

- How routing decisions can be reviewed.

- How exceptions and incidents are handled.

Failed-Payment Retry Where Supported

Some orchestration providers can re-attempt eligible failed payments under defined rules. This is a provider-dependent capability, not a default feature, and retry is not the same as automatic failover.

Where retry is available, the provider should clearly define eligible failure reasons, attempt limits, duplicate-payment controls, and final order-status handling.

When a transaction fails, the failed result is returned to the merchant.

Normalized Reporting

Different providers may produce different transaction IDs, status names, settlement files, and fee structures.

Normalization creates a more consistent data model across providers, reducing the amount of manual stitching required by finance and operations teams.

A strong practical signal is the month-end close process. If closing the books depends on exporting several reports and manually matching them, normalized reconciliation may deliver meaningful operational value.

Local Payment Reach

Customers in different markets do not always use the same payment methods.

An orchestration or multi-provider setup can make it easier to combine:

- International cards.

- Local card networks.

- Digital wallets.

- Bank transfers.

- Real-time payment methods.

- Other market-specific payment options.

This does not mean that a long payment-method list is automatically valuable. The available methods still need to match the merchant’s actual markets and customer behavior.

Operational Visibility

A coordinated payment layer can also make transaction monitoring more consistent.

Payment, product, technical, and finance teams may gain a shared view of:

- Transaction outcomes.

- Provider responses.

- Retry activity, where supported.

- Order status.

- Refund status.

- Reconciliation exceptions.

Payment orchestration is sometimes described as a payment optimization tool. It can contribute to optimization, but it does not guarantee a specific approval-rate, conversion-rate, or cost improvement.

Any performance claim should be supported by merchant-specific measurement.

Intelligent Payment Routing

Routing is usually the most visible element of payment orchestration.

Instead of sending every transaction through one fixed provider, the system selects a route based on relevant transaction and business conditions.

Common routing dimensions include:

- Geographic routing: selecting a route suited to the customer’s country or region.

- Currency routing: directing transactions according to the transaction or settlement currency.

- Payment-method routing: sending a local payment method to a provider that supports it.

- Order-type routing: using different paths for different products, transaction types, or merchant use cases.

- Amount-based routing: applying different routes to different transaction values.

- Channel-status routing: considering the operational status of an available payment channel.

Routing models vary across providers.

Some orchestration platforms allow merchants to build and edit routing rules directly. Managed-routing services may operate the logic on the merchant’s behalf. Neither model is automatically right for every business.

The evaluation should focus on:

- How routing factors are selected.

- How much control the merchant needs.

- Whether decisions can be explained.

- How routing changes are approved.

- How routing performance is reviewed.

More routing rules do not automatically produce better results. Every additional rule must be maintained, tested, and understood.

The goal is to use the smallest set of routing logic that solves the business problem clearly and reliably.

How HaiPay Handles Routing

HaiPay uses a managed, backend-controlled automatic routing model. Payment paths are selected based on factors including:

- Order type.

- Transaction amount.

- Customer region.

- Channel status.

Routing logic is maintained by HaiPay rather than configured through a merchant-facing rules engine. Merchants integrate through HaiPay’s APIs and review transaction and reporting data through the HaiPay dashboard.

This model reduces the need for merchants to build and operate their own routing infrastructure. However, it does not provide merchant-side rule editing.

Businesses evaluating how routing fits into their payment architecture can also review HaiPay’s local and global acquiring overview.

For a deeper look at how routing decisions and the main routing strategies work, see our companion article on how intelligent payment routing works.

Recovering Failed Payments: Retry Across the Industry

Failed and declined payments are a normal part of online payments, but providers handle them differently.

Some orchestration platforms offer rule-based retry, which re-attempts an eligible failed payment under defined conditions. Where retry is offered, the rules matter: some declines are permanent, and retrying them carelessly can create duplicate charges, unnecessary processing, or customer frustration.

A controlled retry policy should define:

- Eligible decline reasons.

- Maximum attempt counts.

- Intervals between attempts.

- Duplicate-payment controls.

- Customer notification rules.

- Final order-status handling.

Retry is not the same as automatic failover.

Retry creates another payment attempt under defined conditions. Automatic failover reroutes a transaction when a provider or channel becomes unavailable. These are separate capabilities and should be evaluated separately.

HaiPay’s Current Handling

HaiPay currently does not automatically initiate failed-payment retries and does not provide automatic failover. When a transaction fails, the failed result is returned directly to the merchant.

Order-status synchronization remains important even without platform-initiated retry because the merchant and provider still need a consistent final state for authorization, capture, refund, and dispute handling.

If retry or automatic failover is a hard requirement, confirm the intended handling during solution design rather than assume that either capability is built into the platform.

Reconciliation, Settlement, and Multi-Currency Management

When several providers each produce their own transaction and settlement records, finance teams may need to export reports, match transactions, identify fee differences, and investigate exceptions manually.

The reconciliation role of an orchestration layer is to collect and normalize those records so the finance team can work from a more consistent data structure.

Relevant data may include:

- Merchant order ID.

- Provider transaction ID.

- Authorization status.

- Captured amount.

- Refunded amount.

- Provider fees.

- Settlement currency.

- Settlement amount.

- Settlement date.

- Dispute status.

- Reconciliation exception.

Multi-currency settlement adds another layer of complexity.

A merchant collecting payments in several markets may need to manage multiple transaction currencies, settlement currencies, conversion records, and provider statements.

The practical objective is not merely to support several currencies. It is to make the resulting financial records understandable and manageable.

A common operational warning sign is when the month-end close depends on one person who knows how to match several provider exports manually.

HaiPay provides automated reconciliation and multi-currency settlement capabilities as part of its payment offering.

Local Payment Methods and Localized Risk

Market differences extend beyond currency.

Customers in different countries and regions may prefer different:

- Card networks.

- Digital wallets.

- Bank-transfer methods.

- Real-time payment systems.

- Cash-based or voucher payment options.

- Authentication experiences.

A checkout that offers only one global payment method may exclude customers who do not have access to it, do not trust it, or do not normally use it.

Risk behavior also varies by market.

A fraud signal that is highly predictive in one market may create unnecessary false declines in another. Local issuer behavior, device patterns, authentication practices, payment methods, and customer habits can all affect the result.

This is where multi-market merchants often begin to feel the limitations of a single global setup.

HaiPay has integrated 100+ PSP and acquiring resources, supports 150+ payment methods across 50+ countries and regions, and supports settlement in 30+ currencies, based on HaiPay product data current as of June 2026.

The important evaluation question, however, is not the length of a payment-method list. It is whether the available payment methods, acquiring paths, localized risk handling, and settlement options match the markets in which the merchant actually operates.

Payment API Integration

For engineering teams, payment orchestration should ultimately translate into a maintainable integration model.

The intended pattern is one standardized integration supporting multiple payment capabilities and markets, rather than a separate architecture for every provider.

A standardized API can reduce differences in:

- Payment request structures.

- Authentication methods.

- Response formats.

- Status mappings.

- Refund operations.

- Webhook handling.

- Reconciliation fields.

Before committing to a payment integration, engineering teams should review:

- API documentation quality.

- Authentication requirements.

- Request and response consistency.

- Idempotency support.

- Webhook and callback design.

- Error-code documentation.

- Sandbox availability.

- Test-payment workflows.

- Refund and dispute handling.

- Versioning and change management.

A standardized payment API is part of HaiPay’s offering.

Engineering teams can begin with the API integration overview and HaiPay’s API documentation.

For a developer-focused walkthrough of what a payment API is and how integration works in practice, see our guide to payment API integration.

The quality of an orchestration product is not defined only by how many providers it connects. It is also defined by how predictable the integration remains as payment capabilities expand.

Compliance: PCI DSS Scope and 3DS2/SCA

Compliance requirements depend on how payment data moves through the merchant’s environment and which systems store, process, or transmit sensitive data.

An orchestration layer does not automatically remove compliance obligations.

PCI DSS Scope

How cardholder data is collected and transmitted affects which systems and processes may fall within PCI DSS scope.

PCI Security Standards Council guidance recommends beginning with the assumption that systems are in scope until their status has been properly verified.

Approaches such as outsourcing certain functions to a compliant third-party service provider or using an eligible point-to-point encryption solution may reduce the number of in-scope system components.

However, reduced scope does not mean no security responsibility.

Systems considered out of scope may still become part of an attack path if segmentation, access control, or data-flow assumptions are incorrect.

Businesses should therefore confirm:

- Where card data is entered.

- Whether card data touches merchant systems.

- Which provider hosts the payment form.

- How tokens are created and stored.

- Which systems receive payment callbacks.

- How access to payment data is controlled.

- Which parties are responsible for each PCI DSS requirement.

Whether orchestration reduces PCI DSS scope depends on the actual architecture. It should never be assumed automatically.

3DS2 and Strong Customer Authentication

EMV 3-D Secure, commonly referred to as 3DS2, is an authentication protocol for card-not-present transactions.

It enables merchants and issuers to exchange transaction and risk data so that the issuer can authenticate the cardholder where required.

3DS2 can support Strong Customer Authentication requirements in applicable European payment scenarios.

However, 3DS2 authentication and fraud-liability shift are related but separate concepts.

The authentication protocol itself does not define every liability outcome. Liability treatment is determined by the applicable card scheme rules, transaction circumstances, exemptions, and implementation details.

Businesses evaluating an orchestration provider should examine:

- Supported 3DS versions.

- Authentication data handling.

- Exemption support.

- Challenge and frictionless flows.

- Regional authentication requirements.

- Reporting of authentication outcomes.

- Scheme-specific liability rules.

Compliance and authentication decisions should be reviewed against the merchant’s actual transaction types, regions, providers, and legal obligations.

Who Should Use Payment Orchestration?

Payment orchestration is not necessary for every business.

Businesses That May Benefit

A business may benefit when it:

- Uses or plans to use more than one payment provider.

- Operates across several markets.

- Needs different local payment methods.

- Maintains several provider-specific integrations.

- Has a large engineering backlog related to payment connections.

- Reconciles transactions across providers manually.

- Needs more consistent order-status handling.

- Wants a standardized payment-data model.

- Requires different payment paths for different markets or products.

The need usually becomes clearer as the number of providers, markets, currencies, methods, and operational teams increases.

Businesses That May Not Need It Yet

A business may not need payment orchestration when:

- One acquirer or PSP already covers its current markets.

- There is no near-term plan to add providers.

- The payment operation is still simple.

- The additional layer would create more complexity than value.

- The business does not have the resources to operate or review routing logic.

- Existing reconciliation processes remain manageable.

Adding an orchestration layer creates its own integration, configuration, monitoring, and governance requirements.

If one connection already meets the business need, maintaining that simpler architecture may be the right decision.

The central trade-off is between single-provider simplicity and multi-provider control.

Orchestration becomes more valuable when the cost of maintaining fragmented payment connections exceeds the cost of operating the layer that coordinates them.

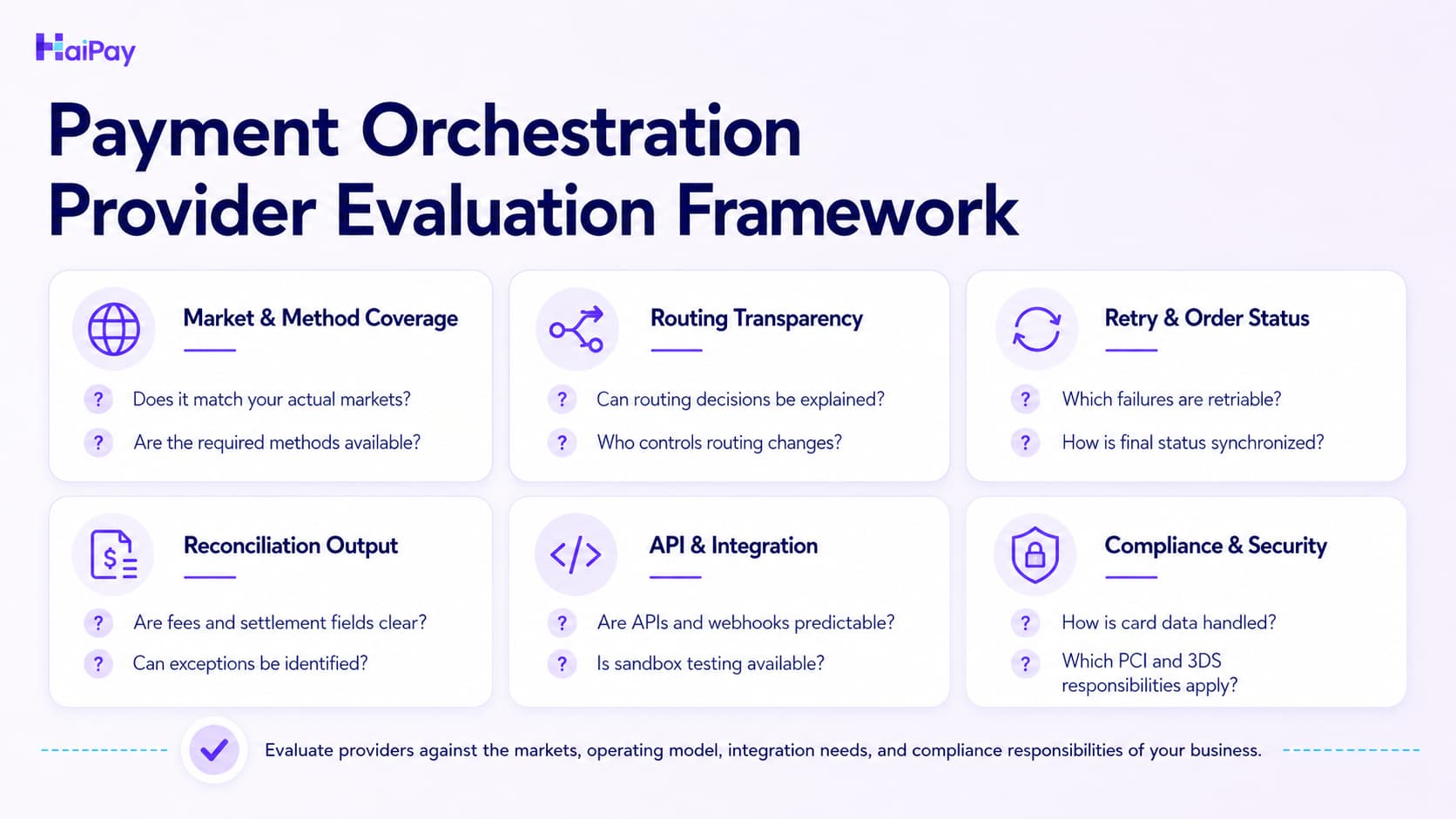

How to Evaluate a Payment Orchestration Provider

A provider evaluation should begin with the merchant’s real operating requirements rather than the longest available feature list.

Routing-only vs. routing + failover — know which you're evaluating

Not every orchestration layer does the same job. Some only make the routing decision: which provider should try this transaction. Others also handle what happens when that attempt fails, such as an automatic retry to a backup processor.

These are two different capabilities, and the term “orchestration” is often used loosely for both. Before evaluating a provider, be clear about which capability the business actually needs — and which one the provider actually offers.

Routing decision only | Routing + automatic failover | |

|---|---|---|

What it does | Picks the best provider or acquirer for each transaction based on rules such as region, amount, payment method, or cost. | Includes routing decisioning, plus automatically re-attempts a failed or declined transaction through a backup provider. |

Best suited to | Businesses optimizing for cost, local acquiring, or payment-method coverage across markets. | Businesses whose top priority is recovering every possible sale in real time, even at higher complexity or cost. |

What to ask the vendor | “What signals drive the routing decision, and can the merchant set its own rules?” | “Is failover automatic and real-time? Which decline reasons trigger a retry? Is there a limit on retry attempts?” |

Where HaiPay fits | HaiPay makes the routing decision across multiple in-market PSP connections, and retries failed subscription charges on the same channel. | HaiPay does not automatically reroute a failed transaction to a backup processor. If real-time cross-provider failover is a hard requirement, evaluate it explicitly. |

If real-time failover is a hard requirement for the business, confirm it explicitly during evaluation. Many “orchestration” tools stop at the routing decision, and that can be the right choice when the priority is cost, local acquiring, and market coverage rather than last-mile recovery.

1. Market and Payment-Method Coverage

Confirm that the provider supports the countries, currencies, payment methods, and acquiring paths that matter to the business.

A large generic method count has limited value when the methods do not match the merchant’s target customers.

2. Routing Model and Transparency

Ask:

- Which factors influence routing?

- Is routing self-service or managed?

- Can the merchant understand why a transaction followed a route?

- How are routing changes requested or configured?

- How are rules tested?

- How are unexpected routing outcomes investigated?

The required level of control will differ between merchants.

3. Retry Availability and Order-Status Handling

Confirm:

- Whether retry is offered at all.

- Which failure types are eligible, if retry is supported.

- How attempt limits are applied.

- How duplicate transactions are prevented.

- How order states are synchronized.

- How delayed provider responses are handled.

- How refunds and disputes affect order status.

Do not assume that retry or automatic failover is included. Confirm both capabilities explicitly with the provider.

4. Reconciliation Output

Review the actual reconciliation format rather than relying only on a product description.

Determine whether the output:

- Matches merchant order IDs.

- Includes provider transaction IDs.

- Separates fees and refunds.

- Identifies settlement amounts.

- Supports multiple currencies.

- Highlights exceptions.

- Can be imported into existing finance workflows.

The objective should be a measurable reduction in manual finance work.

5. Integration Effort

Read the API documentation before making a commercial commitment.

Review:

- Endpoint structure.

- Authentication.

- Error handling.

- Webhooks.

- Sandbox behavior.

- Idempotency.

- Versioning.

- Refund workflows.

- Reporting and reconciliation APIs.

A standardized API should reduce integration duplication, but the initial implementation still needs proper technical scoping.

6. Compliance and Security Posture

Confirm how the provider supports:

- PCI DSS responsibilities.

- Card-data handling.

- Tokenization.

- Authentication.

- 3DS2.

- Strong Customer Authentication.

- Access controls.

- Audit records.

- Regional regulatory requirements.

Compliance claims should be assessed against the merchant’s actual data flows and legal responsibilities.

7. Operating Model

Determine who is responsible for:

- Routing configuration.

- Provider management.

- Performance monitoring.

- Incident handling.

- Payment-method changes.

- Reconciliation exceptions.

- Compliance updates.

- Technical support.

A platform with extensive self-service controls may suit a merchant with a dedicated payment team. A managed model may suit a merchant that wants the provider to operate more of the payment complexity.

The best operating model is the one that matches the merchant’s internal resources and desired level of control.

Businesses preparing an integration can review HaiPay’s API integration overview as a starting point.

Sources

- PCI Security Standards Council.Guidance for PCI DSS Scoping and Network Segmentation. Information supplement aligned with PCI DSS v4.0.

https://www.pcisecuritystandards.org/ - PCI Security Standards Council.Glossary of Terms. Definitions relating to acquirers, payment processors, payment gateways, and payment service providers.

https://www.pcisecuritystandards.org/glossary/ - EMVCo.EMV 3-D Secure. Technical overview of the authentication protocol and its role in supporting Strong Customer Authentication.

https://www.emvco.com/emv-technologies/3-d-secure/

Disclosure

HaiPay is a payment provider, and this guide is published for educational purposes.

HaiPay at haipay.net is distinct from similarly named entities operating through other domains.

FAQ

A gateway transmits transaction data to a processor or acquirer. Payment orchestration coordinates multiple gateways, PSPs, acquirers, and payment methods behind one integration and can apply routing, reconciliation, order-status synchronization, and, where supported, retry logic.

Related HaiPay surfaces

Explore the payment stack

Acquiring

Local and Global Acquiring

Explore how local and global acquiring support payment acceptance across markets, currencies, and payment methods.

Developer Integration

Payment API Integration

Review HaiPay’s standardized API approach for integrating payments, synchronizing order status, and managing multi-market payment flows.

Acquiring Decisions

What Is Merchant Acquiring?

Learn how merchant acquiring connects merchants with payment networks and supports authorization, clearing, and settlement.

Payment Roles

What Is a Payment Facilitator?

Understand how payment facilitators differ from acquirers, gateways, ISOs, and payment orchestration providers.

Need help mapping your payment stack?

Talk to HaiPay about acquiring, orchestration, local methods, and payout workflows.

Contact us