Intelligent Payment Routing: How It Works and the Main Routing Strategies

Last updated: July 21st, 2026

Insights

Intelligent payment routing is the practice of directing each transaction to a payment provider or path according to rules — such as the market, currency, payment method, or cost — instead of sending everything down one fixed route. The goal is to handle each payment in the way that best fits it. This article explains how routing works, the main routing strategies, how routing differs from retrying a failed payment, and when you actually need it.

What is intelligent payment routing?

Intelligent payment routing is a rules-driven way of deciding which provider or path handles a given transaction. Rather than a single fixed connection that every payment flows through, a routing system evaluates attributes of the transaction — and sometimes live signals — and chooses a route accordingly.

In plain terms: “payment routing” is the decision of where a transaction goes; “intelligent” or “smart” routing means that decision is driven by rules and data rather than being hard-coded to one provider. Note this is unrelated to a bank “routing number”, which is a consumer-banking identifier, not transaction routing.

How intelligent payment routing works

At a high level, routing happens at the moment a payment is initiated. The system reads attributes of the transaction — for example its market, currency, payment method, amount, or card type — and applies your rules to pick a provider or path. The transaction is then sent to that provider for authorization and capture, and the outcome is recorded.

The part that makes routing “intelligent” is that the rules can take several factors into account at once, and good systems let you see and change those rules without re-engineering your checkout. Routing you can’t inspect is effectively a black box — when a transaction goes somewhere unexpected, you want to be able to tell why.

A concrete example makes the flow clearer. Say a customer in one market pays with a local card. The routing layer reads the market and method, matches them against your rules, and sends the authorization to the provider you designated for that combination.

If you also have a least-cost rule, and two providers can both handle that market and method, the layer picks the cheaper one. The transaction is authorized, and the result — provider chosen, outcome, reason — is recorded so you can audit the decision later.

The decision took milliseconds; the value is that it was made by a rule you can read rather than by a hard-coded default you can’t change.

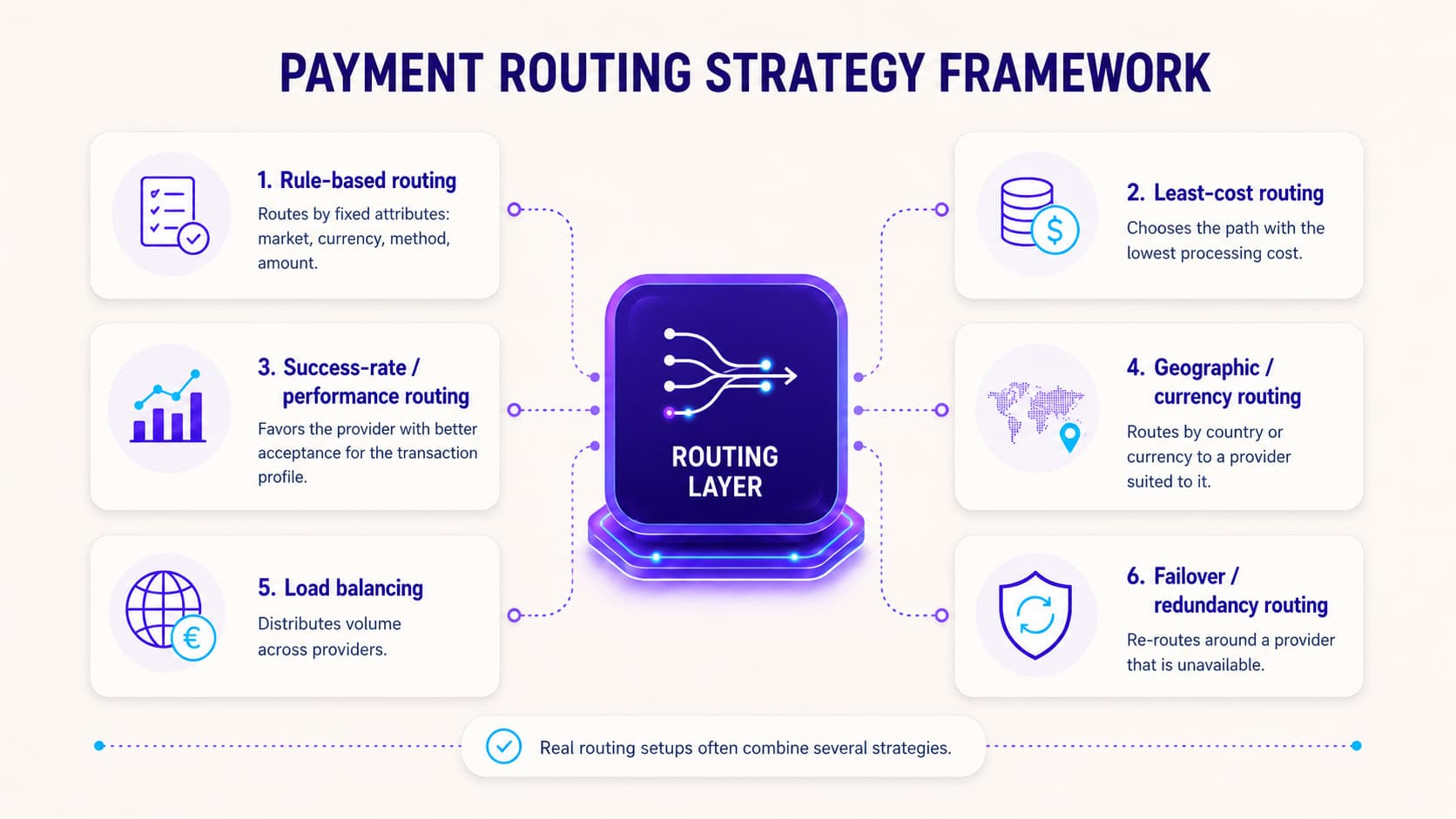

Routing strategies: the main rule types

Most routing setups are built from a handful of strategy types, often combined. The table summarizes the common ones.

Strategy | What it does | Typical use |

|---|---|---|

Rule-based routing | Routes by fixed attributes you define (market, currency, method, amount) | The baseline: predictable, explicit control |

Least-cost routing | Chooses the path with the lowest processing cost for that transaction | Cost optimization across providers |

Success-rate / performance routing | Favors the provider with better acceptance for that transaction profile | Acceptance optimization |

Geographic / currency routing | Routes by country or currency to a provider suited to it | Cross-border and local acceptance |

Load balancing | Distributes volume across providers | Avoiding concentration on one provider |

Failover / redundancy routing | Re-routes around a provider that is unavailable | Continuity (an industry strategy type — see the next section on how this differs from retry) |

These are industry-standard strategy categories, not features unique to any one vendor. Most real configurations blend a few — for example, route by market first, then prefer the lower-cost provider within that market — rather than relying on a single rule.

Each strategy also has a trade-off worth knowing before you turn it on.

Least-cost routing saves on fees, but if it ignores acceptance it can quietly send transactions to a cheaper provider that approves fewer of them — saving cents and losing sales.

Success-rate routing only works once you have enough history to know which provider performs better for a given transaction profile; on day one, with no data, it has nothing to act on.

Load balancing helps you avoid leaning on one provider, but it adds more moving parts to monitor.

The lesson is not “use all of them” — it is to add a strategy only when you can name the problem it solves for you.

Routing vs failed-payment retry

These two are often confused, and the distinction matters. Routing decides where a transaction goes in the first place. Failed-payment retry is what happens after a payment fails — re-attempting it under rules you define.

They work together but are not the same mechanism, and “intelligent routing” should not be read as a promise of automatic, real-time switching between providers mid-transaction.

The practical reason to keep them separate: retry has its own risks. Retrying a permanent decline is pointless; retrying carelessly can create duplicate charges. Retry rules and limits deserve their own design rather than being folded into routing as if it were one switch.

A useful way to remember the order:

Routing is the first decision: where does this payment go?

Retry is the second decision: what do we do if it failed?

A transaction can be routed well and still fail, and it can fail for a reason no retry will fix. Designing the two separately keeps each one honest — your routing rules stay about fit, and your retry rules stay about recovery, instead of one vague setting trying to do both.

Benefits — and what to watch

The honest benefits of routing are about control, not magic numbers:

- Acceptance fit. Sending a transaction to a provider suited to its market or method can help it succeed, rather than forcing everything through one path.

- Cost control. Least-cost strategies can reduce processing cost where you have more than one viable path.

- Transparency. Rules you can inspect and change mean you can debug and adjust without re-engineering.

What to watch: more rules are not automatically better. Each rule is something to maintain and reason about, and an over-complex rule set becomes its own source of bugs.

The goal is the smallest set of rules that does the job. Any specific uplift figure is a measured outcome for your own traffic, not a guarantee — treat vendor headline numbers with that in mind.

When you don’t need complex routing

If you run a single provider that covers your markets and volume, you may not need a routing layer at all — one path is simpler to operate and debug.

Routing earns its keep once you have more than one provider, sell across markets with different local methods, or have a clear cost or acceptance reason to choose between paths. Adding routing complexity you don’t use is cost without benefit.

A simple test before you adopt routing: can you name the specific rule you would write and the problem it solves?

“Route EU transactions to the provider with local acquiring there” is a concrete reason.

“We might want routing someday” is not — and a routing layer you don’t have a rule for is just another system to maintain.

Start from the problem, not the feature.

How intelligent payment routing fits into payment orchestration

Routing is one part of a larger picture. In a payment orchestration setup, routing sits alongside processing, failed-payment retry, and reconciliation as the stages applied to each transaction — see the intelligent-payment-routing section of that guide for how the pieces connect.

HaiPay uses a managed (backend-managed) automatic payment routing model as part of its acquiring offering. Payment paths are selected by factors such as order type, transaction amount, region, and channel status, with the rules maintained in HaiPay’s operations backend rather than configured by the merchant.

One honest boundary to set: HaiPay currently does not provide automatic failover or platform-initiated retries — a failed transaction’s result is returned directly to the merchant.

You can read how the acquiring side works in our local and global acquiring overview. If you are scoping an integration, the API integration overview is a good starting point.

Sources

- Industry-standard routing strategy categories — rule-based, least-cost, success-rate, geographic, load balancing, and failover/redundancy — are described consistently across payments documentation; definitions here are stated in general terms and not attributed to any single vendor.

- For the broader context, see HaiPay’s guide: What Is Payment Orchestration?

Disclosure: HaiPay is a payment provider; this article is educational. HaiPay (haipay.net) is distinct from similarly named entities such as haipay.io, hipay.com, and haipay.in.

FAQ

It is directing each transaction to a provider or path based on rules such as market, currency, method, or cost, rather than sending every payment down one fixed route.