Direct Answer

Recurring payment processing automatically charges a customer’s saved card, bank account, or supported wallet on an agreed schedule. It uses customer consent, tokenized credentials, merchant-initiated transactions, retry logic, and lifecycle controls to manage renewals, payment failures, cancellations, and reconciliation.

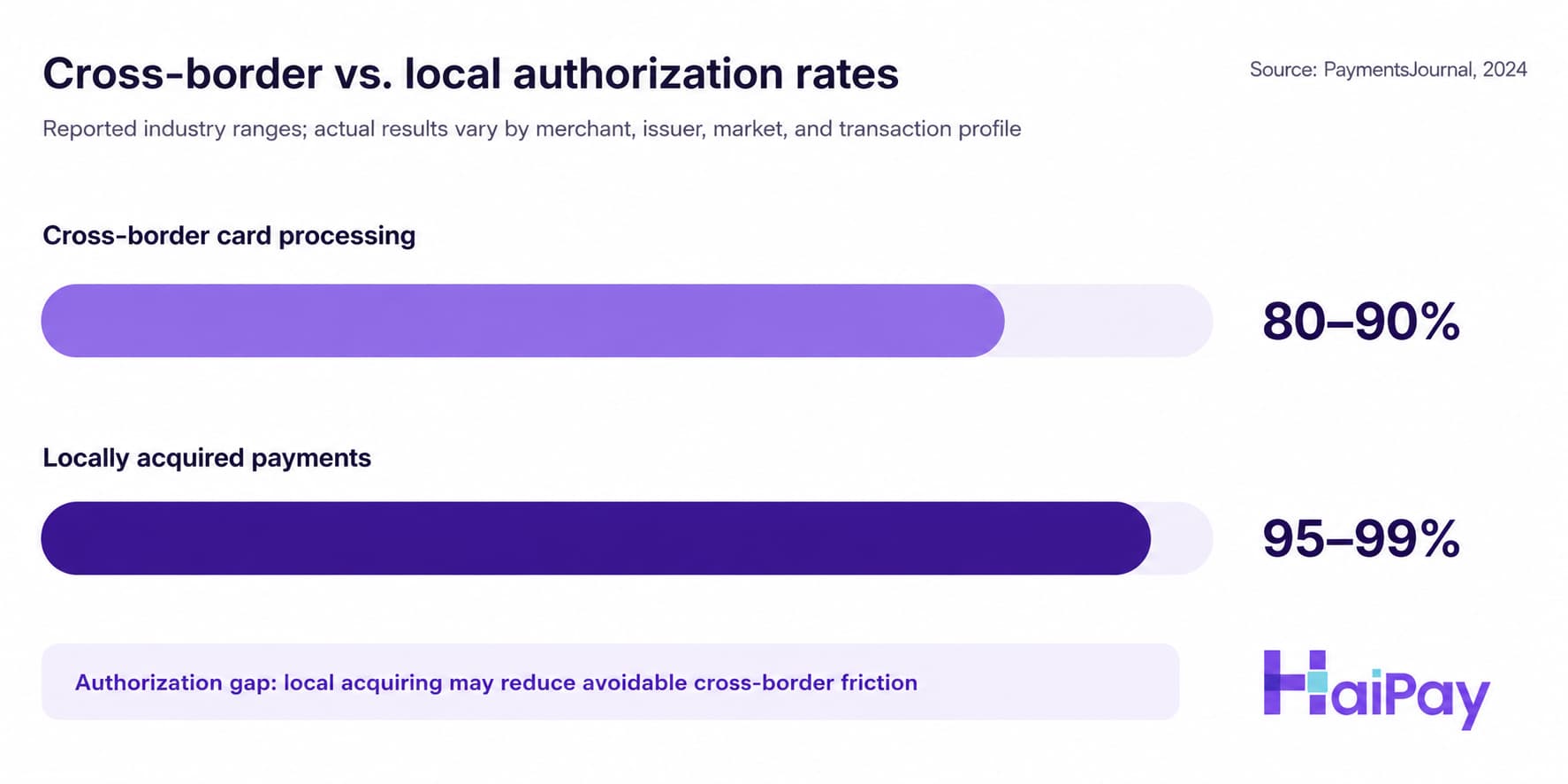

Recurring payment processing is the system that automatically charges a customer’s saved card or bank account on a set schedule — most often as a merchant-initiated transaction (MIT) that the customer pre-authorized. It is what turns a one-time sale into predictable subscription revenue. The challenge for global businesses is that renewals can fail more frequently when customers and acquiring routes are spread across different markets. Industry analyses commonly place cross-border authorization rates at 80–90%, compared with 95–99% for locally acquired payments. This guide explains how recurring payment processing works from authorization to reconciliation, and how local acquiring, tokenization, and intelligent retries can improve renewal performance.

What is recurring payment processing?

Recurring payment processing is the automated handling of payments that repeat on a schedule — weekly, monthly, annually, or at any interval a customer agrees to.

Instead of asking the customer to complete a new payment every cycle, the merchant securely stores the customer’s payment credentials, with consent, and automatically initiates charges according to the agreed schedule.

Recurring payment vs. recurring billing

These terms are often used interchangeably, but they describe different layers:

- A recurring payment is an individual transaction — the charge submitted to the customer’s card or account on a billing date. Technically, it is usually a merchant-initiated transaction (MIT) processed using stored credentials.

- Recurring billing is the broader system that manages the payment schedule, subscription logic, customer communication, failed-payment retries, invoicing, and compliance controls.

In simple terms, a recurring payment is the transaction, while recurring billing is the system that manages the transaction lifecycle.

Fixed vs. variable recurring payments

- Fixed recurring payments: The same amount is charged every cycle, such as a $25 monthly membership.

- Variable recurring payments: The amount changes according to consumption, usage, or quantity, such as cloud storage, utilities, or metered API usage.

Variable recurring payments are also commonly associated with autopay, because the amount is calculated from the customer’s actual consumption.

Merchant-initiated transactions and card on file

A card-on-file (CoF) arrangement allows a merchant to securely retain a customer’s card credentials for future transactions after receiving explicit consent.

Recurring renewals are a common card-on-file use case. The renewal is submitted as an MIT, meaning that the merchant initiates the payment without requiring the customer to return to checkout for every billing cycle.

Card on file is one of several stored or streamlined payment concepts that are frequently confused. The comparison below explains how it differs from Click to Pay and Pay by Link.

How recurring payment processing works

- Authorization and consent.

The customer agrees to recurring charges during sign-up by accepting the billing terms, checking a consent box, or signing an agreement. The terms should clearly state the amount or calculation method, billing frequency, product or service, renewal conditions, and cancellation rights. - Tokenize and securely store payment details.

Payment credentials are tokenized and stored in a PCI DSS-compliant vault. The merchant retains a token instead of the customer’s raw card number. - Set the billing schedule.

The billing system records the payment interval, subscription status, billing amount, and next charge date. - Process the transaction.

On the billing date, the payment gateway sends the transaction request. The payment processor routes it through the card network or applicable payment rail, and the issuing bank approves or declines the charge. The renewal settles over the same merchant acquiring infrastructure as a one-time card payment; where those acquiring routes sit relative to the customer is what drives cross-border decline rates. - Confirm the result and issue a receipt.

When the payment succeeds, the transaction is confirmed and the customer receives a receipt or billing notification. Clear confirmation records can also help reduce disputes. - Handle failures and retry.

Failed charges caused by expired cards, insufficient funds, authentication requirements, or temporary issuer decisions may be retried according to defined rules. Intelligent systems vary the retry timing instead of repeatedly submitting the same request. - Manage the subscription lifecycle.

Upgrades, downgrades, prorated charges, free trials, pauses, cancellations, renewals, and refunds must all feed back into the billing schedule. - Report and reconcile.

Successful payments, failed payments, refunds, churn, taxes, and settlement data flow into financial reporting and reconciliation systems.

Ways to collect recurring payments

Recurring payments can run across several payment rails. The appropriate mix depends on the markets a business serves and the payment methods its customers prefer.

- Cards and card on file: Common for digital subscriptions because they are familiar, widely accepted, and supported by established consumer-protection frameworks. Card processing can carry higher costs than some bank-based methods.

- ACH and direct debit: Bank-account-based pull payments that can suit larger-value or B2B recurring transactions. Availability, timing, and mandate requirements vary by market.

- Digital wallets: Apple Pay, Google Pay, and other supported wallets may enable recurring mandates while simplifying the initial checkout experience.

- Alternative payment methods and Pay by Bank: Local wallets, direct debit, account-to-account rails, and other market-specific payment methods can be important where international cards are not the customer’s default choice.

See the Alternative Payment Methods guide for a broader comparison of wallets, bank payments, QR payments, local schemes, and other payment options.

Card on File vs. Click to Pay vs. Pay by Link

These three concepts solve different payment problems.

Card on File | Click to Pay | Pay by Link | |

|---|---|---|---|

What it is | Stored card credentials for future use | A network-standard online checkout based on EMV® SRC | A payment request delivered through a URL |

Who initiates | Merchant after customer consent, usually as an MIT | Customer during checkout | Merchant sends the link; customer completes the payment |

Scope | One specific merchant relationship | Participating merchants across supported networks | One specific payment request or collection flow |

Best for | Recurring billing and one-click repeat purchases | Faster and more consistent guest checkout | Remote collection and invoice payments without a full website |

Backed by | Merchant vault and tokenization infrastructure | EMVCo and participating card networks | The merchant’s payment provider |

The simplest way to remember the difference is:

- Card on file stores a payment credential.

- Click to Pay provides a standardized checkout experience.

- Pay by Link sends the customer a payment request.

These methods can also work together. A Pay by Link page may offer Click to Pay and allow an eligible customer to save a card for future transactions.

For a no-code collection option, see HaiPay Payment Links.

Why recurring payments fail

Failed subscription renewals do not always mean that a customer has decided to leave.

Subscription-billing platforms including Chargebee and Recurly estimate that 20–40% of subscription churn is involuntary — driven by failed payments rather than deliberate cancellation. Recurly's research puts the revenue impact at roughly 9% of annual revenue lost to failed recurring payments.

Common causes include:

- Expired or replaced cards

- Insufficient funds

- Bank authentication or SCA requirements

- Issuer fraud controls and spending limits

- Cross-border transaction flags

- Cancelled cards

- Payment processor or network interruptions

- Incorrect stored payment information

Smart retries, dunning, and account updater services

Revenue recovery depends heavily on how failed transactions are handled.

- Intelligent retries adjust the timing, parameters, or available processing route for a new attempt instead of repeatedly submitting an identical transaction.

- Dunning is the sequence of emails, messages, or in-product prompts that asks a customer to update a failed payment method.

- Account updater services can receive updated card details when an issuer replaces or renews an eligible card.

- Network tokenization can help keep supported stored credentials current and reduce reliance on static card details.

Effective dunning should provide a clear explanation and a simple payment-update path without forcing the customer through unnecessary steps.

HaiPay product context: HaiPay’s processing engine supports capabilities such as automatic retry handling, BIN identification, 3D Secure routing, and transaction-message optimization. Actual authorization results depend on the market, issuer, transaction profile, and available payment route.

The cross-border recurring payment problem

Global recurring payments face additional authorization challenges because the customer, merchant, issuer, and acquirer may be located in different markets.

A cross-border indicator can affect how an issuer evaluates the transaction. The issuer may have less historical context for the merchant, while differences in currency, location, merchant category, authentication, and transaction data can increase the likelihood of a decline.

Scenario | Typical authorization rate |

|---|---|

Cross-border card processing | 80–90% |

Locally acquired payments | 95–99% |

Source: industry analyses cited by PaymentsJournal (2024). Actual performance varies by merchant, issuer, market, transaction type, and customer mix.

For a recurring business, even a small authorization gap can compound over repeated billing cycles. A subscriber who intended to continue using the service may still be lost when a renewal fails and is not recovered.

How local acquiring and intelligent routing support renewals

Common ways to narrow the cross-border authorization gap include:

- Local acquiring: Process transactions through an in-market acquiring connection where available, allowing eligible payments to be handled more like domestic transactions.

- Intelligent routing: Select an appropriate payment route based on transaction details, channel status, market, and payment method.

- Retry logic: Reattempt recoverable declines according to appropriate timing and retry rules.

- Network tokenization: Keep supported stored credentials current when underlying card details change.

- Proper 3DS2 handling: Apply authentication when required while preserving an appropriate customer experience.

Local payment methods for recurring payments

Customers in many markets do not default to international cards.

Supporting local payment methods, direct debit, wallets, and account-to-account rails can help a recurring business align its payment experience with local customer preferences. The availability of recurring mandates depends on the specific payment method and market.

See Alternative Payment Methods and the Payment Orchestration guide for more detail.

Security and compliance for recurring payments

Storing credentials and initiating future charges increases the importance of payment security, consent records, and compliance controls.

- PCI DSS: Businesses that store, process, or transmit cardholder data must meet the applicable PCI DSS requirements.

- Tokenization: Raw card data is replaced with a non-sensitive token that can be used within an authorized payment environment.

- SCA and 3DS2: In the European Economic Area and the UK, the initial setup or first payment may require Strong Customer Authentication. Eligible later MITs may be treated differently, provided that the recurring relationship was established correctly.

- Customer consent: The merchant should retain evidence that the customer agreed to the amount, frequency, renewal terms, and cancellation process.

- Market-specific mandates: Recurring payment rules vary by jurisdiction. Examples include EU SCA requirements and India’s framework for recurring card mandates.

- Cancellation controls: Customers should have a clear and accessible way to stop future charges.

A recognizable billing descriptor can also reduce customer confusion and disputes. The descriptor should align closely with the merchant’s brand or service name.

Price, frequency, trial terms, renewal conditions, and cancellation rights should be clearly displayed during sign-up rather than hidden in secondary terms.

How to set up recurring payment processing

1. Choose a processor or PSP

Evaluate providers according to the markets, payment methods, billing models, compliance requirements, and technical resources of the business.

2. Define billing plans

Set the following rules before implementation:

- Billing frequency

- Fixed, usage-based, or hybrid pricing

- Trial periods

- Accepted payment methods

- Renewal notifications

- Failed-payment retries

- Dunning communications

- Upgrades and downgrades

- Proration

- Pauses and cancellations

- Refund handling

3. Test the full payment lifecycle

Testing should cover more than a successful initial charge.

Businesses should test:

- Successful subscription creation

- First-payment authentication

- Scheduled renewals

- Expired-card scenarios

- Insufficient-funds declines

- Retry behavior

- Card-update flows

- Upgrade and downgrade calculations

- Cancellation behavior

- Refunds

- Customer notifications

- Webhooks and order-status updates

- Reconciliation and accounting exports

4. Launch and monitor performance

Track both the initial checkout and later renewals.

Useful metrics include:

- Initial payment authorization rate

- Renewal authorization rate

- Retry recovery rate

- Involuntary churn

- Voluntary churn

- Payment-method update rate

- Refund and dispute rate

- Revenue recovered through dunning

- Authorization performance by market and payment method

Processor selection checklist for global subscriptions

- ✅ Local acquiring coverage in priority markets

- ✅ Local payment methods that support the intended billing model

- ✅ Smart retry and dunning capabilities

- ✅ Account updater or network-token support

- ✅ PCI DSS and appropriate security controls

- ✅ SCA and 3DS2 support

- ✅ Market-specific recurring mandate support

- ✅ Clear API documentation and webhook behavior

- ✅ No-code or low-code options where required

- ✅ Reliable transaction reporting and reconciliation

- ✅ Clear pricing for transactions, authorization attempts, refunds, and disputes

Headline transaction pricing should be evaluated together with authorization performance, recovery capabilities, operational effort, and market coverage.

How HaiPay handles recurring payments

This section describes HaiPay’s own product. Product availability, payment methods, authorization performance, and commercial terms vary by market, merchant profile, transaction mix, and implementation.

HaiPay provides cross-border payment infrastructure for businesses that need to collect recurring payments across multiple markets.

Flexible subscription billing models

HaiPay supports three subscription billing structures:

- Fixed-Cycle Billing: Recurring prepayment on a monthly, quarterly, annual, or other defined schedule.

- Usage-Based Billing: Post-paid billing based on actual consumption.

- Hybrid Billing: A fixed base charge combined with usage-based or overage charges.

These structures can support SaaS, content platforms, memberships, digital services, and other recurring business models.

Subscription lifecycle capabilities may include:

- Free trials

- Automatic renewals

- Upgrades and downgrades

- Prorated charges

- Cancellations

- Refunds

- Failed-payment handling

Card on file and retry handling

HaiPay supports saved-card recurring payments using merchant-initiated transaction flows.

Related processing capabilities include:

- Intelligent retry handling

- BIN identification

- 3D Secure matching and routing

- Transaction-message optimization

- Payment-route selection

- Order-status synchronization

Authorization improvements depend on the customer’s issuing bank, payment method, market, merchant category, transaction data, and available payment channels.

Global payment coverage

HaiPay supports major card schemes, including:

- Visa

- Mastercard

- American Express

- JCB

- UnionPay

HaiPay also provides access to local payment methods across multiple markets, including options such as Alipay, WeChat Pay, Pix, and UPI, subject to merchant eligibility, market availability, and the capabilities of each payment method.

Where an eligible local acquiring route or local payment method is available, the transaction can be processed through a payment experience that better matches the customer’s market.

Payment Links

HaiPay Payment Links can support remote and invoice-style collection without requiring a merchant to build a complete checkout page.

The customer receives a shareable payment URL and completes the payment through the hosted payment flow. Whether a specific method supports future recurring charges depends on the payment method, mandate structure, and implementation.

Security and fraud controls

HaiPay’s payment infrastructure includes capabilities such as:

- PCI DSS-compliant card processing

- Tokenized payment credentials

- Real-time transaction risk assessment

- 3D Secure handling

- Fraud-screening controls

- Transaction monitoring

These controls are designed to help businesses manage fraud exposure, false declines, and recurring payment risk. Actual outcomes depend on the merchant’s business model and transaction profile.

Subscription pricing

HaiPay’s published subscription page lists a percentage-pricing option of 2.9% + $0.30 per transaction, with no setup fee and a stated T+3 settlement cycle. An IC++ pricing option is also available.

Commercial terms can change and may vary by merchant, country, payment method, transaction volume, risk profile, and settlement arrangement. Businesses should confirm current terms with HaiPay before implementation.

Explore HaiPay Subscription for product capabilities and billing models.

Explore the HaiPay Subscription API for integration details.

Sources

- Cross-border vs. local authorization rates (80–90% vs. 95–99%): industry analyses cited by PaymentsJournal, 2024 (via orchestrasolutions.com).

- Cross-border vs. domestic failure rate (15–25% vs. 1–5%): CoinLaw, 2025.

- Click to Pay spec:EMVCo Secure Remote Commerce.

- PCI DSS:PCI Security Standards Council.

- HaiPay product details:haipay.net/payins/subscription · Subscription API.

FAQ

A customer authorizes a merchant to store a payment method and charge it on an agreed schedule. Each renewal is usually processed as a merchant-initiated transaction, with a receipt issued after a successful charge.

Related HaiPay surfaces

Explore the payment stack

Subscription

Automate recurring billing across global markets

Explore flexible billing cycles, smart dunning, global payment coverage, and developer-friendly subscription APIs.

Payment Orchestration

Understand how payment orchestration works

Learn how one integration can coordinate payment providers, routing, retries, order status, and reconciliation.

Local Payment Methods

Choose the right payment methods by market

Compare wallets, Pay by Bank, local card schemes, QR payments, and other alternative payment methods for global checkout.

Payment Links

Collect payments without building a checkout

Create shareable payment links for one-time and recurring collection with no-code setup.

Need help mapping your payment stack?

Talk to HaiPay about acquiring, orchestration, local methods, and payout workflows.

Contact us