Alternative payment methods are payment options outside the traditional card payment flow. They can include digital wallets, Pay by Bank and other account-to-account payments, bank transfers, buy now pay later, local card schemes, QR payments, vouchers, real-time payment networks, cryptocurrency and stablecoin payments where legally available and other market-specific ways customers prefer to pay.

For businesses selling across markets, APMs shape checkout trust, payment completion, operational complexity, and the way finance teams handle settlement, refunds, reconciliation, and payment risk.

For a merchant, the practical question is simple: which payment methods should appear at checkout, in which markets, for which customers, and with what operational tradeoffs?

Use this guide to build that decision. When you are ready to validate availability for your own checkout, review HaiPay Checkout or talk to the payments team to confirm availability, settlement, refunds, and implementation requirements before launch.

What are alternative payment methods?

Alternative payment methods, often shortened to APMs, are ways to pay that are not the standard credit-card or debit-card payment flow. The exact boundary varies by provider and market, but most APM guides include wallets, bank-based payments, direct debit, buy now pay later, cash or voucher flows, QR payments, local card schemes, and other local payment options. The category boundary is not globally standardized, so this guide uses APM as a merchant-planning umbrella rather than a regulatory classification. Each method should be verified against official scheme, regulator, or provider documentation for the target market.

Digital payment adoption is expanding across markets. The World Bank’s Global Findex 2025, based on nationally representative surveys of about 148,000 adults across 141 economies, found that 42% of adults in low- and middle-income economies made an in-store or online digital merchant payment in 2024, up from 35% in 2021. This is a digital-payment adoption measure rather than a direct estimate of APM market share, but it shows why merchants need market-specific payment-method planning.

That definition matters because "alternative" does not mean niche. In many markets, a local wallet, bank transfer flow, account-to-account option, or domestic payment scheme may feel more familiar to customers than an international card checkout. The right payment mix is therefore a market decision, not just a feature list.

For B2B and cross-border businesses, APM selection usually comes down to five questions:

- Does the customer already trust this method?

- Does the method fit the transaction size and purchase context?

- What does the payment flow ask the customer to do?

- How do settlement, refunds, failures, and disputes work?

- Can the business support the method operationally after launch?

Why alternative payment methods matter

Payment methods influence whether a customer recognizes the checkout, completes authentication, understands what will happen next, and feels comfortable paying. A card-only checkout can work well in some segments, but it can also create friction when customers expect a local wallet, bank transfer, QR code, or domestic payment network.

APMs matter most when a business is expanding across countries, selling to customers with strong local payment habits, supporting recurring or invoice-like flows, or trying to reduce friction in high-intent checkout sessions. They also matter when finance, operations, and support teams need clearer answers about reconciliation, refund timing, and failed-payment recovery.

The strongest APM strategy is not "add every method." It is "add the methods that match the buyer, market, and operating model." That is the difference between a useful checkout and a crowded one.

Main types of alternative payment methods

The table below groups common APM categories by the job they do at checkout. Availability, settlement timing, refund rules, and compliance requirements vary by country, provider, merchant category, and payment method, so every row should be confirmed before implementation.

APM type | What the customer does | Where it often fits | Key questions before launch |

|---|---|---|---|

Digital wallets | Selects a wallet and confirms payment through an app, browser, or wallet account | Consumer checkout, mobile checkout, repeat buyers, local wallet markets | Which wallets are trusted in the target market? How are refunds, failures, and disputes handled? |

Pay by Bank and account-to-account payments | Authorizes payment from a bank account, often through bank authentication or open-banking-style flows | Bank-trusted markets, lower-card-usage segments, account-funded checkout, invoice-like flows | Which rails are used? How does authentication work? Are refunds and settlement handled through the same flow? |

Bank transfers and direct debit | Pays from a bank account through transfer, debit authorization, or local bank-payment scheme | Larger-ticket purchases, recurring payments, B2B-style flows, markets with strong bank payment habits | What is the confirmation timing? How are failed or reversed payments handled? |

Buy now pay later | Selects an installment or deferred-payment provider | Retail, discretionary purchases, higher average order value categories | Who owns credit decisioning, customer communication, refunds, and merchant settlement? |

Local card schemes | Pays with a domestic or regional card brand | Markets where local card networks have strong acceptance and customer recognition | Is the local scheme relevant to the target market? Is acceptance supported by the acquiring setup? |

QR payments | Scans or displays a QR code and confirms payment in a banking or wallet app | Mobile-first markets, in-person-to-online bridges, local bank or wallet ecosystems | Is the QR flow static or dynamic? How is payment status confirmed? |

Cash, voucher, or convenience-store payments | Receives a code or reference and pays offline or through a local network | Cash-preference segments, underbanked users, local cash networks | How long is the payment window? How are unpaid orders expired and reconciled? |

Cryptocurrency and stablecoin payments | Pays from a digital-asset wallet; the provider may convert the payment to fiat or settle the asset directly | Selected cross-border or digital-native use cases where legally and operationally supported | Which assets and networks are supported? How are exchange rates, settlement, refunds, reversibility, AML/sanctions screening, accounting, and tax handled? |

Real-time payment networks | Initiates an account-to-account payment, often through a bank app, redirect, or QR flow | Markets built around instant domestic rails such as UPI or Pix | How is payment confirmation returned? How do refunds, returns, fraud controls, reconciliation, and failed or pending states work? |

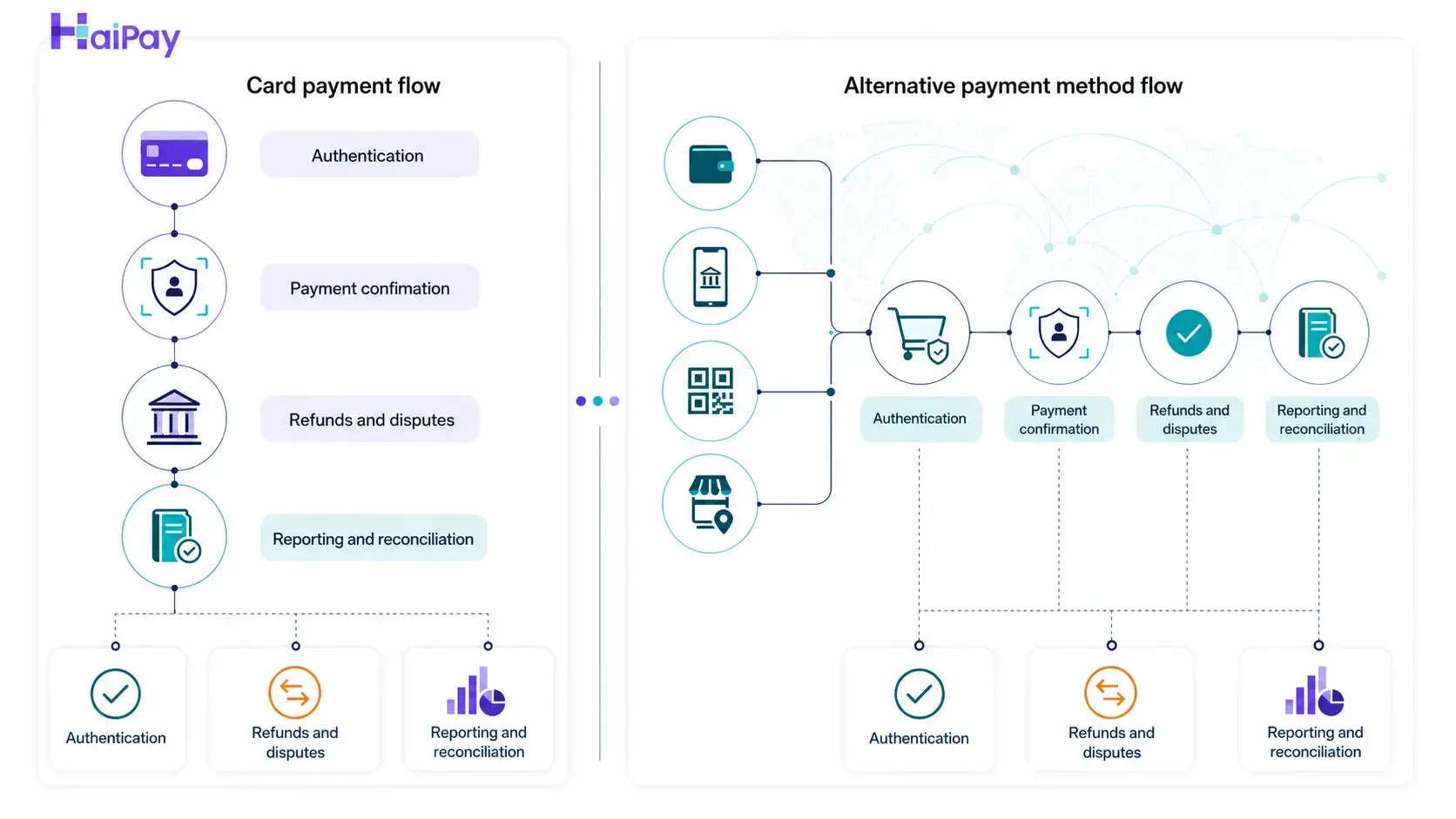

Alternative payment methods vs card payments

Cards are still a major part of online payment acceptance, but APMs differ from cards in how the customer authorizes payment, how the payment is confirmed, and how post-payment operations work.

Area | Card payments | Alternative payment methods |

|---|---|---|

Customer recognition | Familiar in many online markets | Often stronger when the method is local, bank-based, wallet-based, or already part of the customer's daily payment habits |

Authentication | Card details, wallet token, 3DS, or issuer authentication depending on setup | Varies by method: wallet login, bank authentication, QR scan, bank app confirmation, provider approval, voucher payment, or local scheme flow |

Payment confirmation | Usually immediate authorization response, with later clearing and settlement | Can be immediate, delayed, pending, expired, or manually reconciled depending on method |

Refund handling | Commonly card-network-driven, with established card refund patterns | Varies by method and provider. Refund route, timing, and customer communication must be verified |

Disputes and reversals | Card chargeback and dispute rules often apply | Rules differ widely. Some methods have disputes, some have reversals, and some require separate operational handling |

Implementation work | Card acquiring, tokenization, authentication, fraud rules, reporting | Method selection, market routing, local UX, status handling, reconciliation, support scripts, and provider-specific rules |

The goal is not to replace cards everywhere. The goal is to offer the methods that remove friction for the customers and markets you actually serve.

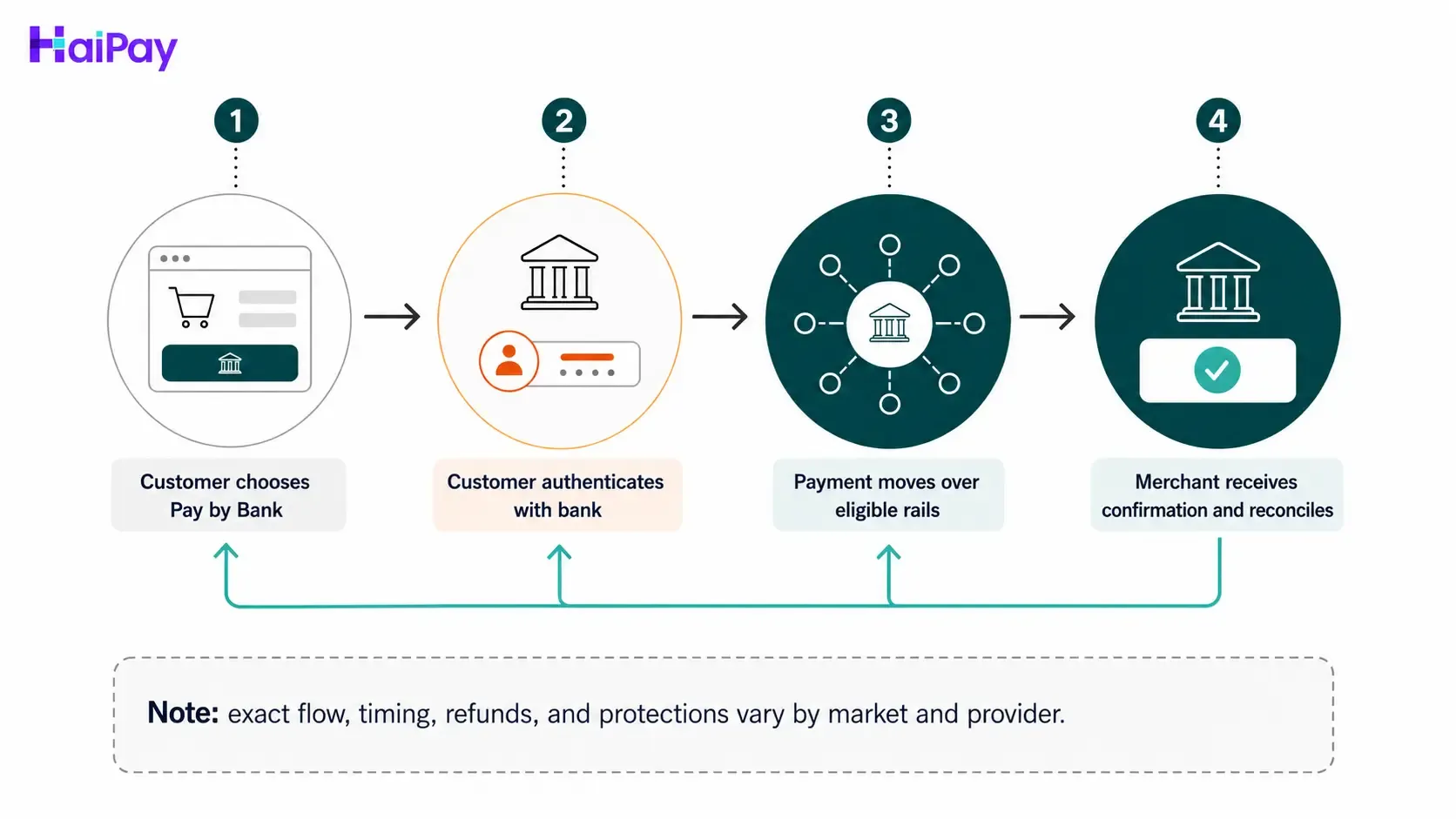

Pay by Bank and account-to-account payments

Pay by Bank is a bank-funded checkout flow. The customer pays from a bank account rather than typing card details. Account-to-account, or A2A, is the broader category of direct movement from one bank account to another. The Federal Reserve Pay-by-Bank note describes Pay-by-Bank as a bank-based payment model in which a transaction originates from the customer's bank account and is routed over bank payment rails to the merchant's bank account.

In some markets, Pay by Bank is closely connected to open banking. Open Banking Limited's Pay by Bank guide describes Pay by Bank as a way for customers to pay directly from their bank account, usually by choosing their bank, authenticating, and confirming the payment. It also notes that protections can differ from card payments, so merchants need to understand the specific rule set behind the flow.

For merchants, Pay by Bank can be attractive when customers trust their banking app, when card entry adds friction, or when the business wants a bank-account-funded payment option. But implementation should not start with a generic promise. Start with operational questions:

- Which markets and banks are covered?

- Is the customer redirected, embedded, or asked to scan a code?

- Is confirmation immediate or delayed?

- How are refunds initiated?

- What happens when authentication succeeds but payment confirmation is delayed?

- What support message should a customer see if the payment is pending?

Real-time payment networks

Real-time payment networks such as UPI and Pix are bank-account-based rails that can overlap with A2A and QR payment categories. They should still be evaluated as a separate operational category because confirmation, availability, refunds or returns, reconciliation, and fraud controls depend on the underlying rail.

Cryptocurrency and stablecoin payments

Some payment-industry taxonomies include cryptocurrency and stablecoin payments within alternative payment methods because the customer pays outside the standard card flow. The label is not universal. Merchants should compare the acceptance model, supported assets and networks, exchange-rate handling, settlement currency, refunds, transaction reversibility, wallet screening, AML and sanctions controls, and tax or accounting treatment. Availability and consumer protection vary by jurisdiction. Do not assume that a payment provider supports crypto unless current product documentation confirms it.

Local payment examples to evaluate

The best APM set depends on where your customers are. These examples are not a recommendation to enable every method. They are common method types that teams should evaluate when building a cross-border payment roadmap.

Market signal | Payment examples to evaluate | Why it may matter | Verification required |

|---|---|---|---|

Customers prefer bank-app or QR payment flows | PromptPay and Thai QR-style flows in Thailand | Bank of Thailand describes Thai QR Payment and PromptPay-connected use cases across personal, corporate, e-wallet, and cross-border contexts. | Confirm provider support, customer flow, refund process, settlement, and business eligibility |

Customers use local or regional card brands | JCB in Japan and broader Asia-focused acceptance contexts | JCB positions itself as a major payment brand with a large cardmember and merchant network, especially connected to Asia. | Confirm acquiring support, routing, currency handling, authentication, and dispute rules |

Customers expect domestic wallet or fintech checkout | Naver Pay in South Korea | NAVER describes Naver Pay as a financial platform that includes easy payment and other financial services. | Confirm acceptance model, redirect or app flow, refunds, settlement, and language requirements |

Customers are comfortable paying from bank accounts | Pay by Bank or A2A payments | Bank-based payment flows can reduce card-entry friction when customers trust the bank authentication flow. | Confirm rails, coverage, confirmation timing, refund route, and customer protections |

Customers need deferred payment options | Buy now pay later providers | BNPL can match purchase contexts where installment or deferred payment is part of customer expectation | Confirm provider approval rules, regulated messaging, refund liability, and settlement terms |

Customers prefer cash or offline confirmation | Voucher, convenience-store, or cash-reference payments | Offline flows can help reach customers who do not want to pay by card online | Confirm expiration windows, order reservation rules, payment confirmation timing, and support process |

Alternative payment methods by region: current signals

Payment behavior varies significantly by market. The figures below use different scopes and measurement methods, so they should not be compared as direct APM market-share estimates. Instead, use them as market signals when deciding which payment methods, customer flows, and operational capabilities require further validation.

Region / market | Current data signal | Merchant implication | Source |

|---|---|---|---|

Global / developing markets | In 2024, 42% of adults in low- and middle-income economies made an in-store or online digital merchant payment, up from 35% in 2021. | Do not apply one global payment-method mix to every market. Validate local preferences using checkout analytics, customer research, device behavior, and payment-provider documentation. | |

India / APAC | UPI processed approximately 23.20 billion transactions in May 2026 across 720 live banks. | Verify UPI merchant eligibility, supported banks, INR settlement, QR or app flow, payment confirmation, refunds, reconciliation, and provider coverage before launch. | |

Brazil / LATAM | By the fourth quarter of 2024, Pix accounted for nearly half—47%—of all non-cash payment transactions in Brazil. Pix transaction volume grew by 52% during 2024. | Merchants targeting Brazil should evaluate Pix alongside cards. Confirm merchant eligibility, BRL settlement, QR and account-based flows, instant confirmation, refunds, fraud controls, and reconciliation. | |

Euro area | In the first half of 2025, instant credit transfers accounted for 23% of the total number of credit transfers processed by euro-area retail payment systems. | Verify whether the provider supports SEPA Instant, sending and receiving capabilities, beneficiary verification, IBAN handling, transaction confirmation, fees, refunds, and reconciliation. | |

Sub-Saharan Africa | In 2024, 58% of adults owned a financial account, while mobile-money account use remained at the highest level in the world. | Evaluate mobile money at the country and operator level. Confirm phone-number flows, customer authentication, cash-in and cash-out dependencies, KYC requirements, reversals, settlement currency, and customer support. | |

Middle East and North Africa | Account ownership reached 53% of adults in 2024, up from 45% in 2021. | Treat the region as a group of distinct national markets. Verify local bank and wallet coverage, Arabic-language checkout requirements, customer authentication, KYC, local regulations, settlement, refunds, and consumer-protection rules. |

These figures show why APM selection should begin with market evidence rather than a provider’s full method catalogue. Before enabling a payment method, confirm customer demand, merchant eligibility, currency support, payment flow, settlement, refunds, disputes or reversals, reconciliation, regulatory requirements, and provider availability for the specific market.

If Hong Kong is one of your target markets, use this Hong Kong payment gateway guide to compare gateway, acquiring, settlement, and local-payment requirements.

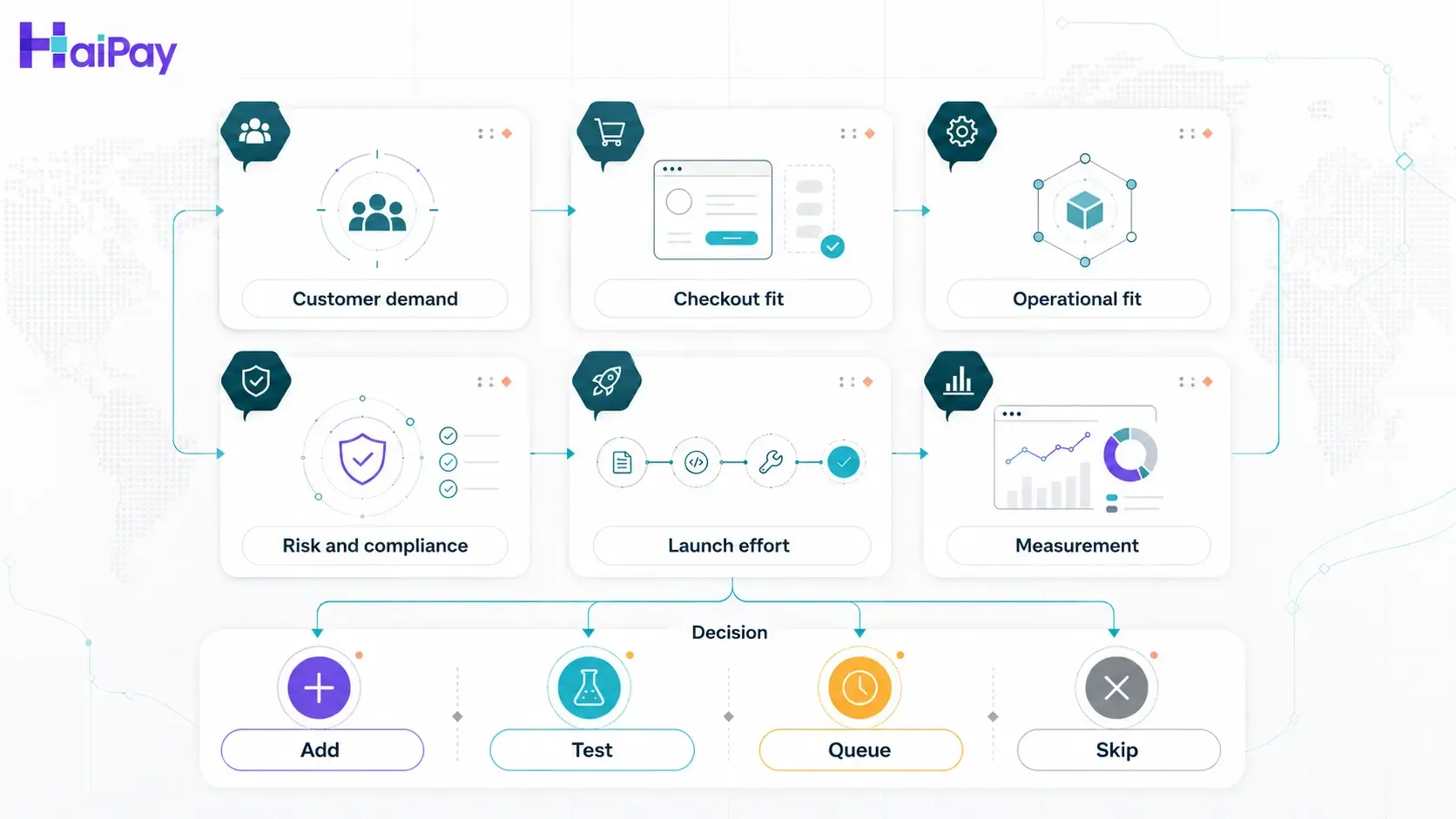

How to choose the right APMs by market

Use a decision matrix before adding payment methods to checkout. The point is to select methods with a clear customer and operational reason.

Decision factor | What to ask | Good signal | Caution signal |

|---|---|---|---|

Customer demand | Do customers in this market already use the method? | Search demand, local competitor adoption, customer interviews, support requests, payment provider guidance | "Competitors have it" is the only reason |

Checkout fit | Does the method match the device, basket size, and purchase context? | Mobile-first method for mobile-heavy market, wallet for repeat consumer checkout, bank-based flow for bank-trusting segment | Long redirect or delayed confirmation for a fast impulse purchase |

Operational fit | Can finance and support handle the payment states? | Clear payment statuses, refund process, reconciliation fields, and support macros | Pending, expired, refunded, and failed states are not mapped |

Risk and compliance | Are the rules understood? | Method-level documentation for authentication, disputes, KYC or merchant-category rules, and regulated messaging | Broad risk-reduction or dispute-elimination promises without source-specific validation |

Launch effort | Is the implementation proportional to the opportunity? | Provider support, test environment, reporting, and market coverage are available | Custom flow needed before demand is proven |

Measurement | Can success be measured? | Baseline conversion, payment-method share, failure rate, refund rate, support tickets, and settlement exceptions | No baseline and no owner for post-launch review |

This is where a checkout provider can help. A provider can simplify method access, hosted checkout design, routing, reporting, and payment-status handling. But each method still needs market, legal, risk, and operational validation before it becomes part of a live checkout.

Explore checkout implementation, then confirm method availability with the HaiPay payments team before making launch commitments.

Method availability can also depend on the acquiring route; compare local acquiring vs cross-border acquiring.

A practical APM rollout plan

Do not launch alternative payment methods as a one-time feature dump. Treat them as a portfolio that should be prioritized, tested, measured, and maintained.

1. Map customer markets and payment expectations

Start with the markets, customer segments, and transaction types that matter most. A merchant selling digital services in South Korea may evaluate different payment methods from a B2B platform expanding into Europe or a marketplace serving mobile-first shoppers in Southeast Asia.

Useful inputs include checkout analytics, abandoned-payment data, support tickets, sales feedback, market research, competitor checkout reviews, and payment provider coverage.

2. Prioritize methods by opportunity and complexity

Score each method against likely demand, coverage, implementation effort, settlement complexity, refund handling, support load, and compliance risk. A method with modest search volume but strong local buyer trust may outrank a globally known method with weak fit for your audience.

3. Design the checkout experience

Customers should understand what will happen when they select a method. If the flow redirects to a bank app, opens a wallet, shows a QR code, creates a pending order, or requires offline payment, the checkout should set expectations before the customer clicks.

Avoid generic labels when a clearer local label exists. Also avoid overloading the payment step with every method at once. Grouping, ordering, localization, and device-aware presentation can matter as much as the methods themselves.

4. Define payment states and support scripts

Every method needs a state model. At minimum, document what your team will show and do for:

- Payment created

- Customer redirected

- Customer authenticated

- Payment pending

- Payment succeeded

- Payment failed

- Payment expired

- Refund initiated

- Refund completed

- Dispute, reversal, or exception

Support teams should know what the customer saw, what status is authoritative, and when to ask payments or finance for help.

5. Confirm settlement, refunds, and reconciliation

Before launch, confirm the operational details with your provider. Do not assume a wallet, bank transfer, local scheme, and BNPL method behave like a card payment after checkout. Settlement timing, fees, refund routes, dispute windows, and reporting fields can differ.

Finance teams should know how each method appears in reports, how fees are represented, how currencies are handled, and how exceptions are investigated.

6. Launch with measurement

Track method adoption and quality after launch. Useful metrics include:

- Payment-method impressions

- Payment-method selection rate

- Authorization or confirmation success rate

- Drop-off after method selection

- Pending-payment completion rate

- Refund rate

- Support contact rate by method

- Settlement exceptions

- Checkout conversion by market and device

APMs should earn their place in checkout. If a method creates more confusion than completed payments, fix the UX, adjust ordering, localize the explanation, or remove it from low-fit segments.

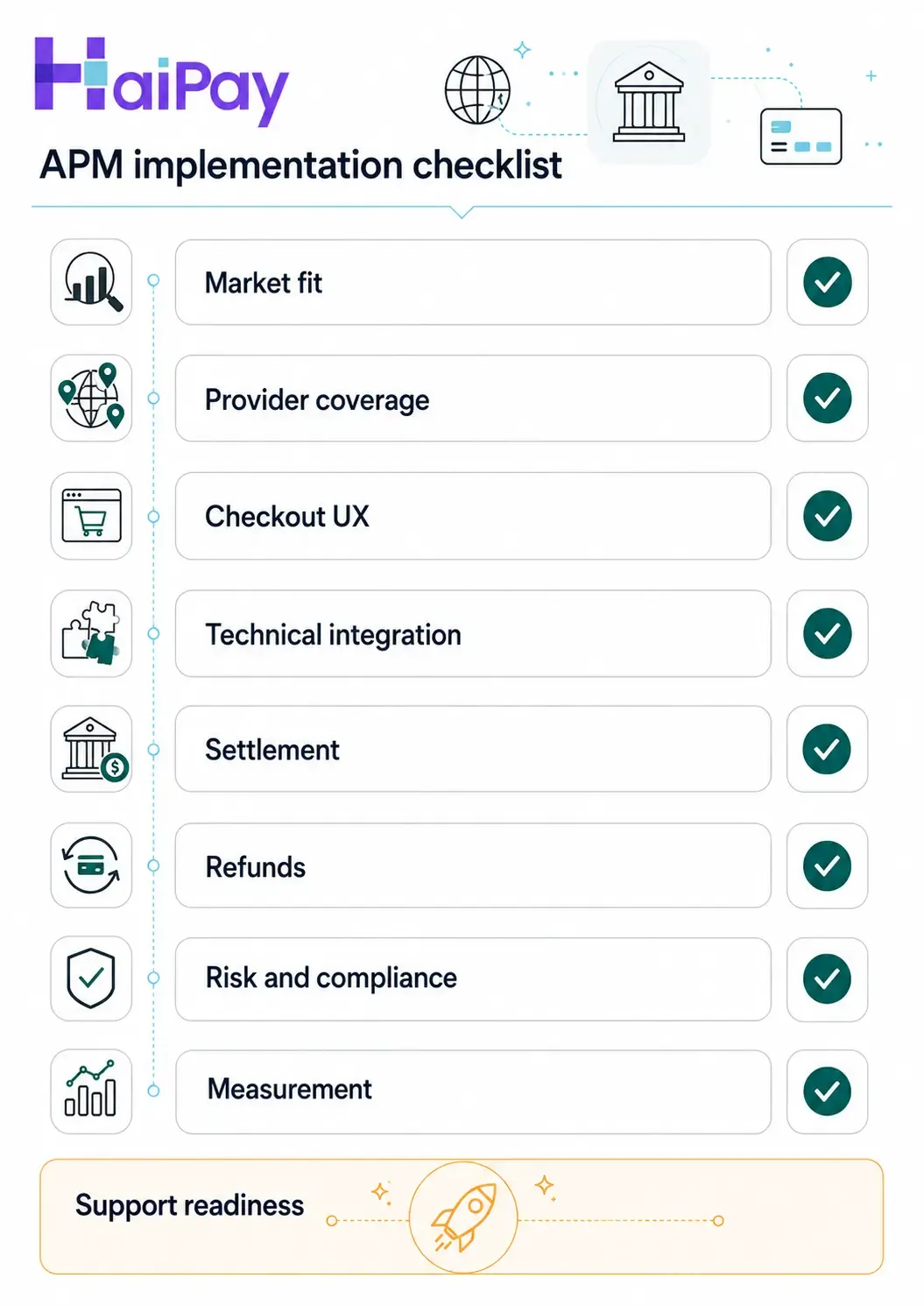

Implementation checklist

Use this checklist before enabling a new APM.

Area | Checklist item | Owner |

|---|---|---|

Market fit | Identify the target market, segment, and customer reason for the method | Product / Growth |

Provider coverage | Confirm the method is available for the merchant entity, region, currency, category, and customer location | Payments |

Checkout UX | Define label, placement, method grouping, redirect copy, QR copy, pending-state copy, and failure messages | Product / Design |

Technical integration | Confirm API, hosted checkout, webhook, payment-status, idempotency, testing, and fallback requirements | Engineering |

Settlement | Confirm settlement timing, reporting fields, fees, currency handling, and reconciliation workflow | Finance |

Refunds | Confirm refund route, partial refund support, customer notification, timing, and failure handling | Support / Finance |

Risk and compliance | Confirm authentication, dispute or reversal rules, prohibited categories, regulated messaging, and local requirements | Risk / Legal |

Support readiness | Create customer-facing explanations for pending, expired, failed, and refunded payments | Support |

Measurement | Define baseline, launch dashboard, review date, and success threshold | Growth / Analytics |

For HaiPay implementation planning, use HaiPay Checkout to evaluate the checkout path, then confirm method coverage with HaiPay internal documentation or product owners. Do not publish claims about specific method support until those details are confirmed.

When a checkout provider becomes useful

A single payment method can often be integrated directly. A growing cross-border checkout usually needs more structure.

Consider a checkout provider or payment orchestration approach when:

- You sell across multiple countries and need local payment methods.

- You need one checkout experience with market-specific payment options.

- You want reporting and reconciliation across several methods.

- You need to test method ordering, localization, and payment status handling.

- Your support and finance teams need consistent operational workflows.

- You want to add methods without rebuilding the checkout each time.

The provider decision should still be grounded in method coverage, integration quality, payment status clarity, settlement reporting, refund handling, compliance support, and customer experience. A broader method list is useful only if the business can operate it cleanly.

Talk to the payments team to validate the right APM mix for your markets and confirm method availability before implementation.

Common mistakes when adding alternative payment methods

Adding methods without a market reason

A long method list can slow decision-making and make checkout feel less trustworthy. Start with customer demand, not a provider catalog.

Treating every APM like a card payment

APMs can differ in confirmation timing, refunds, disputes, reversals, reporting, and customer communication. Build method-specific operating notes before launch.

Ignoring pending and expired payment states

Some methods may not complete in a single immediate authorization flow. If the customer leaves checkout, scans a code, pays offline, or confirms in a bank app, your system and support team need a clear status model.

Making unverified regional claims

"Popular in Asia" or "best for Europe" is too vague to be useful. Use market-specific research, provider documentation, and internal performance data.

Measuring only total conversion

Track method selection, drop-off after selection, payment success, pending completion, refunds, and support tickets. A method may improve trust for one segment while creating friction for another

Next step

Build the APM roadmap around the markets you serve, the customers you want to convert, and the operations your team can support. Then validate the method list with your provider before implementation.

- Explore HaiPay Checkout

- Confirm available payment methods with the HaiPay payments team

- Talk to the payments team to confirm the right payment mix for your business.

FAQ

Examples include digital wallets, Pay by Bank and other account-to-account payments, bank transfers, direct debit, buy now pay later, QR payments, local card schemes, vouchers, cash-reference payments, real-time payment networks, cryptocurrency and stablecoin payments where supported

and domestic fintech payment options. The right examples depend on the target market and customer segment.

Need help mapping your payment stack?

Talk to HaiPay about acquiring, orchestration, local methods, and payout workflows.

Contact us