Local Acquiring in Emerging Markets: What Global Businesses Should Know

Last updated: July 21st, 2026

Insights

A practical guide to local acquiring in emerging markets: what it covers operationally, why local payment methods matter, and how to assess when the transition from cross-border acquiring fits your expansion strategy.

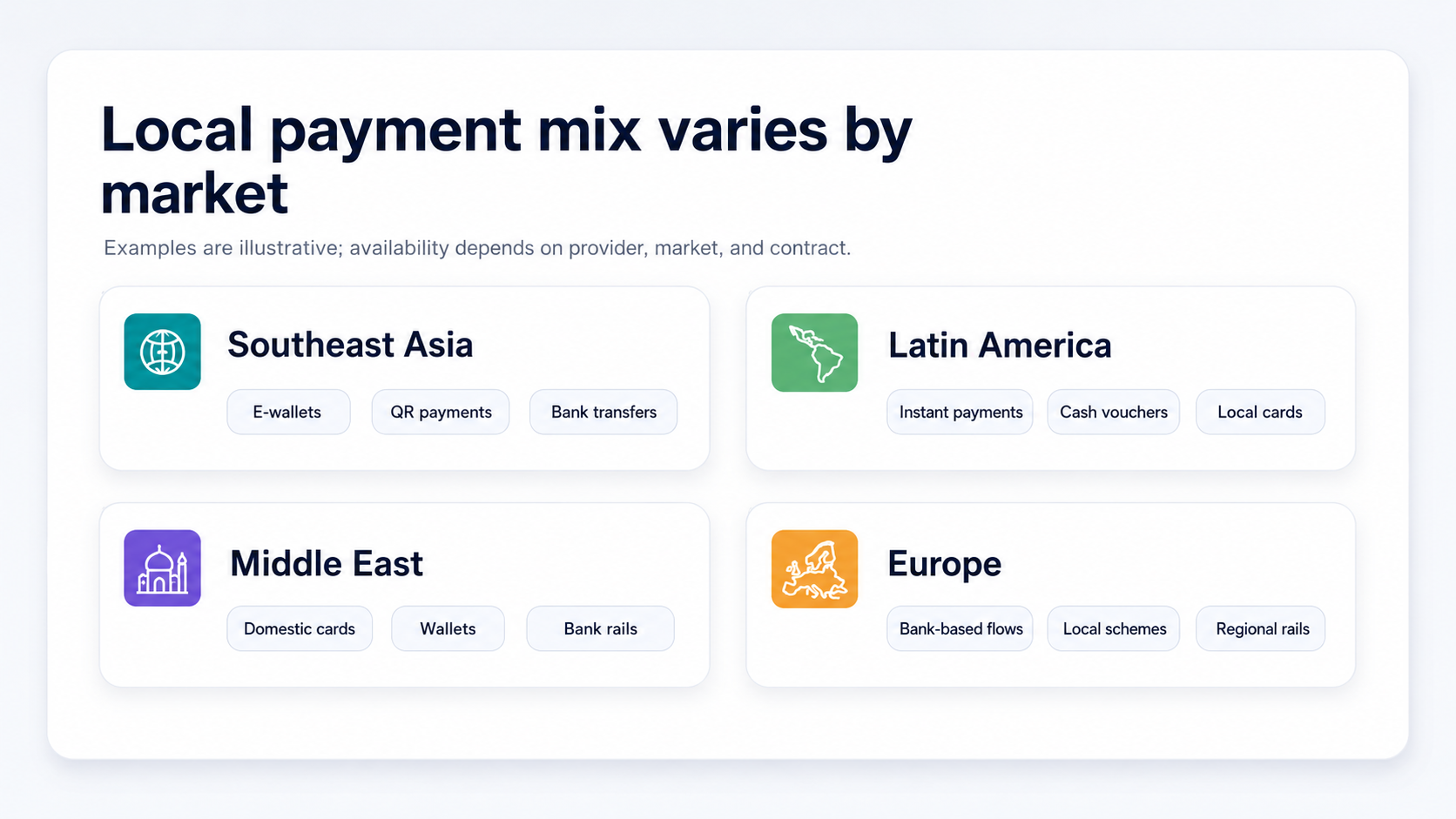

Merchants expanding into Southeast Asia, Latin America, the Middle East, and other high-growth regions often discover that payment infrastructure varies considerably across markets. In many emerging economies, a large share of consumers rely on local payment methods — domestic bank transfers, mobile wallets, QR-based schemes — that operate on networks separate from international card infrastructure. A card-only checkout approach may work in some markets but miss a significant portion of potential buyers in others.

Local acquiring — processing transactions through an acquirer licensed and operating in the customer's market — is one of the primary ways merchants gain access to these locally preferred methods and connect to domestic clearing networks. But it is not a universal upgrade, and the decision involves real trade-offs across licensing, compliance, and operational complexity.

For a structured comparison of local and cross-border models across cost, authorization, settlement, and compliance dimensions, the guide on local acquiring vs cross-border acquiring covers both structures in detail.

Why Emerging Markets Have Distinct Payment Needs

Payment behavior in emerging markets frequently diverges from what merchants are accustomed to in North America or Western Europe. The World Bank Global Findex documents meaningful variation in account ownership and digital payment adoption across regions, and GSMA mobile money resources show how mobile-led financial access has outpaced card penetration in several markets.

In practice, locally preferred payment methods are often the primary — not secondary — way customers pay online in these markets. In Brazil, Pix — the country's central bank-operated instant payment system — is widely used for e-commerce. In Indonesia, OVO and DANA are among the commonly used e-wallets. PromptPay is prevalent in Thailand; Mada and KNET are central to payment infrastructure in Saudi Arabia and Kuwait respectively.

Merchants processing through a cross-border acquirer may have access to international card networks but limited access to these domestic methods. That payment method coverage gap is typically the first and most important reason to evaluate local acquiring in a given market.

What Local Acquiring Covers Operationally

Local acquiring in emerging markets spans several interconnected operational dimensions — not just payment method access.

Acquirer coverage and licensing. Local acquiring requires an acquirer — or a payment provider aggregating local coverage — with the relevant licenses or authorizations in each target market. Licensing requirements vary significantly by country, and merchants should verify what coverage a provider actually holds in their specific target markets.

Payment method access. A locally licensed acquirer can connect to domestic clearing networks and locally issued payment schemes that are unavailable or limited through cross-border channels. This is usually the primary driver of the local acquiring decision in emerging markets.

Checkout localization. Effective localization includes local currency pricing, local language interfaces, and checkout flows adapted to regional expectations — factors that affect conversion independently of which acquiring model is in place.

Settlement timing. Domestic clearing may settle faster than cross-border clearing in certain markets, though actual settlement timing depends on the market, acquirer, payment method, and contract terms. Merchants should evaluate this on a market-by-market basis rather than assuming a single standard applies.

Compliance and risk. An acquirer operating under local regulatory frameworks applies local KYC, AML, and risk rules. This creates obligations for the merchant to understand local compliance requirements and how disputes and fraud are handled in each market.

Reconciliation complexity. Operating across multiple local acquiring relationships increases reconciliation overhead. Finance teams should assess whether they have the tooling to manage multi-market settlement reporting before expanding simultaneously to multiple local setups.

When Local Acquiring Warrants Evaluation

Cross-border acquiring is often the right starting point for testing a new market: it requires less upfront setup and avoids local entity and compliance overhead before demand is validated. The calculus shifts as volume grows or as payment method coverage becomes a concrete constraint.

Indicators that local acquiring may be worth evaluating:

- Local payment methods represent a significant share of how your target customers actually pay

- Cross-border authorization outcomes are materially below expectations and issuer behavior is a plausible contributor

- Settlement timing is creating working capital constraints

- Volume and long-term market commitment justify the compliance and operational investment

The right evaluation point depends on your volume, margin structure, and what local setup requires in the specific market. The cross-border acquiring fees overview and local payment acquiring for ecommerce article can help frame the cost and operational considerations more concretely before making this assessment.

How HaiPay Supports Local Acquiring in Emerging Markets

HaiPay's payment acquiring solution is designed to support merchants seeking local acquiring coverage across multiple emerging markets without managing individual market relationships separately. Its HaiPay acquiring infrastructure helps merchants evaluate local payment and acquiring coverage across supported markets, including selected local clearing networks and locally preferred payment methods where available.

Payment method examples include OVO and DANA in Indonesia, PromptPay in Thailand, Boleto and Pix in Brazil, SPEI in Mexico, and Mada and KNET across parts of the Middle East. These are illustrative examples — actual payment method availability in a specific market depends on configuration, local authorization status, and applicable conditions.

For merchants at earlier expansion stages, the cross-border payment solution provides card and international coverage while local acquiring relationships are being established. HaiPay's public materials highlight 24/7 live agent service, multilingual checkout support, and no setup fees for eligible merchants; actual availability and commercial terms should be confirmed by market and contract.

Conclusion

Local acquiring in emerging markets is a meaningful infrastructure decision, not a default upgrade. The right approach depends on which markets you are entering, how customers actually pay there, the volume and commitment level you have established, and what local compliance obligations apply.

For a full framework comparing local and cross-border acquiring models — covering cost, authorization potential, settlement, and operational readiness — the guide on local acquiring vs cross-border acquiring is a practical starting point.

To explore HaiPay's local acquiring coverage and payment method access for specific markets, visit the payment acquiring solution page or review the global acquiring overview.

FAQ

Local acquiring means your transactions are processed by an acquirer — a bank or licensed payment institution — that operates in the same country or region as your customer. In emerging markets, this typically enables access to locally preferred payment methods on domestic networks, which are often inaccessible through a cross-border acquiring setup.