Cross-border Acquiring Fees: What Merchants Need to Understand

Reviewed by Weijun Tang

Last updated: July 24th, 2026

Insights

Break down the cost components behind cross-border acquiring fees — from interchange and FX to scheme assessments and settlement — and learn the right questions to ask before comparing provider quotes.

When you expand into new markets, payment processing costs can vary more than most merchants expect. Cross-border acquiring introduces multiple fee layers that don't exist in purely domestic transactions — and because providers present these costs differently, comparing quotes without a clear framework leads to poor decisions.

This article breaks down the cost components behind cross-border acquiring, explains where local acquiring may reduce certain fee layers, and gives your team the right questions to ask before committing to a provider.

For a broader look at the acquiring model decision — including how authorization, settlement, and compliance interact — see the local acquiring vs cross-border acquiring guide.

What Are Cross-border Acquiring Fees?

Cross-border acquiring fees are the costs a merchant incurs when a payment is processed by an acquirer in a different country from the cardholder. The BIS cross-border payments programme identifies cost as one of the core frictions in international payments — and for merchants, that friction is distributed across a stack of charges from multiple parties: card networks, issuing banks, acquiring banks, and sometimes intermediary processors.

Understanding what you're paying requires separating these components rather than accepting a single blended rate at face value.

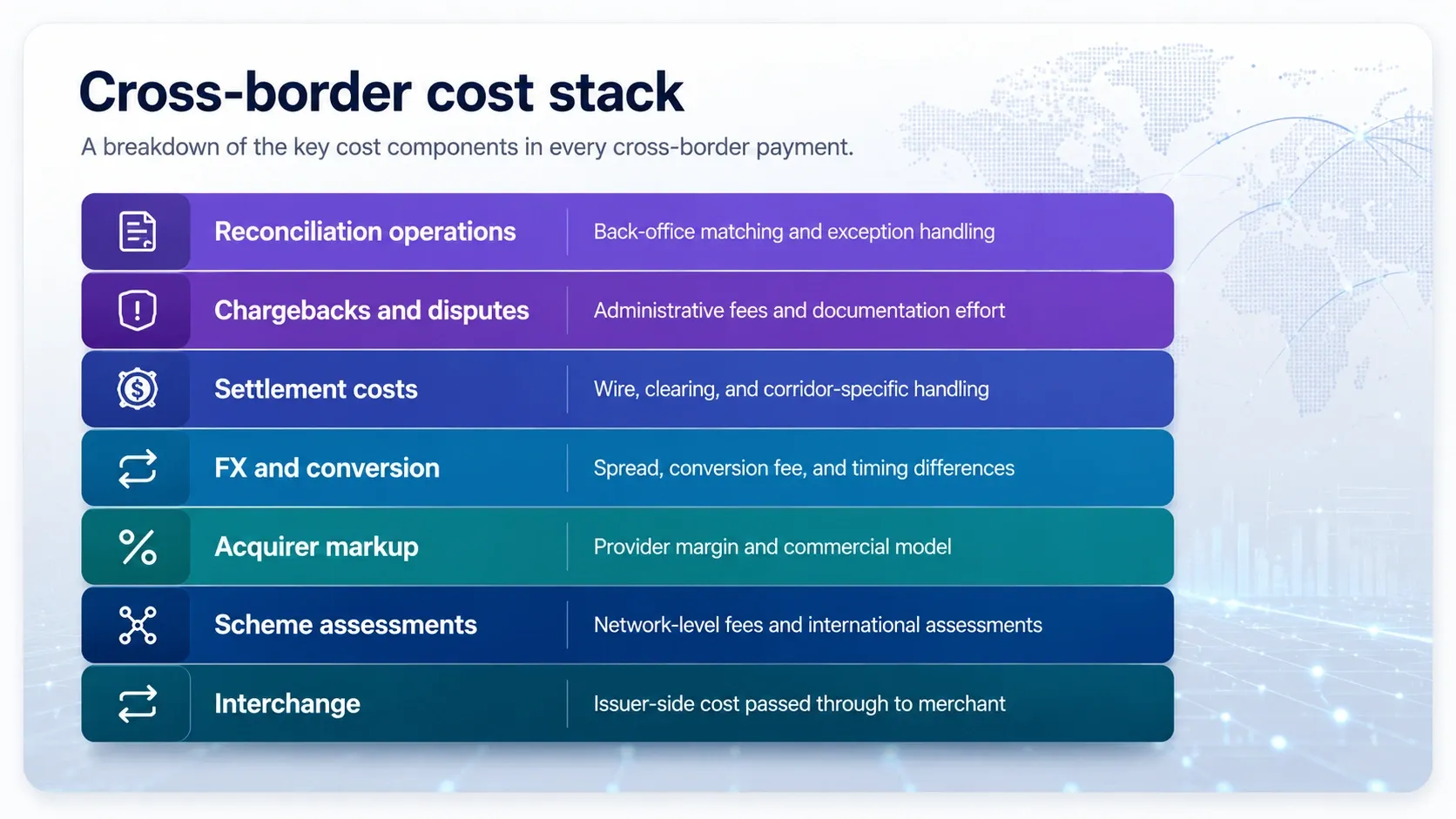

The Main Cost Components

The table below summarizes the seven cost components explained in this section — who charges each one, how cross-border differs from domestic, and what to clarify before signing.

Cost component | Who charges it | Cross-border vs domestic | How it appears in pricing | What to ask the provider |

|---|---|---|---|---|

Interchange | Card issuer (via acquirer) | Often set at a higher tier for cross-border transactions | Passed through; visible under interchange-plus, hidden in blended rates | Which interchange tiers apply to your card mix and corridors |

Scheme & network assessments | Card networks | International service assessments may apply on top of domestic fees | Separate line under interchange-plus; bundled otherwise | Which assessments apply to acquiring vs issuing side |

Acquirer markup | Acquiring bank / processor | Largest variation between providers | Flat rate, percentage, or blended | Ask for margin separated from network costs |

FX & currency conversion | Provider / bank in the chain | Only arises when transaction, settlement, or billing currencies differ | Spread over a reference rate plus explicit conversion fees | Which reference rate, fixed or variable spread, number of conversions |

Settlement costs | Banks / correspondents | Wire and correspondent charges added by cross-border routing | Per-settlement fees; sometimes bundled | Multi-currency settlement availability and terms |

Chargeback & dispute costs | Acquirer + networks | Higher administrative cost across jurisdictions; threshold program fees | Per-chargeback fee plus conditional monitoring fees | Per-chargeback cost and threshold triggers for cross-border volume |

Reconciliation & operational costs | Internal (indirect) | Multi-currency, multi-file data multiplies manual effort | Not on the invoice — appears in your finance team's hours | Reporting formats, consolidation, and automation support |

Interchange

Interchange is a fee paid by the acquirer to the card issuer, typically passed through to the merchant. For cross-border transactions, card networks often set interchange at a higher tier than for domestic transactions. The difference depends on the network, card type, merchant category code, and the countries on each side of the transaction. Networks publish interchange schedules, but mapping them to your actual transaction mix requires analysis against your specific portfolio.

Scheme and Network Assessments

Card networks charge their own fees on top of interchange. For cross-border transactions, networks may apply additional assessments — sometimes called international service assessments — that do not apply to domestic transactions. These vary by network and may apply to the acquiring side, the issuing side, or both.

Acquirer Markup

The acquiring bank or processor adds a margin above interchange and scheme costs. This is often where the most variation exists when comparing provider quotes. Markups may appear as a flat per-transaction rate, a percentage of transaction value, or a blended rate. Interchange-plus pricing structures expose this margin separately from network costs, which flat-rate or blended models can obscure.

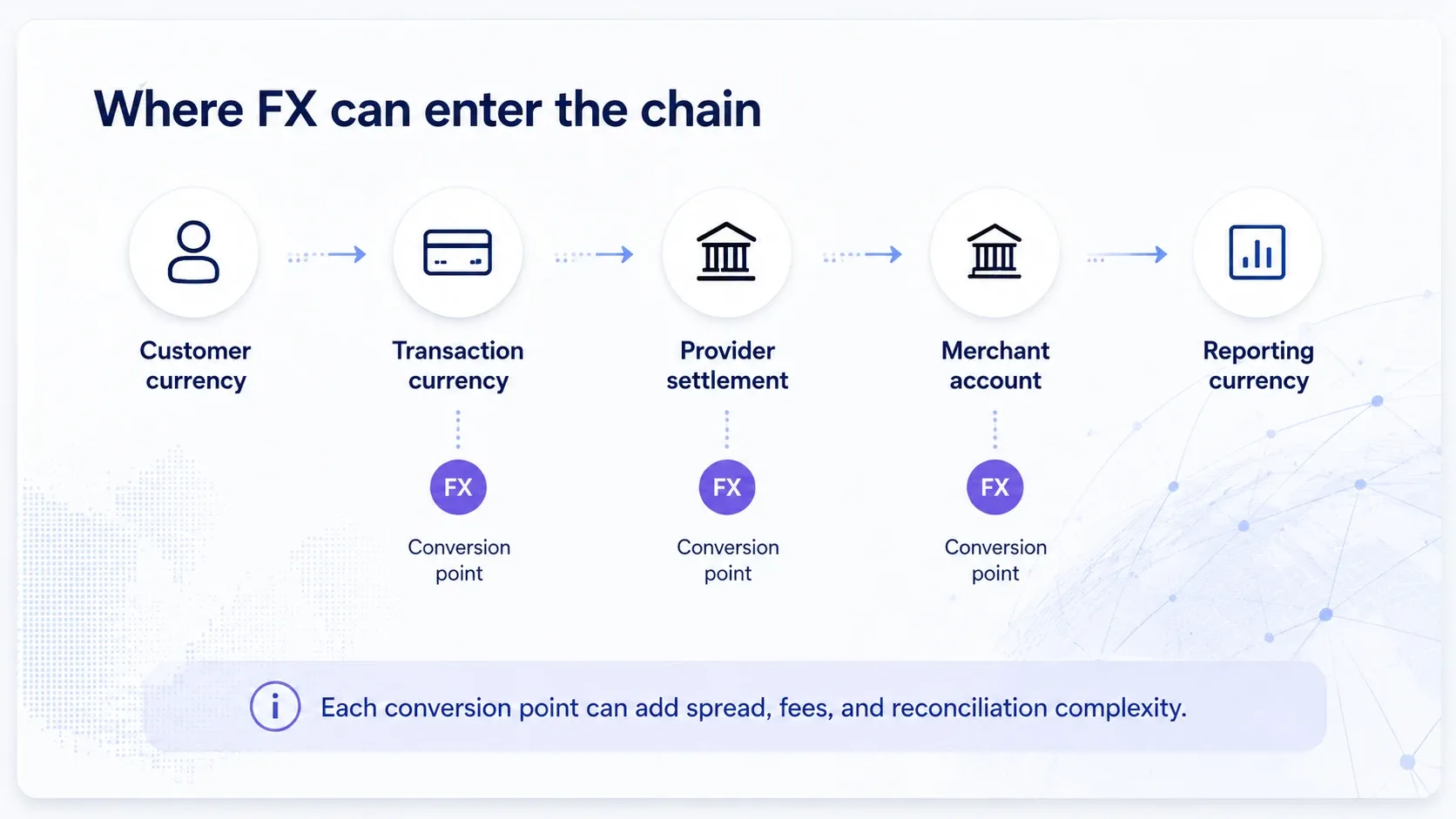

FX and Currency Conversion

When transaction currency differs from settlement currency — or from the cardholder's billing currency — foreign exchange conversion is applied at some point in the chain. FX costs include both the spread applied to a reference rate and any explicit conversion fees. Multiple conversions within a single payment chain can compound these costs.

Dynamic currency conversion (DCC), where a cardholder is offered the option to pay in their home currency at checkout, introduces an additional fee layer and must be disclosed under card network rules.

Settlement Costs

Cross-border settlement may incur wire fees, correspondent banking charges, or processing delays associated with routing funds across currency systems. Some providers offer multi-currency settlement accounts that can reduce the number of conversion events, though the terms and available currency pairs vary by provider and market.

Chargeback and Dispute Costs

Chargebacks in cross-border transactions can carry higher administrative costs, particularly when dispute resolution spans different regulatory jurisdictions. Most acquirers charge a per-chargeback fee, and if your ratio exceeds network thresholds, additional monitoring program fees apply. These costs are often underestimated in total cost of acceptance calculations.

Reconciliation and Operational Costs

Cross-border transaction data often arrives in multiple currencies, across multiple settlement files, from multiple acquirers or processors. Finance teams that handle this manually absorb meaningful time and error costs that should be factored into any full cost of acceptance comparison.

Published rate reference points

Most cross-border cost components are set in acquirer-specific contracts rather than public price lists. The table below collects the few figures that networks and major PSPs do publish — use them as orientation points when reading a quote, not as your expected total cost. Figures verified as of July 24, 2026.

Layer | Published figure | Scope & effective date | Source |

|---|---|---|---|

Mastercard cross-border assessment | 0.60% (CAD-denominated) – 1.00% (non-CAD) charged to acquirers, on top of a 0.090% acquirer volume assessment | Canada acquiring; effective July 1, 2025. The non-CAD tier carries a merchant-POI dynamic currency conversion qualifier in the source document | |

Visa international assessments (ISA / IAF) | Not published in a unified public rate card | Rates reach merchants through acquirer disclosures — ask your acquirer for the pass-through breakdown | — |

Stripe international card surcharge | +1.5% on top of the 2.9% + US$0.30 base rate; +1% more where currency conversion applies | US accounts, standard published pricing; checked July 24, 2026 | |

Adyen card pricing | US$0.13 per transaction + interchange and scheme fees passed through at cost + 0.60% markup (Visa/Mastercard, Global) | USD price list; cross-border network assessments arrive via Interchange++ pass-through; checked July 24, 2026 | |

HaiPay card pricing | 2.5% + US$0.30 blended (or itemized Interchange++ for high-volume merchants); local payment methods from 0.8%; cross-border and currency conversion are quote-confirmed based on contracting entity region and settlement currency | Published pricing, no setup or monthly fees; checked July 24, 2026 |

Network assessments are revised on the card networks' own fee calendars, and PSP list prices change without notice — treat every published number as a snapshot, and confirm current schedules directly with your acquirer or provider before modeling costs.

Local Acquiring and Cost Layers

Local acquiring — where the transaction is processed by an acquirer licensed and operating in the customer's country — can reduce certain cost components in specific markets. When an acquirer operates domestically, some cross-border interchange tiers and international network assessments may not apply. FX exposure may also be reduced if settlement occurs in local currency before any cross-border transfer.

However, local acquiring is not uniformly cheaper. Whether it results in a net cost saving depends on:

- The specific market and how card networks classify transactions there

- The acquirer's local pricing structure and bank partnerships

- Your transaction volume and merchant category

- Whether local entity requirements or compliance setup costs factor into total cost

- The payment methods you need to support and how they are priced locally

In some markets, local acquiring may offer meaningful cost efficiency. In others, cross-border acquiring through a well-structured provider may remain competitive. A useful comparison requires actual quotes against your specific transaction mix, not general assumptions about which model is cheaper.

Questions to Ask Before Comparing Acquiring Quotes

Before accepting a cost proposal from any provider, your team should work through the following:

- What is the pricing model? Interchange-plus, flat rate, or blended? Interchange-plus makes the acquirer's margin visible separately from network costs.

- Which fee components are in the quote? Ask for a breakdown separating interchange, scheme fees, acquirer markup, FX spread, settlement fees, and chargeback fees.

- What FX rate is applied, and when? Ask whether the rate references the network mid-rate, an interbank rate, or a provider-defined rate — and whether the spread is fixed or variable.

- How many currency conversions occur before settlement? Fewer conversion steps generally reduce FX costs, but this depends on your banking setup and the markets involved.

- What are the chargeback and dispute fees? Ask for per-chargeback cost and any threshold-triggered fees specific to cross-border volume.

- What compliance and onboarding requirements apply? Cross-border processing often involves customer due diligence obligations — including under frameworks such as the FinCEN customer due diligence rule — that can affect onboarding timelines and ongoing operational costs.

- Are there volume-based pricing tiers? Understand at what volume levels pricing may be renegotiated and whether projected growth changes the cost picture.

Evaluating Your Acquiring Options

HaiPay's payment acquiring solution is designed to support merchants evaluating acquiring coverage across multiple supported markets, with local payment method access and local network connectivity available in selected markets — including methods such as PromptPay, iDEAL, Pix, and Mada — across key markets. HaiPay Acquiring can provide a unified acquiring layer for eligible merchants, with multi-currency settlement options available depending on market, currency, payment method, and contract terms. The cross-border payment solution addresses merchants who need structured cross-border payment handling without building separate acquirer relationships per market.

Actual costs depend on your transaction mix, target markets, card types, and contract terms. For context on how the models compare in practice, see global acquiring vs local acquiring and local acquiring in emerging markets.

Next Steps

Cross-border acquiring fees are a multi-layer cost stack. Interchange, scheme assessments, acquirer markup, FX, settlement, chargebacks, and reconciliation each contribute — and each can be reduced with the right provider structure and market approach. Local acquiring can help in specific markets, but it is not a universal cost solution. The right starting point is a detailed breakdown of what you are actually paying and why.

For the full framework on acquiring model selection, return to the local acquiring vs cross-border acquiring guide. To explore HaiPay's acquiring options, visit the payment acquiring solution page.

FAQ

Cross-border acquiring fees are the costs a merchant pays when a payment is processed by an acquirer in a different country from the cardholder. They typically include interchange, card network assessments, acquirer markup, FX conversion costs, settlement fees, and chargeback costs — applied by different parties in the payment chain, not as a single line item.