Global Acquiring vs Local Acquiring: How to Choose the Right Model

Last updated: July 21st, 2026

Insights

Global acquiring and local acquiring represent different operating models for payment processing. This guide compares them across coverage, integration, fees, settlement, and compliance to help you choose the right fit.

When you accept payments from customers in multiple countries, how and where those payments are acquired has meaningful consequences for authorization outcomes, checkout experience, settlement timing, fees, and compliance exposure. Two of the most important models to understand are local acquiring and global acquiring — and knowing when each model fits your business is a practical question, not an abstract one.

For a broader look at how these models relate to your expansion strategy, see our guide on local acquiring vs cross-border acquiring.

What is local acquiring?

Local acquiring means your transactions are processed by an acquirer — a licensed bank or payment institution — that operates in the same country or region as your customer. When a buyer in Thailand pays on your checkout, a locally licensed acquirer in that market processes and clears the transaction through domestic clearing networks.

Because the acquiring entity operates under the regulatory framework of the customer's market, the transaction is typically treated as a domestic payment from the issuing bank's perspective. This can influence how the issuer evaluates the authorization request, which payment methods are available at checkout, how funds settle, and which compliance rules apply.

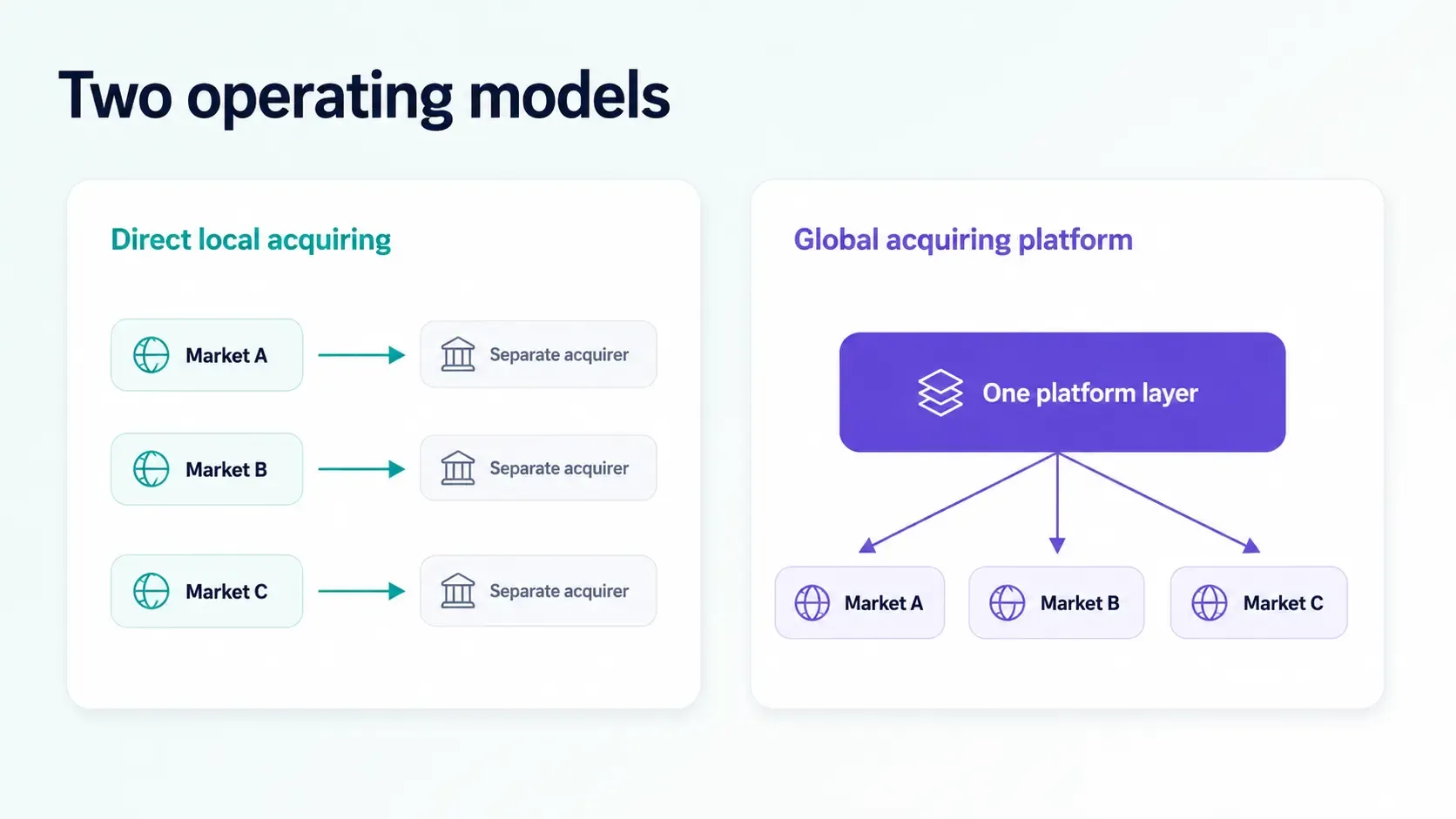

Operating through local acquiring across multiple markets generally requires either direct relationships with local acquirers in each country or working with a payment acquiring solution that aggregates local coverage under one contract and integration.

What is global acquiring?

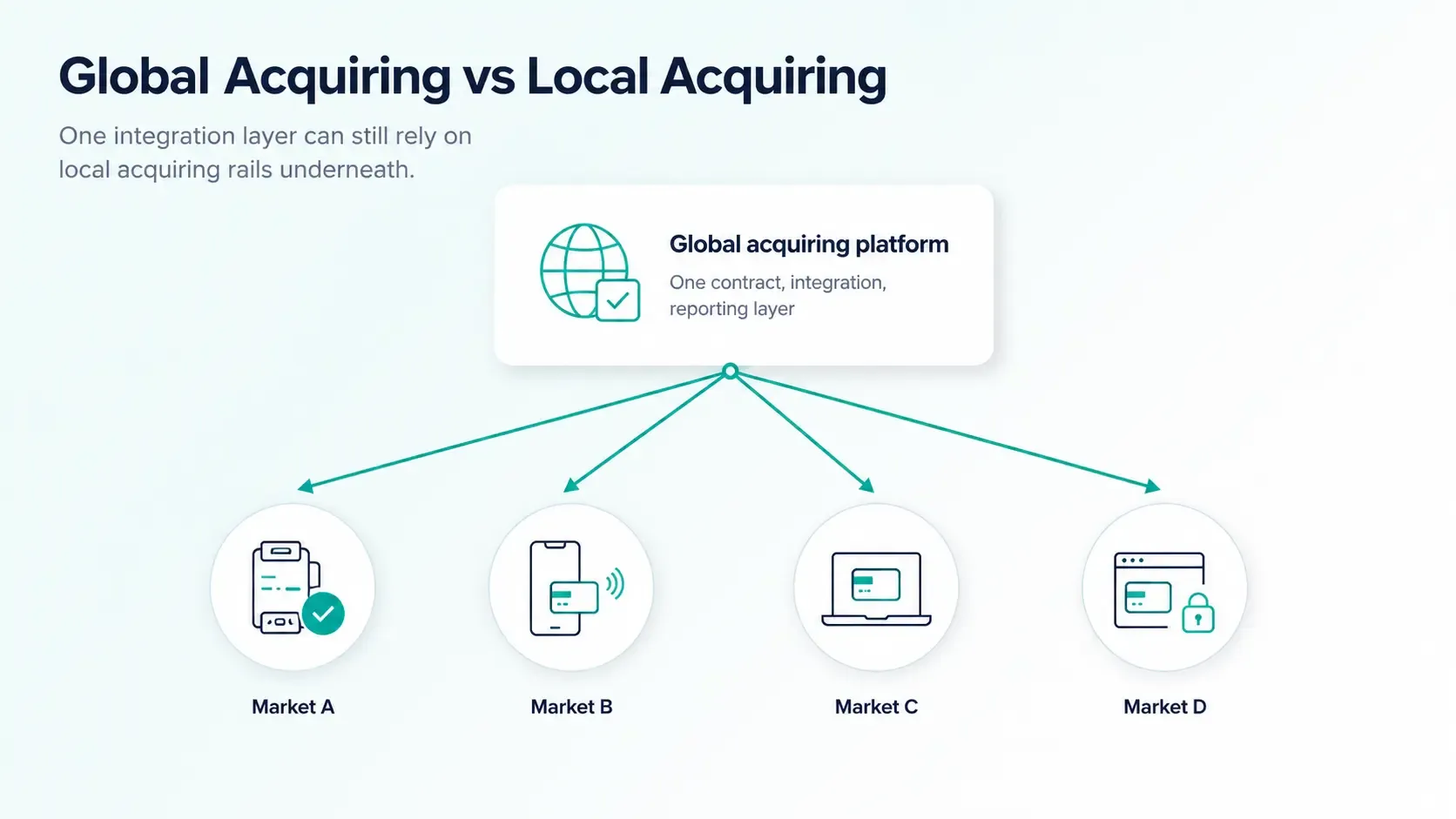

Global acquiring refers to a model where a single provider gives merchants access to local acquiring infrastructure across multiple markets under one platform layer. Rather than building separate local acquirer relationships market by market, merchants connect once and gain access to local processing, local payment methods, and local clearing networks in the regions the provider covers.

The term is sometimes used loosely — it can describe a centralized cross-border acquirer, a multi-local acquiring platform, or a hybrid of the two. For practical purposes, what matters is whether the provider processes transactions through locally licensed entities in each market, or routes them cross-border through a single offshore acquirer. The answer determines how issuers treat those transactions and which payment methods are actually accessible.

A global acquiring platform that uses genuine local infrastructure in each covered market gives merchants access to locally preferred payment methods, local currency settlement, and local issuer treatment — without requiring separate legal entities or acquirer contracts in every country.

Global acquiring vs local acquiring: how they compare

Dimension | Direct local acquiring | Global acquiring platform |

|---|---|---|

Coverage | One market per acquirer relationship | Multiple markets through one provider |

Integration effort | Separate integration per acquirer | Single integration with multi-market access |

Local payment methods | Full access where the acquirer is licensed | Depends on the provider's local network; confirm per market |

Authorization behavior | Issuer typically treats as domestic payment | Depends on whether the provider acquires locally or cross-border in each market |

Fees | May reduce cross-border interchange; depends on contract and market | Varies by provider; consolidated overhead may lower operational cost |

Settlement | Domestic clearing timelines per market | Depends on provider's local banking infrastructure in each market |

Compliance | Merchant manages obligations per-market | Provider handles local licensing; merchant retains its own compliance obligations |

Operational overhead | High — separate contracts, reconciliation, and reporting per acquirer | Lower — centralized reporting, reconciliation, and support |

Best fit | High-volume merchants in specific priority markets | Merchants entering or scaling across multiple markets simultaneously |

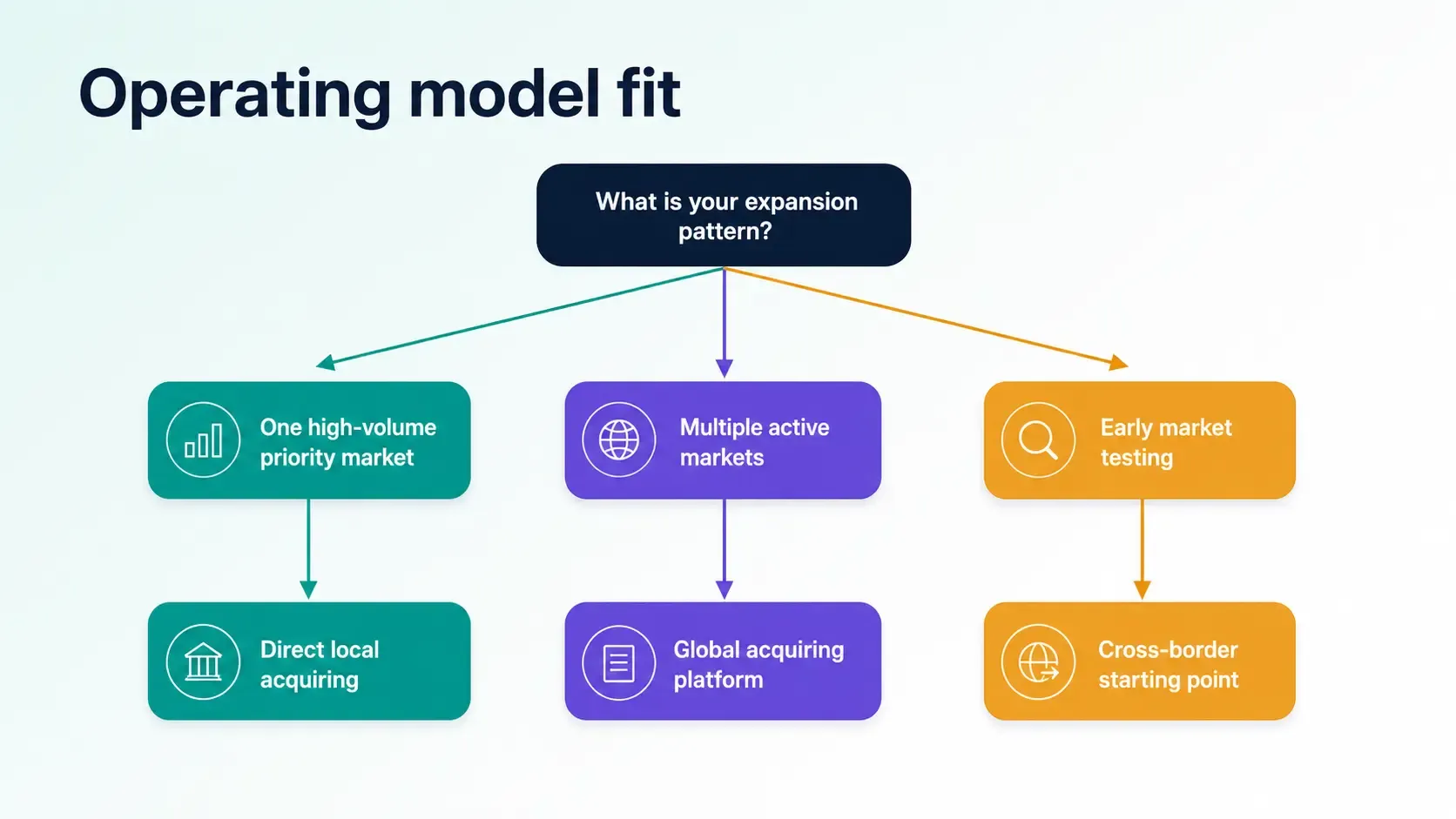

When direct local acquiring makes the most sense

Direct local acquiring tends to be the more practical choice when:

- Your transaction volume in a specific market is large enough to justify a dedicated acquirer relationship and the commercial terms that come with it

- You need deep customization or negotiated rates that require a direct contract

- You are operating in a market with regulatory requirements that favor or require local legal entities

- Your internal payments team has the capacity to manage multiple acquirer integrations, contracts, and reconciliation workflows

In these cases, investing in a direct relationship with one or more local acquirers can make economic and operational sense. The difficulty arises when replicating this model across many markets simultaneously — it quickly becomes resource-intensive to maintain.

When global acquiring is more practical

Global acquiring tends to make more operational sense when:

- You are entering or actively selling in multiple markets and need coverage without establishing local entities in each one

- You need access to locally preferred payment methods — such as OVO or DANA in Southeast Asia, iDEAL in the Netherlands, Boleto or Pix in Brazil, or Mada in Saudi Arabia — without building and maintaining separate integrations per provider

- Your payments team has limited capacity to manage multiple acquirer contracts, reconciliation systems, and local compliance obligations

- You want centralized reporting, settlement, and support across markets rather than managing each provider independently

When evaluating a global acquiring provider, the key due-diligence question is how they process transactions in each market: through locally licensed infrastructure or through cross-border routing. The BIS cross-border payments programme underscores why multi-local infrastructure design matters for reducing friction in international payments. Regional frameworks like SEPA in Europe further illustrate how local and regional acquiring rules shape what merchants can and cannot do in specific jurisdictions.

How HaiPay supports global acquiring

HaiPay's global acquiring model is designed around local infrastructure in the markets it serves. The platform supports pay-ins across 50+ countries and regions — including markets across Southeast Asia, Europe, the Middle East, Latin America, North America, and the Asia-Pacific — with access to 100+ integrated payment methods.

For merchants, this means local wallets, bank transfers, domestic card schemes, and real-time payment networks are available through a single integration rather than through separate provider relationships. Settlement is managed through local banking infrastructure where it is available in a given market, and reconciliation is automated across currencies.

The platform is built for businesses that need multi-market coverage without the operational overhead of managing separate local acquirer relationships. It requires no setup fee, and support is available 24/7. For merchants building a cross-border payment solution or evaluating multi-market checkout, the right starting point is mapping your specific target markets against the provider's local coverage and confirming payment method availability market by market.

Choosing the right model

The decision between direct local acquiring and a global acquiring platform comes down to market priorities, transaction volume, internal operational capacity, and speed of expansion.

For merchants scaling across multiple markets at once, a global acquiring platform that uses genuine local infrastructure typically offers a more efficient path than building acquirer relationships one market at a time. For merchants with concentrated, high-volume presence in specific markets, direct local acquiring relationships may offer more tailored commercial terms and control.

In either model, the underlying question is consistent: is the transaction being processed by an acquirer operating in the customer's market, or cross-border? The answer shapes authorization behavior, payment method access, settlement timing, and compliance obligations. For a detailed breakdown of the cost side, see our article on cross-border acquiring fees. For the ecommerce-specific angle, see local payment acquiring for ecommerce.

Our full guide to local acquiring vs cross-border acquiring covers these trade-offs in depth across all the dimensions that matter for global expansion decisions.

Assess your acquiring options with HaiPay

HaiPay's payment acquiring solution covers 50+ countries and regions with local infrastructure, 100+ integrated payment methods, and no setup fee required. Contact us or explore the global acquiring page to evaluate coverage for your target markets.

FAQ

Global acquiring refers to a model where a single platform provides merchants with access to local payment acquiring infrastructure across multiple markets, under one integration and contract layer. The term is used differently by different providers — what matters in practice is whether transactions in each market are processed by locally licensed entities, not just routed through a centralized offshore acquirer.