Payment Facilitator vs Merchant Acquirer: What's the Difference?

Last updated: July 21st, 2026

The key thing to understand: a payment facilitator and a merchant acquirer aren't competitors — they're a stack. A merchant acquirer, or acquiring bank, is the financial institution registered with the card networks that ultimately holds the merchant account and carries the final risk. A payment facilitator (PayFac) sits underneath an acquirer, using a master merchant account the acquirer provides to onboard sub-merchants.

In other words, a PayFac can't exist without an acquirer behind it.

This is part of our payment facilitator series. For the full model, see the guide.

What is a merchant acquirer?

A merchant acquirer is a financial institution that's a registered member of the card networks, such as Visa and Mastercard. It provides merchant accounts, enables card acceptance, and is ultimately responsible for the movement of funds and any losses.

When you hear "acquiring bank," this is the entity at the base of the stack.

Read more: Merchant Acquiring Guide

What is a payment facilitator?

A PayFac partners with an acquirer to obtain a master merchant account and MID, then onboards businesses as sub-merchants underneath it.

The PayFac handles day-to-day underwriting, onboarding, and sub-merchant risk — but it operates under the acquirer's registration.

A PayFac also differs from an ISO, which only refers merchants without taking on risk — see PayFac vs ISO.

Read more: Payment Facilitator Guide

How they work together

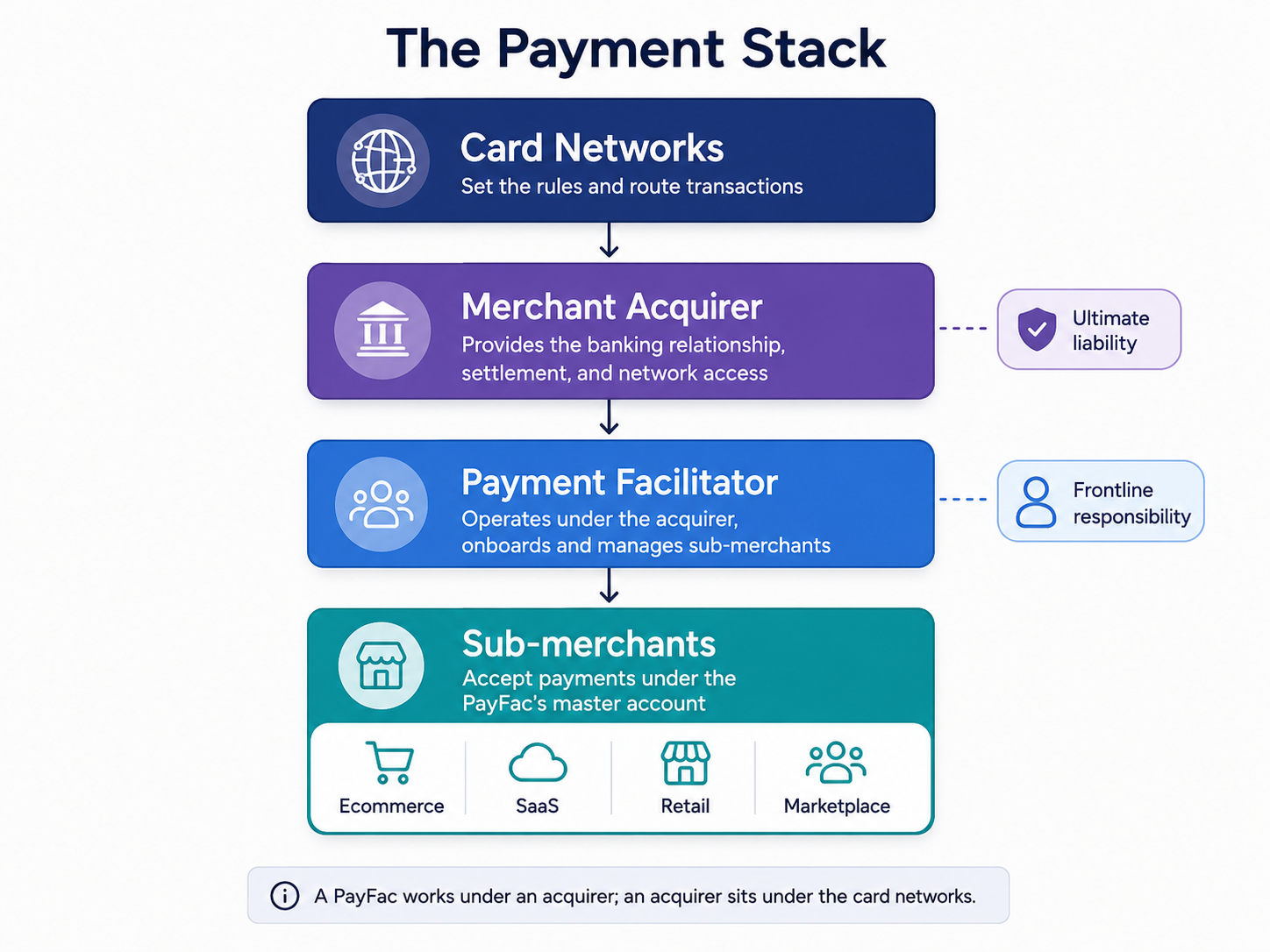

Think of it as layers, from the card networks down to the merchant:

- Card networks — Visa and Mastercard set the rules.

- Merchant acquirer — registered network member; holds the banking relationship and ultimate risk.

- Payment facilitator — operates under the acquirer; onboards and manages sub-merchants.

- Sub-merchants — accept payments under the PayFac's master account.

The acquirer carries the ultimate liability; the PayFac carries the frontline, day-to-day responsibility for its sub-merchants. Even when a sub-merchant grows large enough to sign a direct agreement with the acquirer, the PayFac typically stays on the frontline for that merchant's behavior.

Side-by-side comparison

Payment facilitator (PayFac) | Merchant acquirer | |

|---|---|---|

Card-network status | Registered PayFac under an acquirer | Registered network member |

Holds the banking relationship | No, uses the acquirer's | Yes |

Ultimate risk / liability | Frontline for sub-merchants | Ultimate |

Onboards sub-merchants | Yes | Not directly; works via PayFacs, ISOs, or merchants |

Capital and registration burden | High | Highest, because it is a bank or network member |

Customer-facing | Yes, to sub-merchants | Usually no |

When to deal with an acquirer directly

You would usually deal directly with an acquirer if you're a single, larger merchant that wants its own dedicated merchant account and more control.

This route can make sense when the business has enough processing volume, operational maturity, and compliance readiness to manage a more direct relationship with the acquiring side.

When to use a PayFac

You would usually work with a PayFac, or a PayFac-as-a-Service model, if you're a SaaS platform, marketplace, or smaller business that wants fast onboarding and less compliance overhead.

The PayFac model is designed to make payment acceptance easier for many smaller businesses underneath one master structure.

The in-between case

The right answer often depends on whether your markets are cards-first, or whether you need many local payment methods across countries.

A company may not need to become a PayFac or contract directly with one acquirer if the real problem is broader: accepting the payment methods customers already use in each local market.

The cross-border angle

Here's what neither "PayFac" nor "single acquirer" automatically solves: getting paid across many countries.

A single acquirer rarely reaches every market, and the card-network PayFac model is built around cards — not the local payment methods that dominate in many regions.

That's the job of cross-border local acquiring: a provider that already has the local methods, clearing, and licensing in each market.

Read more: Local Acquiring vs Cross-Border Acquiring

HaiPay is a licensed payment provider — regulated across the Philippines, Indonesia, the US, and Canada — that facilitates cross-border local acquiring with local payment methods across its supported markets: Pix in Brazil, GCash and GoPay in Southeast Asia, UPI in India, Mada/STC Pay in the Middle East, plus international card payments and local payout.

See how cross-border local acquiring works: Pay-ins Acquiring

Last updated June 2026.

Sources

- Visa — Merchant Payment Providers:usa.visa.com/supporting-info/merchant-payment-providers.html

- Mastercard — Payment Facilitators:mastercard.com/us/en/business/support/payment-facilitators.html

FAQ

No. An acquirer is a registered card-network member that holds the banking relationship and ultimate risk. A PayFac operates under an acquirer to onboard sub-merchants.