Payment API Integration: What a Payment API Is and How Integration Works

Last updated: July 21st, 2026

Insights

A payment API is the interface your application uses to send and receive payment instructions — authorizing a charge, capturing funds, issuing a refund, checking status — without your code talking to banks or card networks directly. Payment API integration is the work of connecting your system to that interface. This article explains what a payment API is, the pieces of a typical integration, what to look for in the docs, and the common pitfalls — written for the people who actually build the integration.

What is a payment API?

A payment API (application programming interface) is a defined way for your software to ask a payment provider to do something — “authorize this charge”, “capture these funds”, “refund this transaction”, “tell me the status of this order” — and to get a structured response back. You send a request; the provider does the work of reaching the processor, acquirer, or scheme; you get a predictable answer.

The value is abstraction. Without an API, accepting payments would mean integrating directly with banks, card networks, and local schemes, each with its own protocol. A payment API hides that complexity behind a consistent request-and-response contract, so your team writes against one interface instead of many.

This is different from a payment gateway or orchestration layer, though the terms overlap. The API is the interface you call; a gateway is one thing that interface might route to; orchestration is coordinating several providers behind that interface. For the broader picture, see our guide to payment orchestration.

It also helps to separate the kinds of work a payment API does, because “payment API” can mean different surfaces depending on the provider. Most fall into a few categories: accept operations (authorize and capture a customer payment), manage operations (refund, void, partial capture, status lookup on an existing payment), notify operations (webhooks that push events to you), and sometimes payout operations (sending money out, which is a different flow from accepting it). When a provider says “payment API”, it’s worth checking which of these it actually covers — an accept-only API and a full accept-plus-payout API are very different integration scopes.

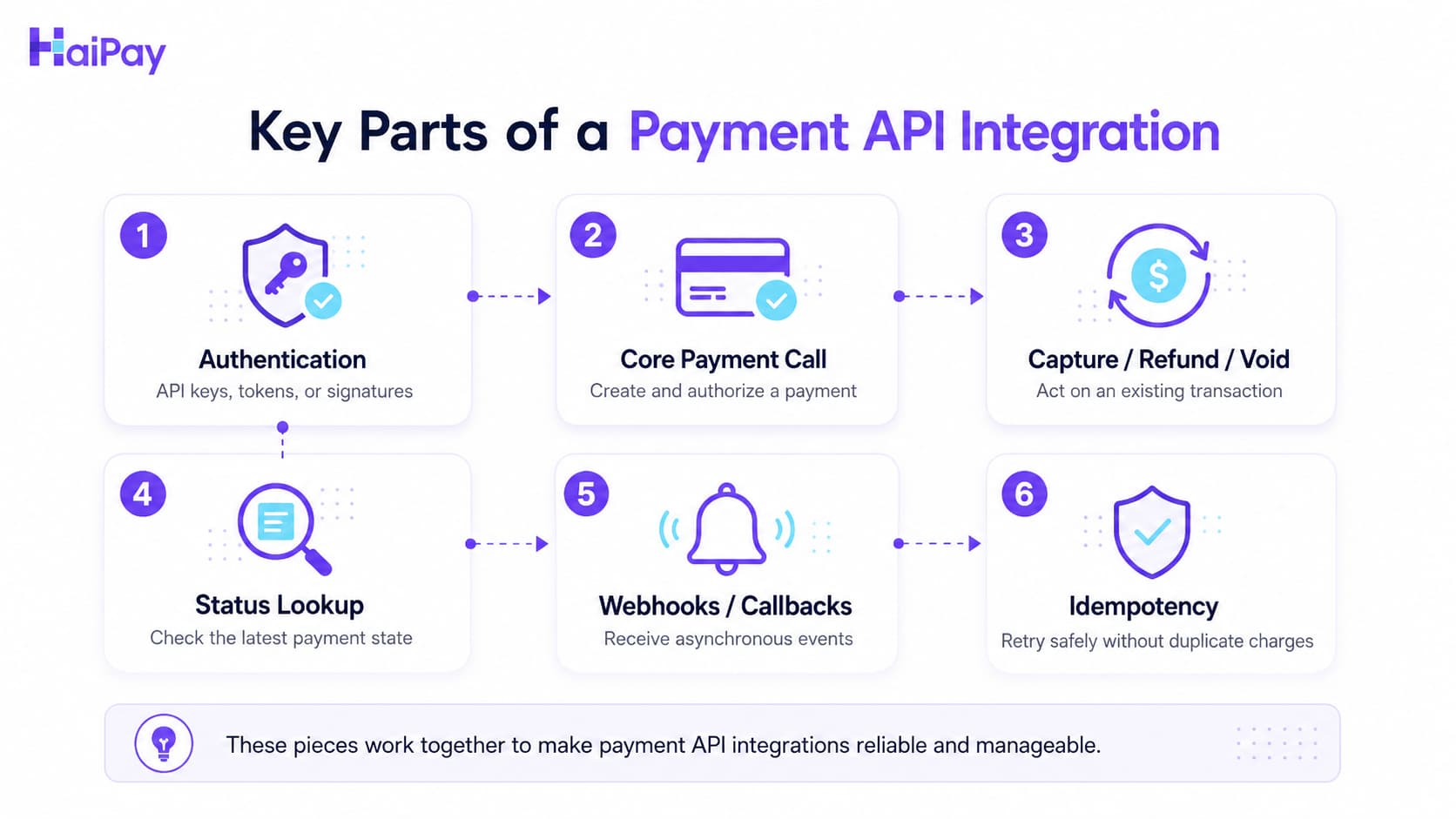

The parts of a typical payment API integration

Most payment API integrations are assembled from a recognizable set of pieces:

- Authentication. An API key, token, or signature that proves your requests are really from you. How keys are issued, rotated, and scoped is the first thing to read in any provider’s docs.

- The core payment call. A request that creates and authorizes a payment, usually returning an identifier you keep for later operations.

- Capture, refund, and void. Follow-up calls that act on an existing payment by its identifier.

- Status and lookup. A way to ask the provider for the current state of a transaction rather than guessing from your own records.

- Webhooks / callbacks. The provider notifying your system of asynchronous events (a payment settled, a dispute opened) so you don’t have to poll constantly.

- Idempotency. A mechanism — often an idempotency key — that lets you safely retry a request without creating a duplicate charge if the network hiccups.

You won’t use every piece on day one, but knowing the full set helps you scope the work honestly instead of discovering capture or webhooks late.

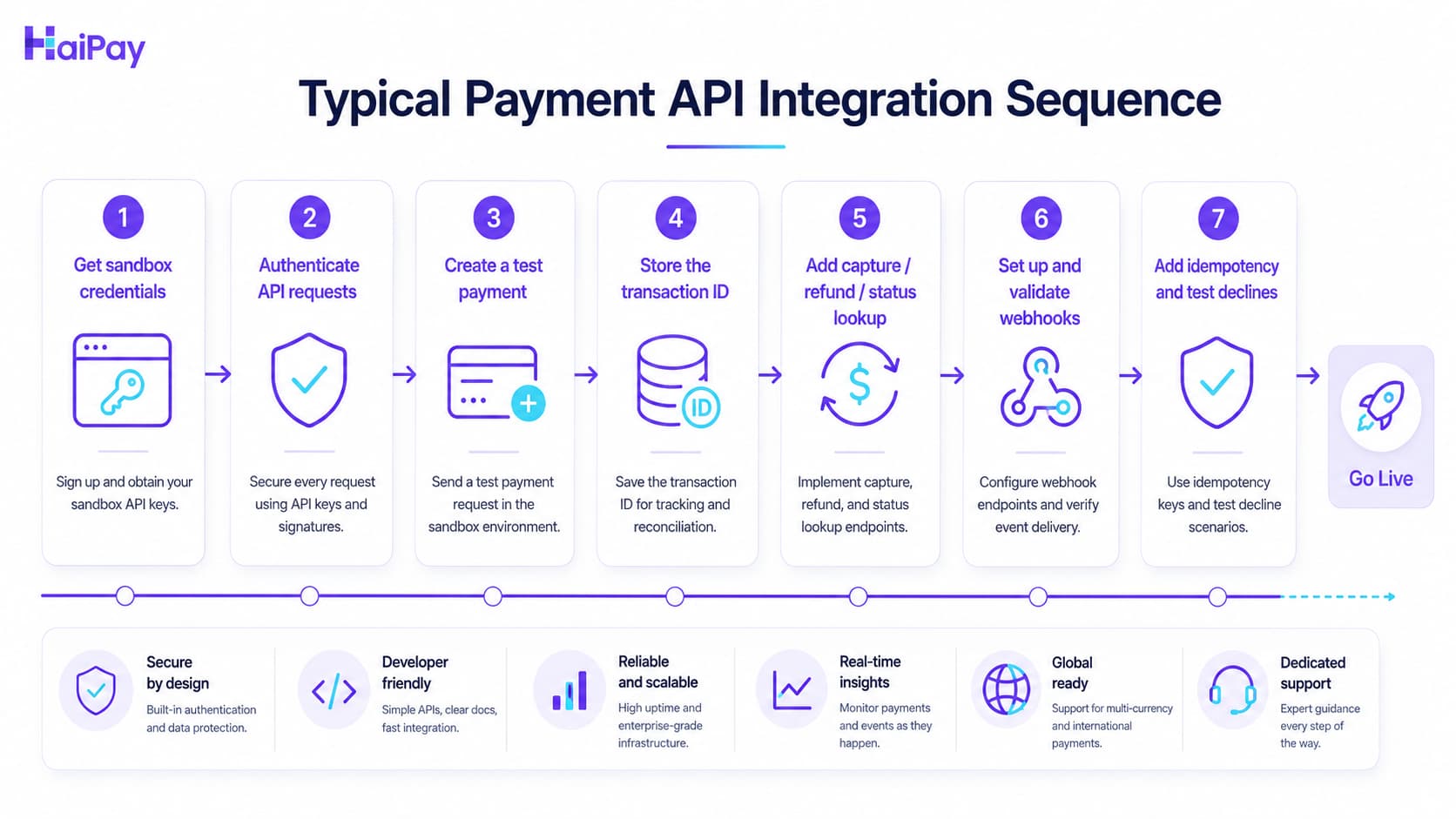

A typical first integration runs in roughly this order. You start in the sandbox: get test credentials and authenticate. You make a single payment call with a test card and confirm you can read the response and store the returned transaction identifier. You then wire up the follow-up calls — capture, refund, status lookup — against that identifier. Next you add a webhook endpoint and verify you actually receive and validate the provider’s event notifications (a step teams routinely defer and regret). You add an idempotency key to the payment call so a network retry can’t double-charge. Only then do you exercise the unhappy paths — declines, refunds, disputes — and confirm your code handles each. Going live is mostly swapping test credentials for production ones once those steps pass, not a separate rebuild.

What to look for in payment API documentation

Before committing to a provider, the docs tell you more than the marketing page does. Read for:

- A sandbox / test environment. Can you make real test calls before going live, with test credentials and test cards? If not, integration becomes guesswork.

- Clear request/response examples. Concrete examples for each call, with the actual fields, beat prose descriptions every time.

- Error and decline handling. How declines and errors are represented, and whether reason codes are documented. This is where integrations quietly break.

- Idempotency and retries. Whether the API supports idempotency keys, and what its guidance is for retrying safely. Note that an API supporting client-side idempotent retries is not the same as the platform automatically retrying or failing over for you — see the boundary note below.

- Versioning. How the provider versions the API and communicates breaking changes, so an upgrade doesn’t surprise you in production.

Common pitfalls in payment API integration

The mistakes that cause real incidents are usually not exotic:

- Skipping idempotency. Under network retries, a non-idempotent payment call can double-charge a customer. This is the single most common avoidable bug.

- Ignoring webhooks. Relying only on the synchronous response misses asynchronous events (late settlement, disputes), so your records drift from the provider’s.

- Treating every decline the same. Some declines are retriable, many are permanent; handling them identically either annoys customers or loses recoverable sales.

- Testing only the happy path. Failed, refunded, and disputed transactions need test coverage too, or they surface for the first time in production.

A note on security and PCI scope

How a payment API handles card data has direct consequences for your compliance burden, so it belongs in the integration decision, not after it. As a general principle, the more raw card data touches your own systems, the broader your PCI DSS scope tends to be — which is why many integrations use provider-hosted fields or tokenization to keep raw card numbers out of your servers. Whether a given approach narrows your scope depends on exactly how the data flows, so confirm it against the provider’s documentation and the PCI Security Standards Council’s guidance rather than assuming. The compliance section of our payment orchestration guide covers the scope question in more depth.

How payment API integration works with HaiPay

HaiPay exposes a standardized payment API: you integrate once against that interface and reach multiple providers and payment methods through it, rather than maintaining a separate integration per provider. Routing across those providers is managed in HaiPay’s operations backend (based on factors such as order type, transaction amount, region, and channel status), so the integration on your side stays focused on the API contract rather than on routing logic.

One honest boundary for engineers planning error handling: HaiPay currently does not provide automatic failover or platform-initiated retries — when a transaction fails, the failed result is returned to you, and your own retry/idempotency logic is what decides what happens next. Design your integration with that in mind.

To go deeper, start with the API integration overview and the API documentation. For how routing and acquiring fit around the API, see local and global acquiring.

Sources

- API integration concepts here (authentication, capture/refund, webhooks, idempotency, versioning) are standard across payment-provider documentation and are stated in general terms, not attributed to one vendor.

- For the broader model, see HaiPay’s guide: What Is Payment Orchestration?

Disclosure: HaiPay is a payment provider; this article is educational. HaiPay (haipay.net) is distinct from similarly named entities such as haipay.io, hipay.com, and haipay.in.

FAQ

It is the interface your application uses to send payment instructions — authorize, capture, refund, check status — and receive structured responses, without your code talking to banks or card networks directly.