Local Payment Acquiring for Ecommerce: A Practical Guide

Last updated: July 21st, 2026

Insights

A practical guide to local payment acquiring for ecommerce — covering checkout integration, local payment methods, authorization, settlement, refunds, and how to evaluate an acquiring provider.

For ecommerce teams, the acquirer layer sits directly beneath checkout and determines which payment methods customers can use, how authorization requests are evaluated, how funds settle, and how disputes are handled. Evaluating acquiring and checkout as a single decision — rather than separately — matters more as you expand across markets.

Acquiring and Checkout Are One Decision

Your checkout can only present payment methods your acquiring infrastructure can process. A locally preferred bank transfer, e-wallet, or domestic card scheme requires connectivity to the local network that handles it. Without that connectivity in a given market, those methods cannot appear at checkout regardless of front-end design.

Baymard checkout research identifies limited payment options as a factor in checkout abandonment, though figures vary by market and merchant type. The Worldpay Global Payments Report shows that payment method preferences differ substantially by country, with local instruments — bank transfers, e-wallets, domestic card schemes — accounting for a significant share of ecommerce payments in many markets.

The full comparison between local and cross-border acquiring models is covered in the local acquiring vs cross-border acquiring guide. The sections below focus on what local acquiring means for ecommerce specifically.

Local Payment Methods in Ecommerce

Local payment methods are instruments tied to domestic networks, banking systems, or regulatory frameworks. Examples include iDEAL in the Netherlands, Pix in Brazil, OVO and DANA in Indonesia, PromptPay in Thailand, BLIK in Poland, Boleto in Brazil, Mada in Saudi Arabia, and KNET in Kuwait. These are illustrative examples — actual availability for any merchant depends on the acquirer's network, licensing, and market agreements.

Whether offering local payment methods affects your conversion meaningfully depends on the market. In markets where a local instrument is how most people pay online, not offering it can limit your addressable customer base. In markets where international cards dominate, the effect is smaller. The Worldpay Global Payments Report provides useful payment preference data by market and channel that is worth reviewing before finalizing your checkout scope.

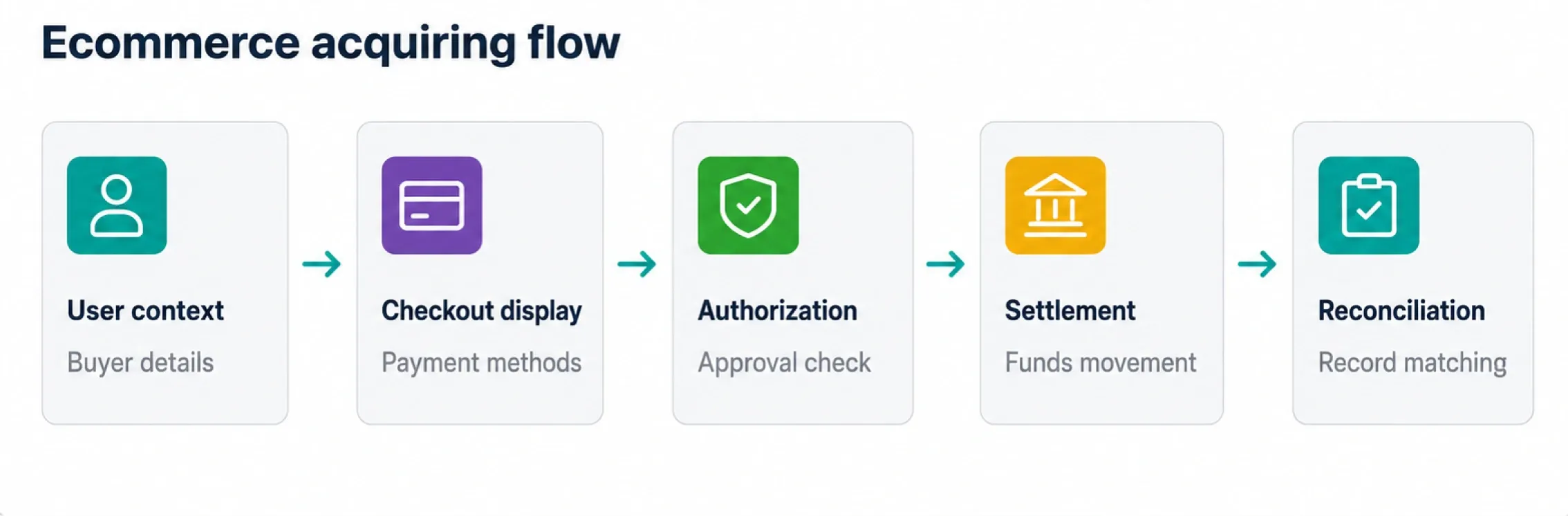

Authorization, FX, and Settlement

When a customer completes a payment, an authorization request flows to the issuing bank. Local acquiring — where the acquirer is licensed in the customer's market — may result in the issuing bank treating the transaction as a domestic payment. This can affect authorization outcomes in some markets and for certain card types. It does not guarantee higher approval rates; results vary by market, issuer, payment method, and transaction context.

FX handling differs between models. Cross-border acquiring typically involves currency conversion at one or more points in the settlement chain, while local acquiring may reduce those steps depending on contract structure. Settlement timelines also vary. Local clearing infrastructure can enable faster settlement in some markets, but timelines should be confirmed at the contract level. For a breakdown of fee structures, cross-border acquiring fees covers the main components.

Refunds, Disputes, and Reconciliation

Refunds typically process through the same rails as the original payment. Disputes under local acquiring are often handled under the rules of the local card scheme, which can simplify documentation and timelines for teams managing high volumes in a specific market — though this depends on the acquirer's capabilities.

Reconciliation is where complexity tends to accumulate most visibly. Merchants processing payments across multiple markets, currencies, and payment methods need tooling that can aggregate transaction data, match settlements, and flag discrepancies automatically. Evaluating reconciliation capabilities should be part of any acquirer assessment, not an afterthought.

When to Stay with Cross-Border Acquiring

Cross-border acquiring through a global acquiring arrangement is often the practical starting point, particularly for merchants testing new markets or operating where card payments dominate. It removes the need for local entities or separate acquirer contracts in each market.

The picture shifts when volume in a specific market grows, when local payment method access becomes important to conversion, or when settlement efficiency becomes a working capital consideration. For context on how these trade-offs play out in growth markets, local acquiring in emerging markets covers the relevant considerations.

Evaluating an Acquiring Provider

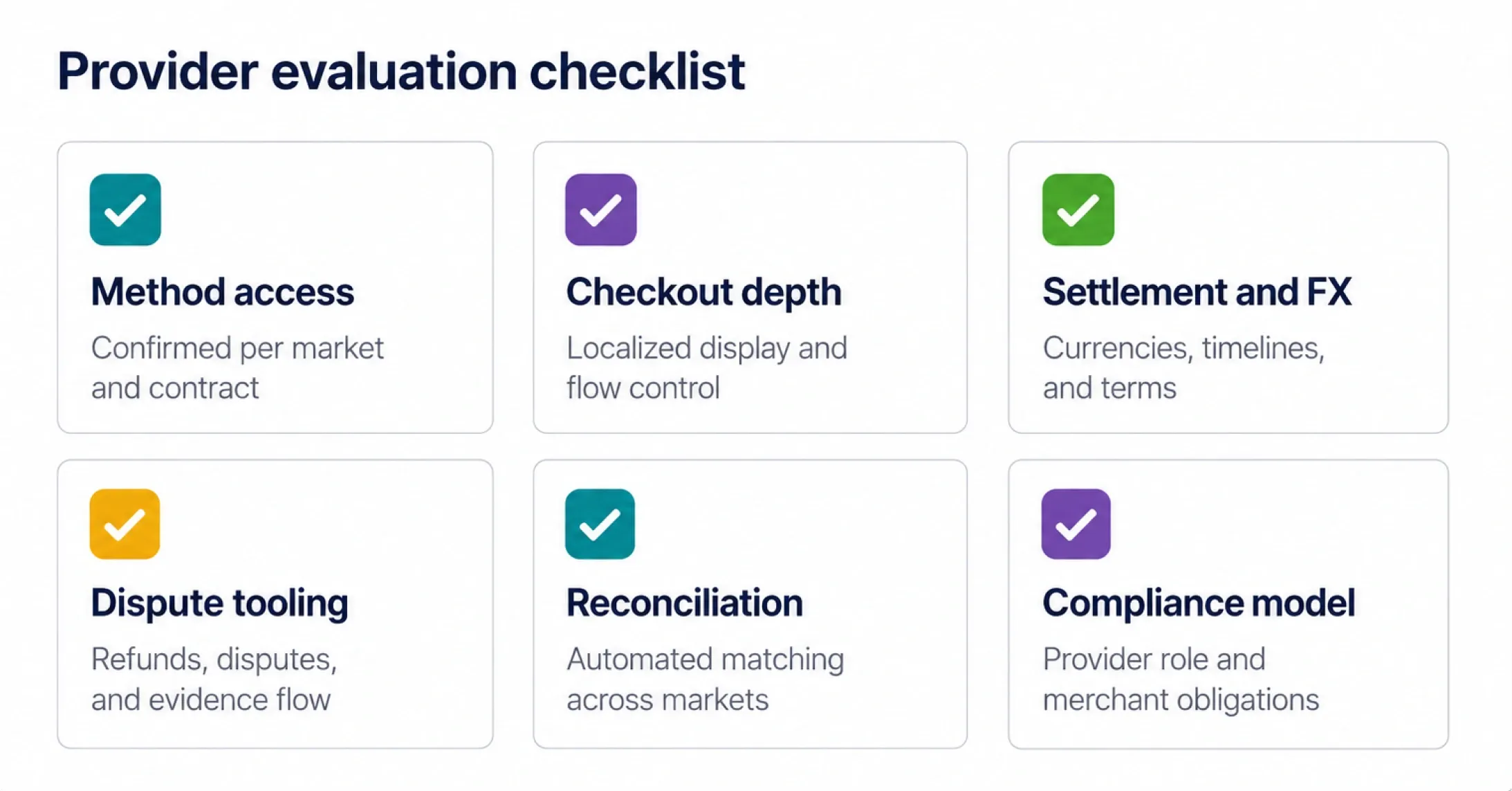

When assessing a payment acquiring solution for ecommerce, the evaluation should cover:

Payment method access. Which local methods does the provider support in your specific markets, confirmed for your merchant category and contract structure?

Checkout integration. How does the Checkout layer connect to acquiring? Integration depth affects payment method display, localization, and flow control.

Settlement and FX. What currencies are available for settlement, on what timelines, and at what FX terms — per market, not just in aggregate?

Dispute and reconciliation tooling. Does the provider offer automated reconciliation and dispute workflows with per-market reporting?

Compliance and licensing. Does the provider hold relevant authorizations in your target markets, or operate through partners? Understand what that means for your regulatory obligations.

How HaiPay Supports Ecommerce Acquiring

HaiPay's E-commerce solution is designed for merchants operating across multiple markets. The underlying payment acquiring solution supports pay-in coverage across multiple supported markets, with local payment method examples that may include OVO, DANA, PromptPay, iDEAL, BLIK, Boleto, Pix, Mada, and KNET depending on market availability.

The Checkout layer supports localized payment method presentation, multi-currency billing, and multilingual UX. Reconciliation is automated. Disputes are handled by localized teams with 24/7 support availability. HaiPay's public materials describe 100+ integrated payment methods and no setup fees; actual payment method availability, onboarding scope, and commercial terms vary by market and merchant profile. For merchants evaluating global acquiring alongside local coverage, both models can be supported within a single provider relationship.

For a broader comparison of local and cross-border acquiring across authorization, settlement, and compliance dimensions, see the local acquiring vs cross-border acquiring guide.

Ready to evaluate local payment acquiring for your ecommerce operation?Explore HaiPay's E-commerce solution or review acquiring options.

FAQ

Local payment acquiring for ecommerce means your transactions are processed by an acquirer licensed and operating in the same country or region as your customer. This enables access to local payment methods, local currency billing, and settlement through domestic clearing networks. Specific availability depends on the acquirer, market, and contract.