Local Acquiring vs Cross-border Acquiring: Key Differences and When to Use Each

Compare local acquiring vs cross-border acquiring: fees, settlement, compliance, and payment flow. A decision guide for global merchants.

Direct Answer

Local acquiring processes payments through an acquirer licensed or connected in the customer’s market, which can improve local payment method access, domestic transaction handling, settlement, and cost efficiency in mature markets. Cross-border acquiring processes payments through an acquirer in another country, making it faster to launch and simpler to manage when testing new markets. Many global merchants start with cross-border acquiring and add local or global acquiring as volume grows.

When you sell to customers in multiple countries, one of the most consequential payment decisions is where and how your transactions are acquired. The choice between local acquiring and cross-border acquiring affects checkout experience, authorization outcomes, settlement timelines, compliance exposure, and how your payment stack scales with your business.

This guide explains both models, compares them across the dimensions that matter most to global merchants, and helps you decide which approach fits your expansion strategy.

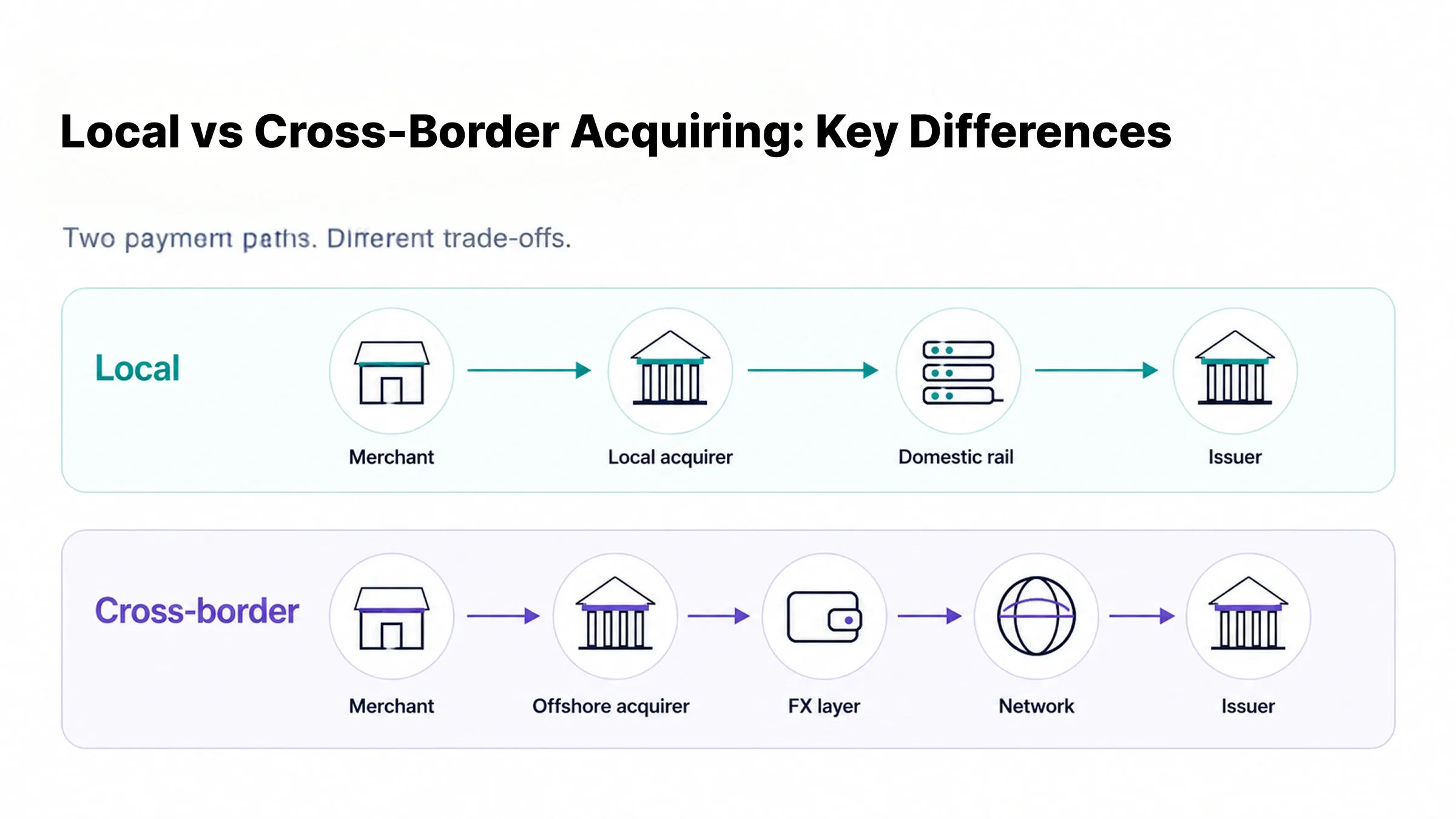

What is local acquiring?

Local acquiring means your payment transactions are processed by an acquirer — a bank or licensed payment institution — that operates in the same country or region as your customer. When a buyer in the Netherlands pays on your checkout, a locally licensed acquirer in that market processes and clears the transaction through local or regional card networks and clearing systems.

Because the acquiring entity operates under the regulatory framework of the customer's market, the transaction is treated as a domestic payment from the issuing bank's perspective. This can affect how the card issuer evaluates the authorization request, which payment methods are available at checkout, how funds settle, and which compliance rules apply.

Local acquiring typically requires working with an acquirer that holds the relevant local licenses or payment institution authorizations in each target market — either through a direct relationship or through a payment provider that offers local acquiring coverage across multiple regions.

What is cross-border acquiring?

Cross-border acquiring occurs when a transaction in one country is processed by an acquirer based in a different country. A merchant incorporated in Singapore can accept payments from customers in Germany through a Singapore- or US-based acquirer without a locally licensed European entity.

Cross-border acquiring is a common starting point for merchants entering new markets because it removes the need to establish local entities or banking relationships upfront. However, card networks often classify cross-border transactions differently than domestic ones, which can influence interchange fees, issuer authorization behavior, and access to locally preferred payment methods in some markets.

Local acquiring vs cross-border acquiring: key differences

Dimension | Local acquiring | Cross-border acquiring | Why it matters |

|---|---|---|---|

Acquirer location | Licensed and operating in the customer's country or region | Based in a different country from the customer | Affects how card issuers classify and route the transaction |

Customer billing experience | May appear as a domestic charge; local currency billing | May appear as a foreign transaction; can trigger issuer friction | Impacts cardholder trust and checkout abandonment |

Payment method coverage | Can support locally preferred methods such as domestic bank transfers, e-wallets, and local card schemes | Access to locally preferred payment methods may be limited depending on the acquirer's network | Determines whether you can serve the full range of customer payment preferences |

Authorization / approval potential | Issuer may treat the transaction more favorably as a domestic payment in certain markets | Cross-border classification may affect how some issuers evaluate authorization | Influences payment success rates; outcomes vary by market, card type, and issuer |

Fees and FX exposure | May reduce cross-border interchange and scheme fees; actual savings depend on contract, market, and volume | Cross-border fees and FX conversion costs may apply | Directly affects processing cost and margin |

Settlement speed | May settle faster through domestic clearing networks depending on the market | Settlement may be extended by cross-border clearing and FX conversion steps | Affects working capital and cash flow |

Compliance and risk handling | Acquirer operates under local regulatory requirements; local KYC, AML, and risk rules apply | Merchant may face additional compliance obligations across jurisdictions | Determines operational burden and regulatory exposure |

Best-fit merchant stage | Merchants with established or growing volume in a specific market | Merchants testing a new market or consolidating global volume under a single relationship | Helps match the acquiring model to business maturity and expansion stage |

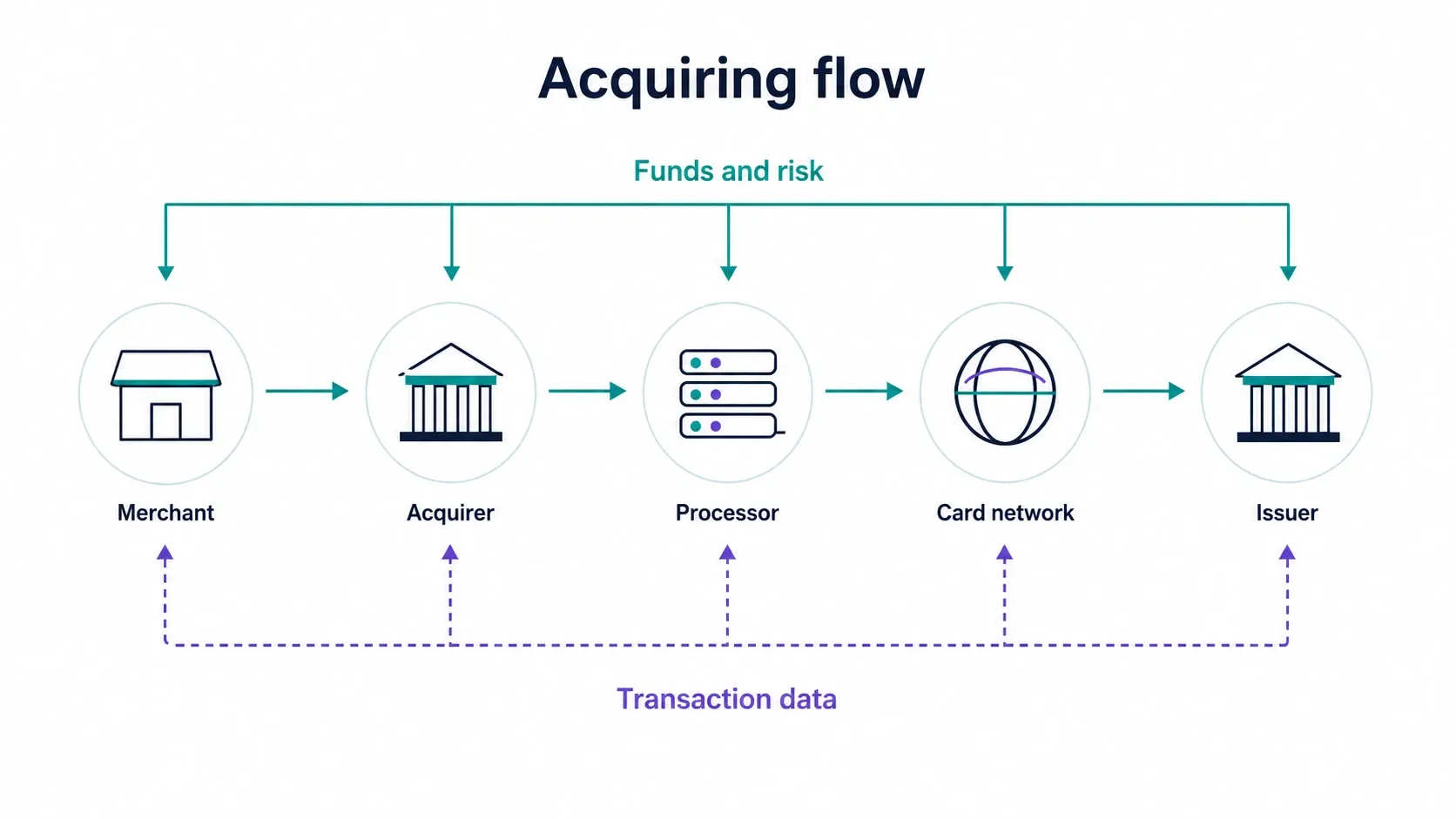

Payment flow

In local acquiring, the transaction travels through a domestic or regional clearing network before reaching the issuer — a shorter, more direct path. In cross-border acquiring, the transaction crosses at least one additional settlement boundary, often with an FX conversion step, which can add processing time and cost depending on the corridor.

Authorization and approval rates

Some issuers in certain markets evaluate domestically acquired transactions differently than cross-border ones. The actual effect on authorization outcomes depends on the market, payment method, card type, and issuer policy. Local acquiring does not guarantee higher approval rates, but it may remove one potential friction point in the authorization chain for certain issuer and market combinations.

Local payment methods and checkout experience

Many markets have strongly preferred local payment instruments — bank transfer schemes, domestic debit networks, and mobile wallet platforms — that may only be accessible through acquirers with local network connections. Examples include PromptPay and GrabPay in Southeast Asia, iDEAL in the Netherlands, Pix in Brazil, and Mada in Saudi Arabia, though availability through any specific acquirer will vary by market and provider.

Fees, FX, and currency conversion

Cross-border acquiring typically involves additional cost layers: cross-border interchange fees set by card schemes, international processing surcharges, and FX conversion margins. Local acquiring can reduce or eliminate some of these costs where domestic interchange rates differ from cross-border rates. Whether local acquiring is cheaper overall depends on the specific market, your acquiring contract, transaction volume, and currency settlement terms.

Settlement and reconciliation

Local acquiring can shorten the settlement chain through domestic clearing systems. Cross-border settlement often involves additional FX conversion and correspondent banking steps that can extend timelines and complicate reconciliation. The degree of difference varies by market, corridor, and provider.

Compliance, licensing, and risk

Acquirers operating locally are subject to the regulatory requirements of the relevant jurisdiction — local KYC, AML, data residency, and consumer protection rules. Merchants expanding into regulated markets in the EU, Southeast Asia, the Middle East, or Latin America should assess both the acquirer's licensing footprint and their own compliance obligations in each country.

When should ecommerce businesses use local acquiring?

Local acquiring tends to make strategic sense when you have established or growing transaction volume in a specific market and want to optimize payment performance and cost. Key scenarios include:

- Market commitment: You have localized your website, pricing, and customer support for a specific country, and the payment experience needs to match that investment.

- Checkout abandonment: Data shows customers abandoning at the payment stage in a specific market where the acquiring model may be a contributing factor.

- Reliance on local payment methods: Your target customers primarily use payment instruments that are only accessible through local network connections.

- Cost optimization: Cross-border processing fees in a market are materially higher than domestic equivalents, and volume justifies the transition.

- Regulatory alignment: Local regulations or issuer requirements favor or effectively require locally licensed acquirers for certain transaction types.

When is cross-border acquiring still a good option?

Cross-border acquiring remains a practical choice in several situations:

- Market exploration: Testing demand in a new country before committing to local entity or banking setup.

- Low or unpredictable volume: Transaction volume does not yet justify the operational overhead of a dedicated local acquiring relationship.

- Card-first markets: International cards are the dominant payment method and local payment method access is less critical.

- Speed to market: Payment acceptance is needed in a new market within days rather than weeks.

- Consolidation preference: Your finance team prefers a single settlement account and unified reporting structure over managing multiple local relationships.

How global acquiring combines local coverage with cross-border flexibility

Global acquiring refers to a model in which a single provider delivers local acquiring access across multiple markets through a unified platform — rather than requiring merchants to manage separate acquirer relationships in each country.

Under a global acquiring arrangement, transactions in supported markets may be routed to a locally connected acquirer, while the merchant maintains one integration, one reconciliation layer, and one commercial relationship with the provider. Coverage, payment method support, settlement terms, and licensing arrangements vary by provider and region. Merchants should evaluate providers on the depth of their local network connections, compliance posture, and settlement capabilities.

How HaiPay supports local and global acquiring

HaiPay's payment acquiring solution is built around local network connectivity across 50+ countries and regions, giving merchants access to 100+ payment methods — including locally preferred options such as OVO and DANA in Indonesia, PromptPay in Thailand, iDEAL in Europe, Pix in Brazil, and Mada in Saudi Arabia — alongside international card schemes, through a single integration.

Key capabilities include:

- Local payment method coverage: Integrated access to locally preferred payment instruments in supported markets.

- Multi-currency settlement: Settlement in multiple currencies with local clearing network connectivity where available in supported markets.

- Smart routing: Intelligent transaction routing designed to optimize authorization paths across available acquirers.

- Localized risk controls: Market-specific risk rules and compliance configurations to support fraud prevention in local contexts.

- Reconciliation tools: Automated reconciliation to reduce manual overhead across multi-market operations.

HaiPay also supports a cross-border payment solution for merchants that need to serve international customers alongside local acquiring coverage. There are no setup fees, onboarding typically moves quickly, and 24/7 live agent support is available.

For specific coverage details, licensing, settlement terms, or payment method availability in your target markets, speak with a HaiPay payments specialist.

FAQ

Local acquiring is a payment processing model in which the acquirer is licensed and operating in the same country or region as the customer. The transaction clears through local or regional networks, which can affect payment method availability, authorization handling, settlement speed, and compliance requirements compared with cross-border acquiring.

Need help mapping your payment stack?

Talk to HaiPay about acquiring, orchestration, local methods, and payout workflows.

Contact us