What Is JCB Payment? A Merchant Guide to Accepting JCB Cards

Last updated: June 28th, 2026

JCB payment means a customer pays with a JCB-branded card or JCB payment technology. For merchants, accepting JCB is not just a logo decision. You need to confirm that your processor, acquirer, checkout setup, authentication flow, reporting, refunds, and dispute handling can support JCB in the markets where your buyers actually use it. JCB describes itself as the only international payment brand based in Japan and reported over 181 million cardmembers and about 72 million merchants as of March 2026; JCB notes that cardmembers include other payment-related products.

This guide treats JCB as one card-based payment method inside a broader alternative payment methods strategy. It is written for cross-border ecommerce, digital goods, SaaS, game, and app merchants deciding whether JCB deserves a place in their checkout mix.

If you are evaluating payment-method coverage for your own checkout, use this article to prepare the right questions, then confirm current availability and implementation requirements with your payment provider or the HaiPay team.

What is JCB payment?

JCB is an international payment brand based in Japan. In merchant checkout planning, a JCB payment is usually a transaction made with a JCB card through an online checkout, point-of-sale terminal, contactless flow, or another supported acceptance route.

For taxonomy, JCB sits closest to a card-based local or regional payment method: it behaves more like a card scheme than a wallet, but its strongest relevance often comes from buyer geography and brand recognition, especially for merchants serving Japan or Asia-connected customers.

That distinction matters. A merchant should not treat JCB like a generic wallet, a bank transfer, or a buy now pay later option. It needs the same operational questions you would ask of a card method:

- Can your processor or acquirer accept JCB for your merchant entity and target countries?

- Does your checkout identify and display the method correctly?

- Which authentication flow applies to ecommerce transactions?

- How are refunds, disputes, settlement, and reporting handled?

- What customer-support message should appear if a JCB payment fails?

The useful definition is practical:

JCB payment is a card-based payment method where customers pay with a JCB card or JCB-supported payment technology, and merchants must verify acceptance, authentication, settlement, refunds, disputes, reporting, and market fit before enabling it in checkout.

How JCB payments work in online checkout

In an online checkout, JCB usually fits into the card-payment path. The exact implementation depends on your payment service provider, acquirer, merchant location, customer location, card issuer, and fraud/authentication setup.

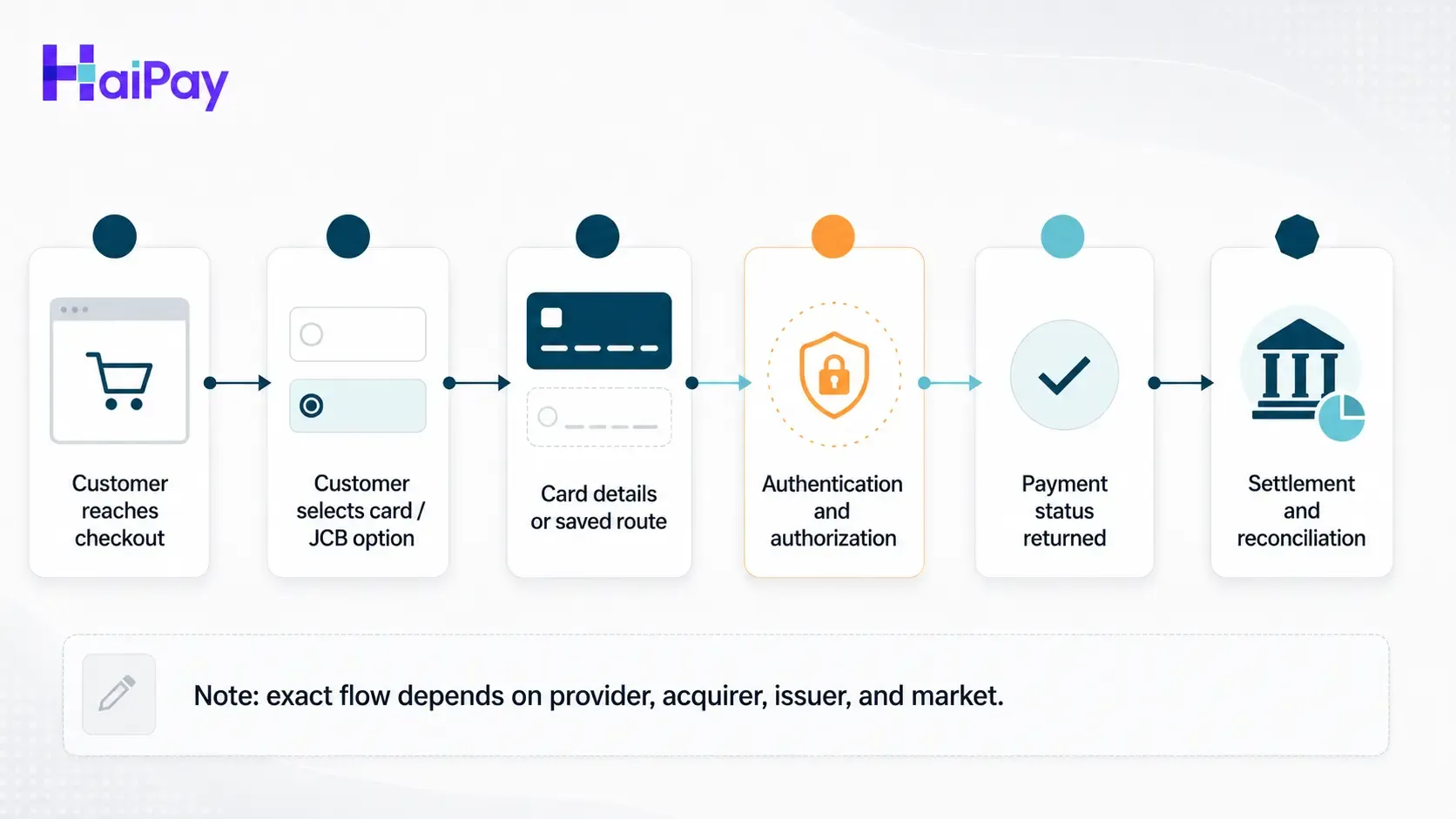

A typical online acceptance flow looks like this:

- The customer reaches checkout and chooses card payment or a visible JCB option, depending on the checkout design.

- The customer enters JCB card details or uses a supported saved card or wallet route if available for that card and device.

- The checkout sends the payment request through the merchant's payment provider and acquiring setup.

- Authentication and authorization are completed according to the provider, acquirer, issuer, and applicable card rules.

- The merchant receives a payment status and decides whether the order can be fulfilled.

- Settlement, reconciliation, refunds, and disputes are handled through the provider/acquirer workflow the merchant has configured.

JCB also has specific payment and security products that may matter during implementation. JCB Contactless is described by JCB as a payment method for secure, simple, fast tap-based payments, and the official contactless page says registered JCB cards can also be used via Apple Pay or Google Pay when the issuing company supports that service. For ecommerce authentication, JCB's J/Secure 2.0 page describes an authentication service that can use supplementary data, such as device information or geographic location, and may require additional credentials like a one-time password.

The merchant takeaway is simple: do not assume the checkout behavior from the JCB logo alone. Ask your provider how card entry, J/Secure or 3DS-style authentication, saved cards, wallet support, refunds, disputes, and reporting work for your exact market and merchant account.

Where JCB is most relevant for merchants

JCB is most relevant when a merchant has a real buyer-fit signal, not just a desire to add more payment logos.

JCB's own What We Do page positions it as the international payment brand from Japan. The same page reports over 181 million cardmembers, with JCB noting that cardmembers include other payment-related products, and about 72 million merchants as of March 2026. It also says JCB cards are accepted in Australia, New Zealand, and Canada through a partnership with American Express, and in the U.S. through Discover Network.

That does not mean every US merchant should prioritize JCB on day one. It means JCB deserves evaluation when your customer mix, product category, or market expansion path suggests demand from JCB cardholders.

Use this mini matrix before adding JCB to your payment roadmap:

Merchant signal | JCB fit | What to verify |

|---|---|---|

You sell to customers in Japan or Japan-connected buyer segments | Stronger fit | Processor/acquirer support, issuer authentication behavior, local currency and reporting needs. |

You sell travel, digital goods, games, apps, subscriptions, or cross-border ecommerce to APAC-heavy audiences | Possible fit | Buyer demand, card mix, authorization performance, refund process, fraud review, customer-support needs. |

Your business is US-only with no Japan/APAC buyer signal | Lower priority | Search/support demand, existing card mix, and whether adding JCB would change checkout completion. |

Your checkout already has too many low-use methods | Add only with evidence | Method ordering, localization, payment-method analytics, and whether JCB should be shown conditionally. |

Your provider cannot confirm JCB acceptance for your entity and market | Not ready | Do not publish JCB availability in checkout until support is confirmed. |

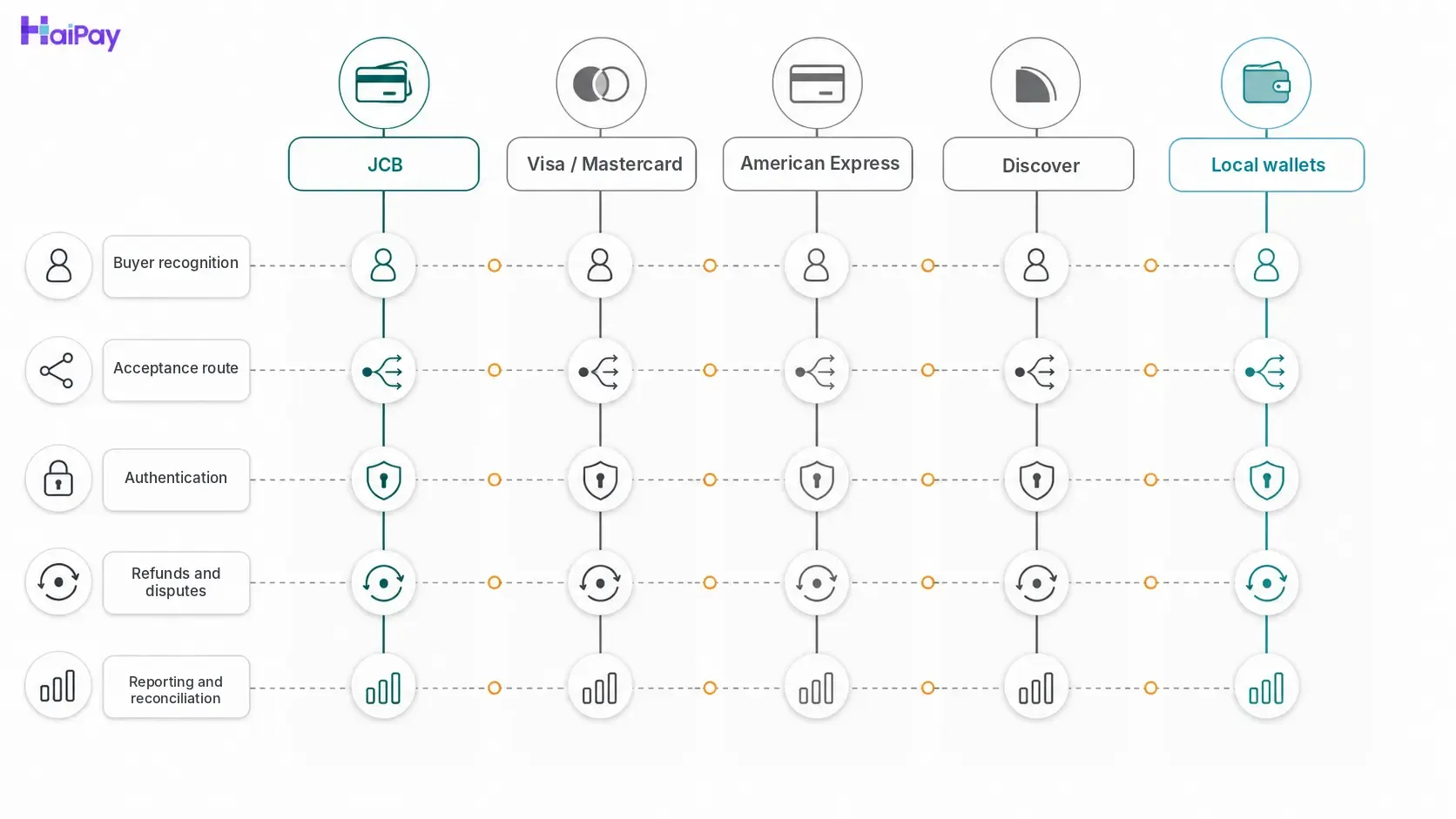

JCB payment vs Visa, Mastercard, Amex, and local wallets

Merchants often ask whether JCB is like Visa, like Amex, or like a wallet. The answer depends on which layer you are comparing.

Method type | What it is | Buyer recognition | Merchant implementation question | When to prioritize |

|---|---|---|---|---|

JCB | International card-based payment brand based in Japan | Strongest where JCB cardholders are meaningful to your audience | Does your processor/acquirer support JCB for your market, currency, authentication, refunds, disputes, and reporting? | When Japan/APAC or JCB-cardholder demand is visible. |

Visa / Mastercard | Global card networks with broad acceptance | Broad global card familiarity | Are card acquiring, authentication, fraud rules, and reporting configured well? | Baseline card acceptance for many online merchants. |

American Express | Card network and issuer/acquirer model with strong brand recognition in some segments | Strong in selected customer and travel/business contexts | Is Amex acceptance enabled, and what are the commercial/operational rules? | When buyer base and provider economics justify it. |

Discover | Card network with US relevance and partnership context for JCB acceptance in the U.S. | More US-focused recognition | How does Discover/JCB routing apply to your provider setup? | When your processor/acquirer confirms the route and buyer demand exists. |

Local wallets | Wallets or super-app payment methods | Often very strong in specific local markets | Does the wallet flow, redirect/app handoff, refund route, and settlement model fit your checkout? | When customers expect that wallet in a target market. |

The practical difference is this: Visa and Mastercard are often part of baseline card acceptance; wallets are customer-account or app-based payment methods; JCB is a card-based brand whose value depends heavily on whether your audience includes JCB cardholders and whether your provider can support the full operating model.

Why merchants consider accepting JCB

Merchants usually consider JCB for one of five reasons.

First, buyer recognition. If a meaningful share of your customers uses or recognizes JCB, showing JCB acceptance can reduce uncertainty at checkout.

Second, market expansion. A merchant expanding into Japan or APAC-connected segments may need to evaluate JCB alongside wallets, bank transfers, and other local payment methods.

Third, card-method completeness. For some cross-border merchants, the payment roadmap is not only cards plus wallets. It can include international card brands, local card schemes, account-to-account payments, and region-specific wallets.

Fourth, checkout trust. A familiar payment mark can help the customer understand that their preferred card may work. This should be measured with payment-method analytics, not assumed.

Fifth, sales and support readiness. If prospects, customers, or partners ask whether JCB is accepted, the business needs a verified answer and a documented route to implementation.

Avoid the weak version of the argument: more methods always increase conversion. More methods can help when they match buyer demand. They can also clutter checkout, create operational work, and introduce support questions if the method is not well understood.

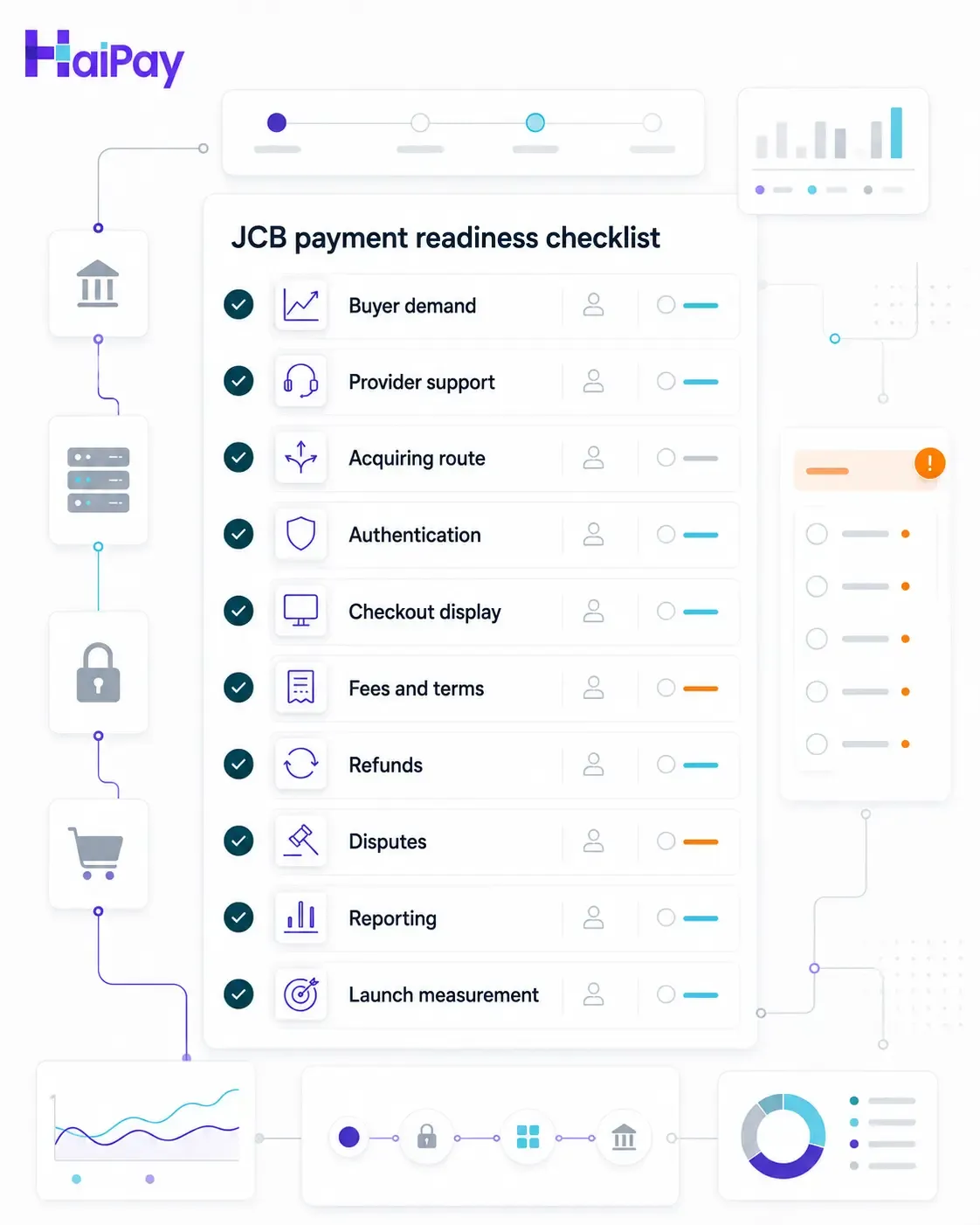

What to verify before adding JCB to checkout

Before enabling JCB, treat the project as a payments readiness review. The right question is not Can we add a JCB logo? It is Can we accept, authenticate, report, refund, and support JCB payments in the markets we serve?

Readiness area | What to verify | Owner |

|---|---|---|

Provider support | Does your payment provider support JCB for your merchant entity, industry, customer countries, and transaction types? | Product / payments |

Acquirer route | Which acquirer or network route processes JCB transactions for your setup? | Payments / provider owner |

Countries and currencies | Where can JCB be accepted, and which presentment/settlement currencies apply? | Payments / finance |

Authentication | Is J/Secure or another 3DS-style authentication flow required or recommended for ecommerce? | Risk / engineering |

Checkout display | Should JCB appear as a separate logo, inside card acceptance marks, or conditionally by country/device? | Product / design |

Fees and commercial terms | What are the processing costs, cross-border costs, FX terms, and any minimums? | Finance |

Refunds | Are full and partial refunds supported, and how long do they take? | Finance / support |

Disputes and chargebacks | Which dispute process applies, and what evidence is required? | Risk / support |

Reporting | Are JCB transactions identifiable in exports, dashboards, payout reports, and reconciliation fields? | Finance / data |

Testing | Are test cards, sandbox flows, webhooks, and decline scenarios available? | Engineering / QA |

If any of these answers is missing, keep JCB in evaluation rather than launch. A payment method should not go live until the customer flow and the back-office flow are both understood.

JCB payment acceptance readiness checklist

Use this checklist as the working version for product, finance, risk, and support.

This checklist is the main content asset for the page. It turns a broad payment-method question into an implementation decision.

When should a merchant add JCB?

Use this decision tree:

Decision question | If yes | If no |

|---|---|---|

Do you have customers in Japan, APAC-heavy segments, travel/cross-border contexts, or JCB-cardholder audiences? | Continue to provider validation. | Keep JCB as a monitored roadmap item rather than a launch priority. |

Can your provider/acquirer confirm JCB support for your merchant account and target market? | Continue to operational readiness. | Do not show JCB as accepted; ask the provider for availability and restrictions. |

Can finance and support handle refunds, disputes, reporting, and customer questions? | Continue to checkout testing. | Resolve back-office ownership before launch. |

Can checkout display JCB clearly without crowding the payment step? | Run QA and limited rollout if available. | Consider conditional display by country, device, or buyer segment. |

Can you measure method share and checkout impact? | Launch with monitoring. | Add tracking before enabling the method broadly. |

The best time to add JCB is when all three are true: your buyers have a reason to use it, your provider can support it, and your internal teams can operate it after the first transaction succeeds.

JCB payment implementation checklist

Before launch:

- Confirm JCB availability with your payment provider or acquirer.

- Confirm supported merchant countries, customer countries, currencies, and business categories.

- Confirm whether J/Secure or another authentication flow applies.

- Test successful authorization, failed authorization, authentication challenge, timeout, refund, and reporting scenarios.

- Decide whether JCB appears for all customers or only selected countries, devices, or buyer segments.

- Confirm how JCB appears in payment-method analytics and reconciliation exports.

- Prepare support scripts for failed payments, unsupported cards, pending orders, refunds, and disputes.

- Review logo usage and payment-method display rules.

- Confirm the launch metric owner for authorization rate, method share, checkout completion, refund rate, dispute rate, and support contacts.

After launch:

- Compare JCB method share against buyer geography.

- Watch failed-payment reasons and authentication drop-off.

- Review refund and dispute handling with support.

- Check reconciliation accuracy with finance.

- Decide whether to expand, conditionally display, or reduce visibility based on measured use.

How JCB fits into an alternative payment methods strategy

JCB should not replace your broader payment-method strategy. It should sit inside it.

A practical checkout mix may include:

- Cards for broad baseline acceptance.

- JCB when JCB cardholder demand and provider support justify it.

- Local wallets where customers expect app-based payment.

- Bank transfers or Pay by Bank where bank-account payment is familiar and operationally viable.

- QR or offline methods where local payment behavior requires them.

The parent Alternative Payment Methods guide explains how to evaluate payment methods by market, customer fit, operations, risk, settlement, refunds, and implementation effort. This JCB guide is the narrower child page: it helps you decide whether JCB belongs in that mix and what to verify before launch.

If you are evaluating checkout coverage, explore HaiPay Checkout and contact HaiPay to confirm current payment-method availability for your target markets. Do not treat this article as confirmation that JCB is currently supported by HaiPay.

FAQ

A JCB payment method is a card-based payment option that lets customers pay with a JCB-branded card or JCB-supported payment technology. For merchants, accepting JCB requires provider/acquirer support, checkout configuration, authentication, reporting, refunds, and dispute handling.

Blog article footer

Subscribe to the HaiPay Blog

Stay connected with HaiPay and receive new blog posts in your inbox.

Like this post? Join our team.

HaiPay builds financial tools and economic infrastructure for the internet.