Embedded Payments Explained: A Guide for Cross-Border Platforms

Last updated: July 9th, 2026

Insights

Embedded payments help platforms keep checkout, settlement and payouts inside their own branded product instead of sending users to an external processor. This guide explains how embedded payments differ from integrated payments, embedded finance and Banking-as-a-Service; how API, Hosted Checkout and Components-based payment flows work; and why cross-border platforms need local payment methods in each market, not just card acceptance. It also outlines how to compare provider models such as PayFac, PayFac-as-a-Service, gateway processing and Merchant of Record, with a focus on integration fit, local coverage, compliance responsibilities and payout needs.

Disclosure: This guide is published by HaiPay, a payments infrastructure provider. It references HaiPay's own products alongside other providers; it is educational and not financial or compliance advice. Market figures are dated and sourced; product coverage varies by market — confirm specifics for your use case.

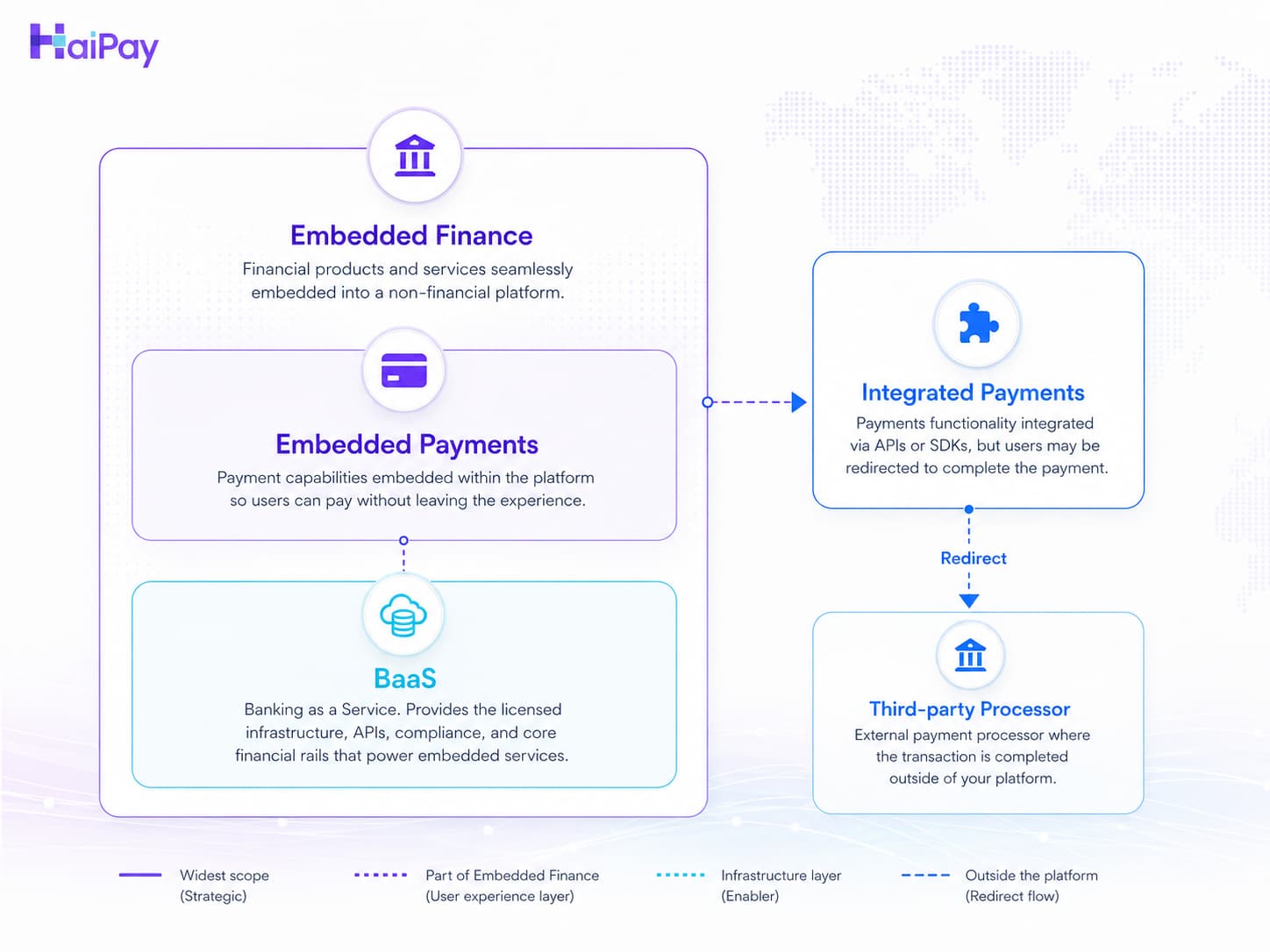

Embedded payments are payment capabilities built directly into a non-financial software platform, letting users pay without leaving the app. Unlike integrated payments — which redirect the user to a third-party processor — embedded payments keep checkout, and often settlement and payouts, inside the platform's own branded experience. For cross-border platforms, embedded payments can also incorporate local payment methods in each market through an API, not just cards.

That single shift — from sending users to a payment provider to building payments into the product — is why software platforms, marketplaces, and SaaS companies are rethinking how money moves through their apps. This guide explains what embedded payments are, how they differ from the terms they're constantly confused with, how they work, and what cross-border platforms should look for when choosing a provider.

Embedded payments vs. integrated payments vs. embedded finance vs. BaaS

These four terms are used interchangeably across the web, and that confusion is the single biggest source of misunderstanding for platforms evaluating their options. They are not the same thing. Here is how they relate:

Term | What it is | Who owns the experience | Example |

|---|---|---|---|

Integrated payments | Payment processing connected to software, but the user is redirected to a third-party processor's page or terminal to pay | The processor | Software that links out to a hosted PayPal or gateway page |

Embedded payments | Payment functionality built into the platform so users pay without leaving it | The platform | A booking app where you pay in-app; a marketplace checkout |

Embedded finance | The broader category: any financial service (payments, lending, insurance, accounts) embedded into a non-financial product | The platform | A retail app offering "buy now, pay later" or insurance at checkout |

Banking-as-a-Service (BaaS) | A licensed bank exposing banking capabilities (accounts, cards, compliance) to non-banks via API, often the layer underneath embedded finance | The bank (licensed), consumed by the platform | A platform issuing branded debit cards through a partner bank |

The simplest way to hold it in your head: embedded payments are a subset of embedded finance, and BaaS is often the infrastructure layer that makes the broader financial services possible. Integrated payments are the older, looser model embedded payments improved on.

This guide focuses on embedded payments. If you want to go deeper on the wider category, see our companion guides on embedded finance and Banking-as-a-Service. (Internal links to be activated when those pages are live.)

A common edge case: Is Klarna embedded finance? Klarna's "buy now, pay later" option offered inside a merchant's checkout is a form of embedded finance (embedded lending, specifically) — which shows how payments, lending, and the broader category overlap in practice.

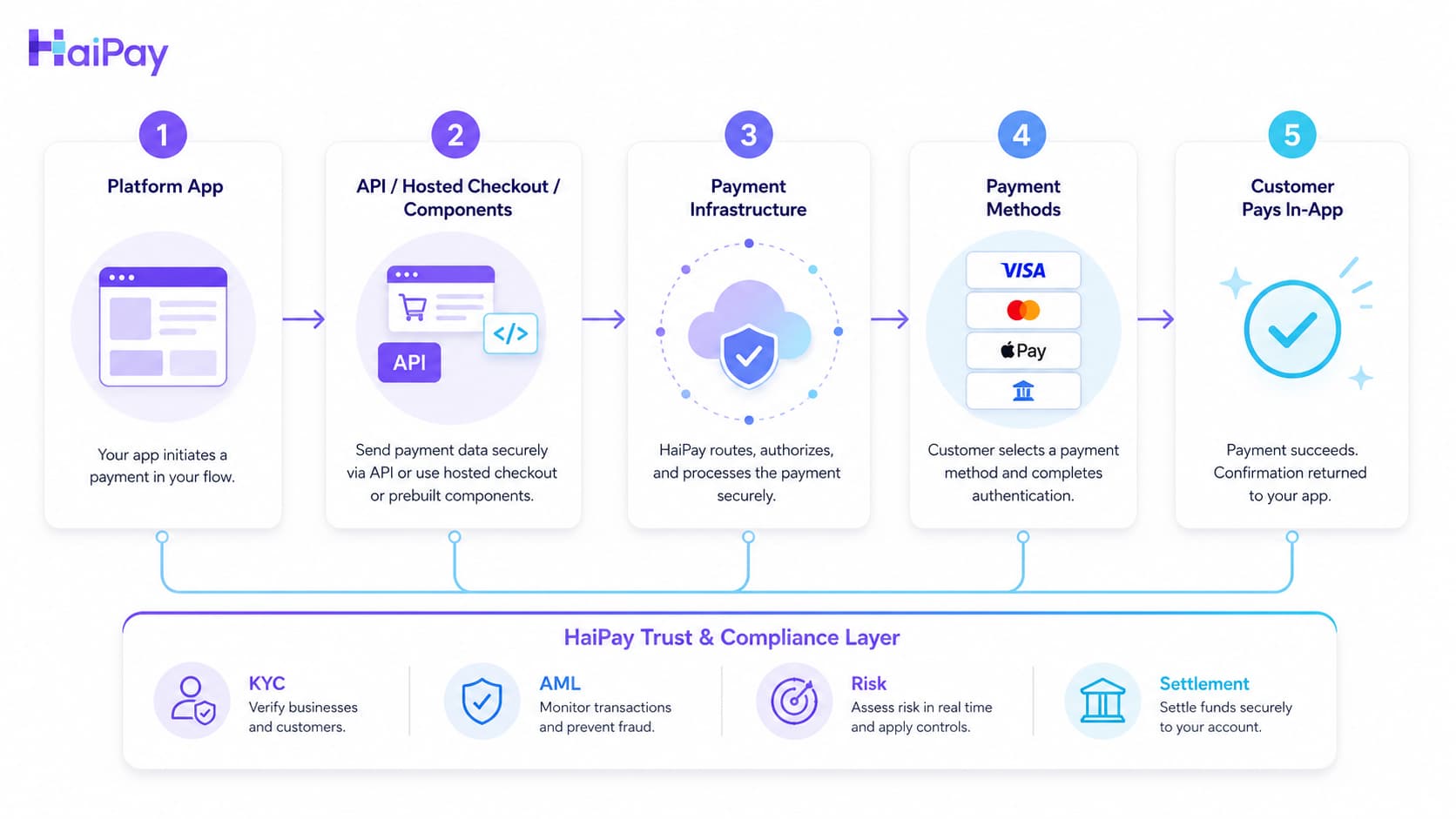

How embedded payments work

Embedded payments sit on a stack of components that most platforms consume rather than build from scratch:

- APIs and SDKs — the platform calls a provider's API, or drops in pre-built UI components, to accept and manage payments inside its own product.

- Payment rails and methods — card networks, bank transfers, real-time payment schemes, digital wallets, and local payment methods that vary by market.

- A payments provider or facilitator — the infrastructure partner that connects the platform to those rails and handles the heavy lifting of processing.

- Onboarding, KYC and AML — identity verification and anti-money-laundering checks for the platform's own users, such as merchants, sellers, or sub-accounts.

In practice, a platform integrates once and can then offer payments to its users as if it were a native feature. With HaiPay, for example, platforms can integrate payment acceptance and local payment methods through an API, Hosted Checkout, or drop-in Components — choosing the level of control and build effort that fits their product.

The benefits of embedded payments

Platforms move to embedded payments for four reasons that compound:

- Payments become a revenue stream, not just a cost. Instead of pointing users to an external processor, the platform participates in the payment flow it already generates. The scale of that opportunity is why infrastructure revenue in this space is growing — in the US, embedded finance platform and infrastructure revenue is forecast to more than double from $21 billion in 2021 to $51 billion in 2026 (Bain & Company). (This figure is for the broader embedded finance market, of which payments is the largest component.)

- A smoother customer experience. Users complete payment without being bounced to an unfamiliar page, which reduces drop-off and keeps the platform's brand front and center.

- Faster integration and less maintenance. Consuming a provider's API or components is far lighter than building and certifying a payment stack in-house — an effort that can otherwise take many months.

- Room to scale. As the platform grows into new segments or markets, the same integration can extend to new payment methods and geographies rather than requiring a new project each time.

To put the trajectory in context: embedded finance is forecast to reach roughly 10% of all US financial transactions by 2026, with total transaction value surpassing $7 trillion (Bain & Company). Payments are the entry point into that shift for most platforms.

Embedded payments examples and companies

Embedded payments are already everywhere, even when they're invisible:

- Ride-hailing and delivery apps — you pay inside the app the moment the ride or order ends; there's no separate checkout step.

- Marketplaces — buyers pay and sellers get paid out without either party leaving the platform.

- Vertical SaaS — a scheduling tool for clinics, salons, or contractors that lets its business customers take payment inside the same software they use to run operations.

- Creator and gig platforms — payouts to creators, drivers, or freelancers handled natively.

The provider landscape spans large processors and platforms, such as Stripe, Adyen, and others, specialist facilitators, and infrastructure providers focused on specific strengths such as cross-border reach. Which one fits depends less on brand and more on the criteria below — especially if your users span multiple countries.

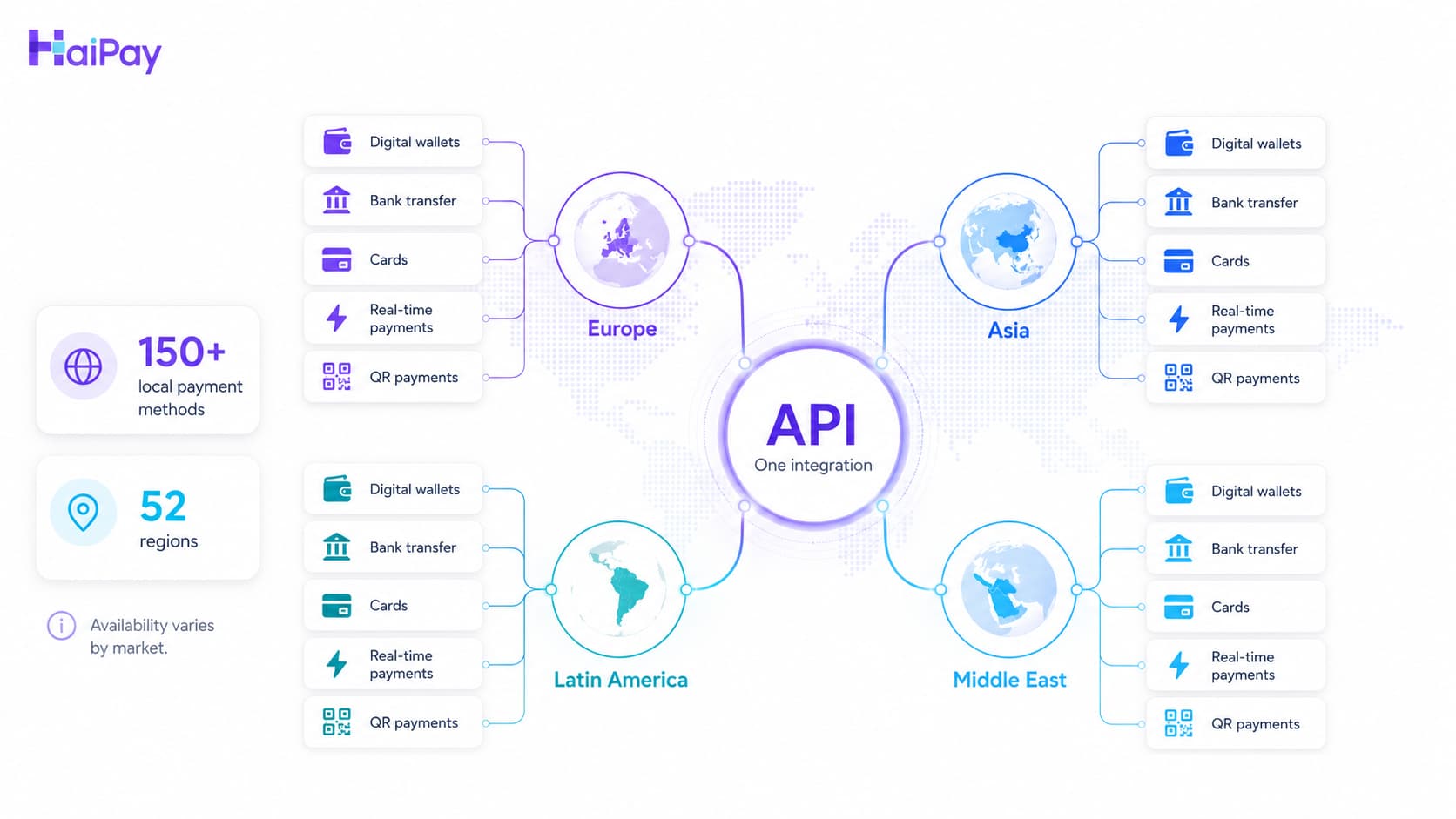

Embedded payments for cross-border platforms

This is where many platforms hit a wall that domestic-only guides never mention: paying with a card works fine in one market and fails in the next. Shoppers in different regions expect different payment methods — bank transfers, local wallets, real-time payment schemes — and a checkout that only offers cards can quietly lose a large share of would-be buyers in those markets.

For a cross-border platform, the value of embedded payments is not just "pay in-app" — it's "pay in-app, the way each local customer expects." That means the underlying provider has to bring local payment methods to the integration, not leave the platform to source each one country by country.

This is the layer HaiPay focuses on. HaiPay's payment network spans 150+ local payment methods across 52 regions, which platforms can integrate through an API, Hosted Checkout, or Components — accessing local coverage through a single integration rather than rebuilding for each new market. The exact methods available and each market's requirements vary, so the practical value is the ability to reach local methods through one integration, not an assumption that every market behaves identically.

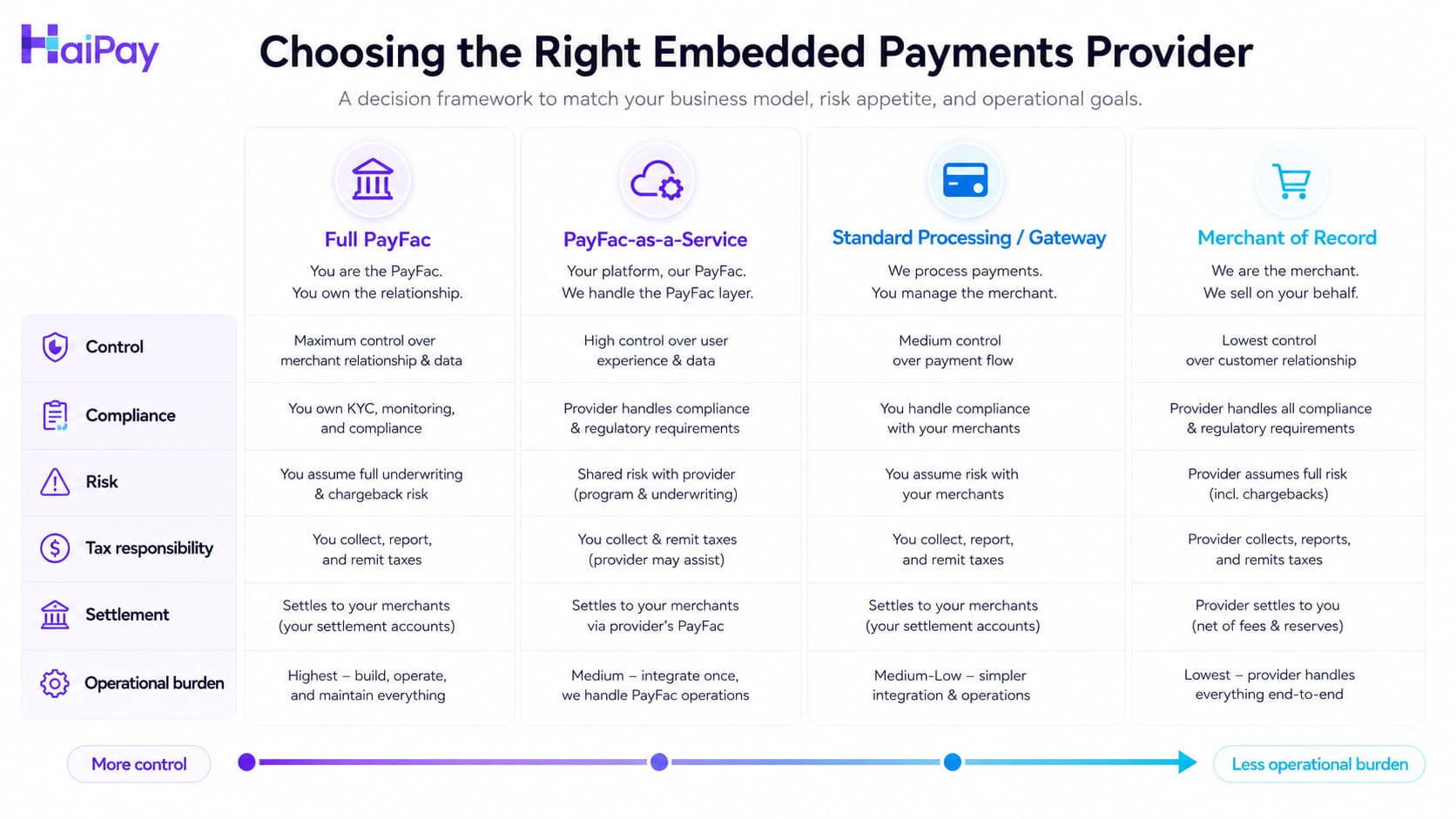

How to choose an embedded payments provider

Once you've decided to embed payments, the real question is how much of the payment operation you want to own versus outsource. The main models trade control against complexity:

Model | What you take on | Best when |

Become a full payment facilitator (PayFac) | You underwrite and onboard your users, and carry liability for fraud, chargebacks, KYC/AML, and PCI compliance | You have scale, capital, and a dedicated payments/compliance team, and want maximum control and margin |

PayFac-as-a-Service | A provider handles the heavy compliance and infrastructure; you get monetization and a degree of control without registering as a facilitator | You want payment revenue and control without building underwriting and compliance in-house |

Standard processing / gateway | The provider owns most of the flow; you integrate acceptance | You want the fastest path and don't need to monetize the payment layer |

Merchant of Record (MoR) | A third party becomes the seller of record and takes on tax, compliance, and fraud liability | Global tax and compliance burden is your main concern |

Beyond the model, weigh these criteria — the ones that most often get overlooked until they become a problem:

- Local payment method coverage in the specific markets your users are in, not just the number of methods overall.

- Onboarding control — can you shape the experience for your users, or is it a black box bolted onto your product?

- Integration options — API, hosted checkout, and pre-built components give you room to trade build effort against control.

- Clarity on compliance and liability — who is responsible for what, and does the provider's answer match your team's capacity?

- Payouts and settlement — if you run a marketplace or pay out creators or sellers, confirm the provider supports that flow.

There is no single "best" provider — there's the one whose model and coverage fit your product and your markets.

Bring embedded payments to your platform

If you're building payments into a cross-border product, the deciding factor is usually local coverage and integration fit. Book a demo or talk to a payment specialist to see how your platform can integrate acceptance, local payment methods, and payouts through HaiPay's API, Checkout or Components, local payment methods, and mass payouts.

Wesley Wang is part of the team at HaiPay, a payments infrastructure provider helping platforms accept and move money across borders.

FAQ

Paying for a ride inside a ride-hailing app the moment your trip ends is an embedded payment — the transaction happens inside the app, with no redirect to a separate payment page.

Blog article footer

Subscribe to the HaiPay Blog

Stay connected with HaiPay and receive new blog posts in your inbox.

Like this post? Join our team.

HaiPay builds financial tools and economic infrastructure for the internet.