Merchant Acquirer vs Payment Processor

Reviewed by Yuanqiang Wu

Last updated: June 5th, 2026

Insights

A merchant acquirer owns the merchant account, settlement relationship, and risk. A payment processor supports the transaction-processing layer. This article explains how the roles differ, why one provider can do both, and when the distinction matters.

A merchant acquirer and a payment processor do two different jobs, even when they are bundled inside the same provider. A merchant acquirer (also called an acquiring bank) is the merchant-side financial role: it holds your merchant account, settles card funds, and carries the risk if transactions go wrong. A payment processor is generally described as the operational and technical role that helps move payment information through the transaction flow so a payment can be authorized, cleared, and settled. The two terms get mixed together because one provider can play both roles.

For the full picture of merchant acquiring, including acquiring banks, payment facilitators, merchant accounts, and gateways, see our merchant acquiring guide. This article zooms in on one comparison: acquirer vs processor.

Merchant acquirer vs payment processor: the short answer

Merchant acquirer (acquiring bank) | Payment processor | |

|---|---|---|

Core role | Holds the merchant account, settles funds, carries the risk | Helps route and manage payment transaction processing |

Holds your funds? | Yes | Generally no; it supports transaction processing rather than owning the merchant account |

Card-network relationship | Direct, as a member of or sponsored into the networks; exact model varies | Usually through the acquirer or acquiring bank |

Bears chargeback / default risk? | Yes | Generally no |

Plain-language label | The "financial / settlement" side | The "technical / processing" side |

The "financial side vs technical side" split is a common way the industry frames the two roles; it is a useful mental model, not a strict legal definition.

What a merchant acquirer does

A merchant acquirer is a bank or financial institution that lets a business accept card payments. Its defining jobs are financial:

- It holds your merchant account — the account where card funds land before they are paid out to your business bank account.

- It settles your funds — it deposits the money, minus fees, into your account after a transaction clears.

- It carries the risk — if you issue refunds or chargebacks you cannot cover, or go out of business, the acquirer is exposed. That is why an acquirer vets, or underwrites, the businesses it onboards.

- It works with the card networks — it connects your transactions into Visa, Mastercard, and other networks. Acquirers are generally members of, or sponsored into, those networks; the exact membership model varies by provider and region.

The short version: without an acquirer or acquiring relationship, you generally do not have the merchant account and settlement role needed to receive card funds.

What a payment processor does

A payment processor is generally described as the technology and operations layer that helps a card transaction move through the payment system. In a typical card flow, the processor helps transmit payment information, communicate with the relevant parties, obtain authorization, and support clearing and settlement steps.

That does not make the processor the same as the acquirer. The processor supports the movement of payment data and transaction messages; the acquirer owns the merchant account relationship, settlement exposure, and chargeback/default risk. This is also why merchant processing is separate from card issuing: the processing/acquiring side of a payment is not the same as the customer's-bank side.

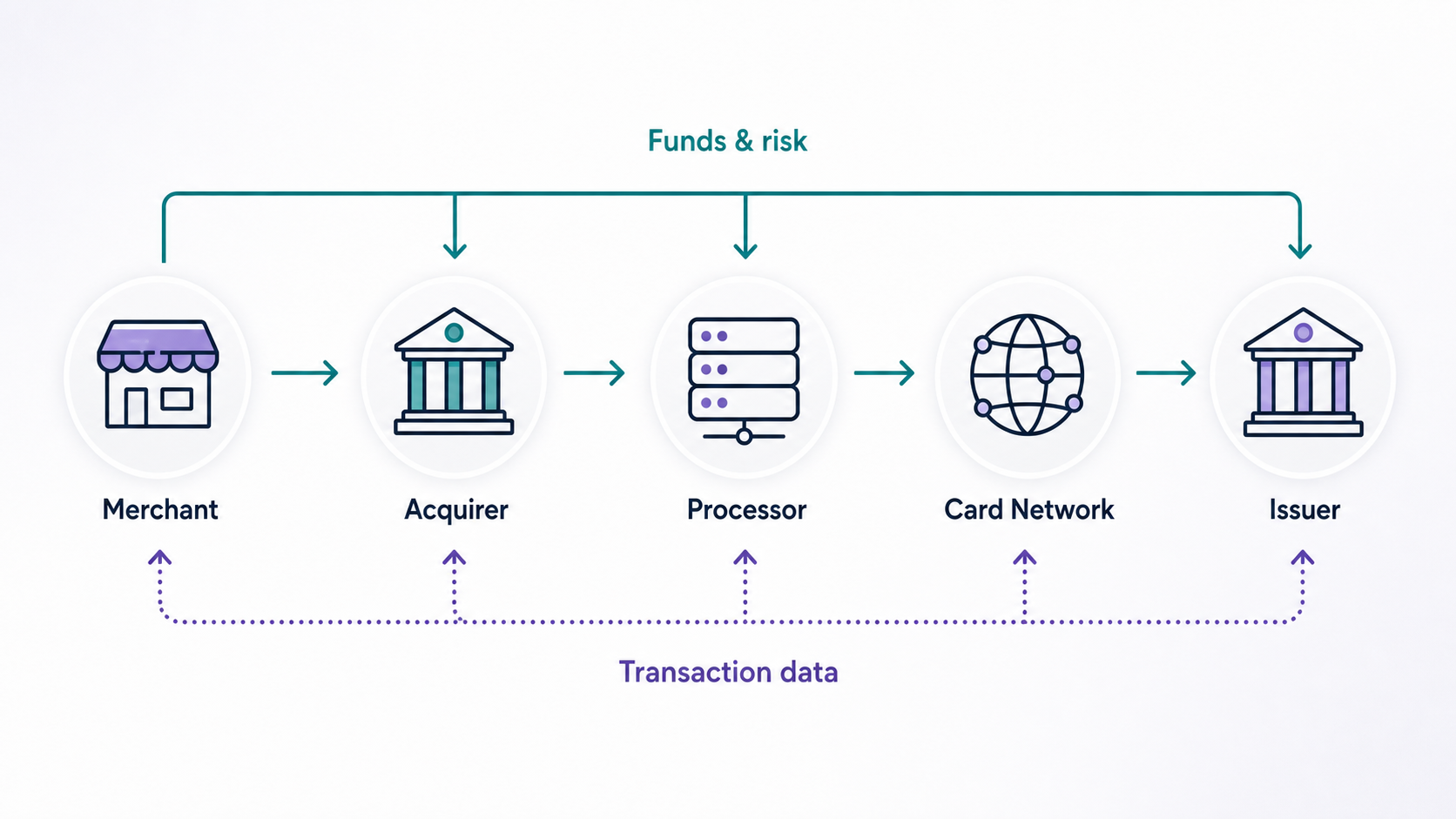

How an acquirer and a processor work together

In a single card payment, the two roles sit next to each other. The flow is usually described in three stages:

- Authorization — the customer pays; the processor helps route the request through the payment chain so the issuer can approve or decline it.

- Clearing — the approved transaction details are exchanged and reconciled so the parties agree on what is owed.

- Settlement — funds move through the card-payment system, and the acquirer deposits the merchant's net funds into the merchant account.

The processor is most visible in the transaction-message flow. The acquirer owns the merchant account and the risk-bearing settlement relationship. Both roles are needed for a card payment to complete, but a merchant may encounter them as one bundled service.

Why one company is often both

Here is the part that causes most of the confusion: many full-stack payment providers can combine acquiring and processing functions. One provider may hold the merchant account relationship and also operate the processing technology, so a business signs up once and never sees the roles separately.

When a single provider bundles both functions, people naturally use "acquirer" and "processor" to mean the same thing in everyday conversation. The underlying jobs are still different: acquiring is the financial and risk-bearing role; processing is the transaction-processing role.

This is also why questions like "Is my provider an acquirer or a processor?" often do not have a one-word answer. For many large providers, the honest answer can be both, or one role plus partners behind the scenes.

Is your provider an acquirer or a processor? (how to tell)

You do not need the provider's internal licensing details to work out which role it is playing for you. Ask two questions:

- Does it hold your merchant account and settle your funds to your business account? If yes, it is acting as your acquirer, or it has an acquirer behind it.

- Does it route your transactions and return approvals or declines? If yes, it is doing the processing function.

If the same provider does both, it is a full-stack acquirer-processor setup, which is common. If you cannot tell from the marketing, ask: "Do you hold my merchant account and settle my funds, or do you route transactions to an acquiring partner?" The answer tells you which role they own and whether there is a separate acquirer in the chain.

Does the difference matter for your business?

Often, it does not. If you use one full-stack provider that handles everything and your volumes are straightforward, you can treat "acquirer" and "processor" as one operational box and move on.

It starts to matter when:

- You sell across borders. Where and how your transactions are acquired can affect approval rates and cost, though the size of any effect depends on your markets, card mix, and setup. The acquirer relationship is the lever here, not just the processing technology.

- You want to switch or add a processor without changing who holds your account. That is only possible if you know which provider owns which role.

- You run a multi-acquirer setup to route transactions to different acquirers by market. That strategy only makes sense once you separate the acquiring role from the processing layer.

For the broader context, including acquiring banks vs issuing banks, payment facilitators, merchant accounts, and gateways, the merchant acquiring guide covers the whole picture. This page deliberately stays on one comparison.

Where HaiPay fits

HaiPay provides acquiring and cross-border payment services for businesses that sell into multiple markets. If you are weighing up acquirer vs processor because you are expanding internationally, the acquiring side of your setup is the part worth understanding clearly.

To see whether it fits your markets, explore HaiPay acquiring, or talk to our team.

FAQ

What is the difference between a merchant acquirer and a payment processor?

The acquirer holds your merchant account, settles your funds, and carries settlement/chargeback risk. The processor supports the transaction-processing function so payment information can move through the payment chain. One provider can do both, but the roles are distinct.

Can one company be both a merchant acquirer and a payment processor?

Yes. A full-stack provider can combine acquiring and processing functions, which is why the two terms are often used interchangeably.

How do I tell whether my provider is an acquirer or a processor?

Ask whether it holds your merchant account and settles your funds, or whether it routes transactions to an acquiring partner. If it does both, it is acting as a full-stack acquirer-processor setup.

Do I need both an acquirer and a payment processor?

Functionally, every card payment needs both roles. In practice, you may get both from one provider, so you do not necessarily contract them separately.

Is a merchant acquirer the same as an acquiring bank?

Effectively yes. "Acquiring bank" emphasizes that the acquirer is, or works as, a bank or regulated financial institution that holds your merchant account. The merchant acquiring guide explains the term in more depth.

Sources

- Wikipedia — Acquiring bank: defines the acquirer, states that it offers a merchant account, and describes the acquirer's solvency/chargeback risk.

- Office of the Comptroller of the Currency (OCC), Comptroller's Handbook — Merchant Processing: U.S. bank-regulator guidance noting that card payment-related merchant processing is separate from card issuing.

- Stripe — How payment transaction processing works: public explanation of payment processing, including payment information transfer, authorization, clearing, settlement, and processor responsibilities.

Blog article footer

Subscribe to the HaiPay Blog

Stay connected with HaiPay and receive new blog posts in your inbox.

Like this post? Join our team.

HaiPay builds financial tools and economic infrastructure for the internet.