Merchant Account vs Payment Gateway: Do You Need Both?

Reviewed by Yuanqiang Wu

Last updated: July 21st, 2026

Insights

- A payment gateway captures your customer's card details at checkout; a merchant account is the bank account that receives the funds once a payment is approved. - To accept card payments you need both functions — but many providers bundle them, so you may never open your own merchant account. - You either operate as a sub-merchant under an all-in-one provider's account, or run your own merchant account via an acquirer — a trade-off between speed and control. - Not sure which you have? Check how your funds settle and how you signed up.

A payment gateway and a merchant account do two different jobs — and to accept card payments you generally need both. A payment gateway is the software at checkout that captures your customer's card details and securely sends them off to be authorized. A merchant account is the specialized bank account that receives the card funds once a payment is approved, before they're paid out to your everyday business bank account. The gateway is the front door; the merchant account is where the money lands. The catch that confuses most people: many providers bundle both, so you may never set up your own merchant account at all.

This article zooms in on one comparison: the merchant account vs the payment gateway. For the full picture — acquiring banks, payment processors, payment facilitators, merchant accounts and gateways together — see our merchant acquiring guide. For the closely related question of who settles your funds, see merchant acquirer vs payment processor.

Merchant account vs payment gateway: the short answer

Merchant account | Payment gateway | |

|---|---|---|

What it is | A specialized bank account for card funds | Software / a checkout interface |

What it does | Receives and holds card funds before payout | Captures card details and transmits them for authorization |

Where it sits | The back end (after approval) | The front end (at checkout) |

Who provides it | An acquirer / acquiring bank | A gateway provider (often the same company) |

Holds your money? | Yes — temporarily, before payout | No — it moves data, not funds |

Do you set it up separately? | Only if you open your own; an all-in-one provider may include it | Yes, but often bundled with the account |

Plain-language label* | The "where the money lands" side | The "how the card data gets in" side |

* "Front-end data vs back-end funds" is a common way to frame the two; it's a useful mental model, not a strict legal definition. A simple analogy: the gateway is the cashier taking the card; the merchant account is the till the money goes into.

What a merchant account is

A merchant account is a specialized bank account that lets a business accept and hold funds from card transactions. It's opened for you by an acquirer (an acquiring bank or acquiring partner), and it's distinct from your ordinary business bank account.

- It receives your card funds. When a card payment is approved, the money lands in the merchant account first, then is paid out — usually minus fees — to your business bank account.

- It's tied to the acquiring relationship. Because the acquirer holds these funds and carries settlement and chargeback exposure, opening your own merchant account usually involves an application and underwriting (the acquirer vets your business).

- It is not a payment gateway. A merchant account doesn't capture card details or sit on your checkout page; it's the funds-holding role behind the scenes.

What a payment gateway is

A payment gateway is the technology that captures a customer's card details and securely transmits them so the payment can be authorized. Online, it's the checkout page or the embedded payment form; in person, the role is played by the card terminal.

- It captures and encrypts card data at the point of payment.

- It transmits that data to the processor and on through the payment chain for authorization, then relays back the approval or decline.

- It doesn't hold your money. The gateway moves payment information, not funds. The funds land in the merchant account.

How a merchant account and a payment gateway work together

In a single card payment, the two roles sit end to end:

- Capture — at checkout, the payment gateway collects the customer's card details and securely sends them on.

- Authorization — the details are routed (via the processor) to the customer's bank, which approves or declines the payment.

- Settlement — for approved payments, the funds move through the card-payment system and the acquirer deposits your net funds into your merchant account, which then pays out to your business bank account.

The gateway is most visible at the front (the checkout); the merchant account is where the money settles at the back — and the processor does the authorization in the middle (see payment gateway vs payment processor). Both functions are needed for a card payment to complete — but, as the next section explains, you may get both from a single provider.

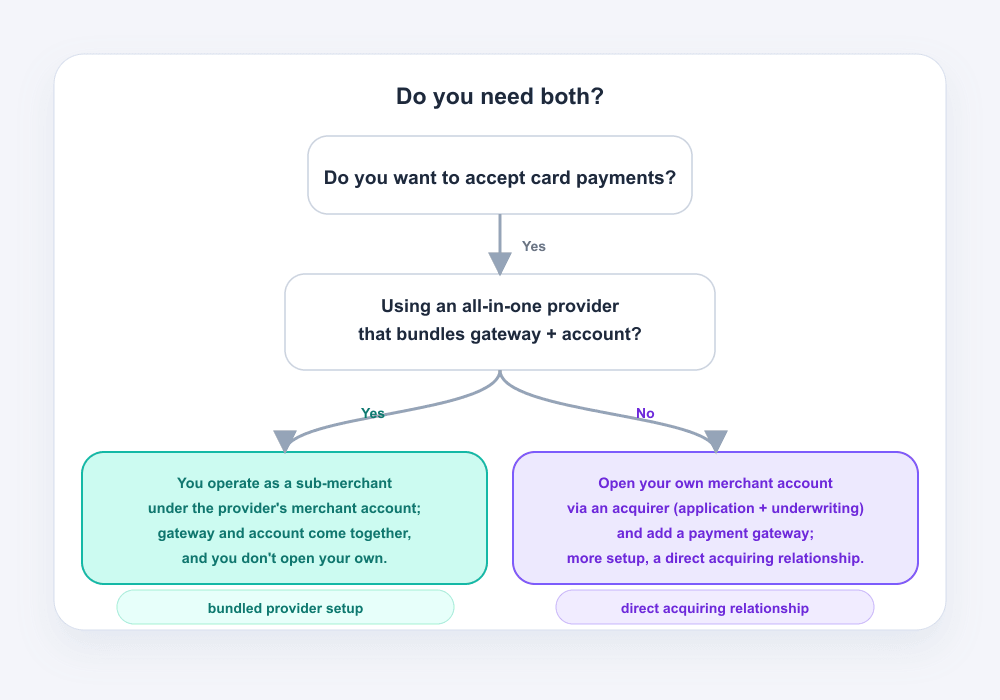

Do you need both? (an all-in-one provider vs your own merchant account)

Functionally, yes — accepting a card payment requires both a way to capture the card (a gateway) and a place for the funds to settle (a merchant account). What's optional is whether 你 set them up separately.

There are two common setups:

- All-in-one provider (you operate as a sub-merchant). Many modern providers bundle the gateway and the merchant-account function together. You sign up online, and you accept payments under the provider's own master merchant account rather than opening your own. You get the functionality of both without contracting them separately. This is the payment service provider (PSP) model — it's how the large platform payment providers are typically described.

- Your own merchant account + a gateway. You open a merchant account through an acquirer (with an application and underwriting) and pair it with a gateway. This is more setup, but it gives you a direct acquiring relationship.

Neither is "correct" universally — it's a trade-off between speed and simplicity on one side and control on the other (see "When the difference matters" below).

How to tell what you already have

If you're not sure whether you have your own merchant account or are operating under a provider's, three checks usually tell you — without needing the provider's internal details:

- How do your funds arrive? If a provider holds the money and pays you out a net amount on a schedule, you're typically operating under their merchant account. If funds settle into an account in your business's name that you set up via an acquirer, that's your own merchant account.

- How did you sign up? A few minutes online with no underwriting usually means you're a sub-merchant under the provider's master account. A separate application, underwriting, and an acquiring agreement usually means your own merchant account.

- Whose descriptor is involved? The billing descriptor and statements can hint at whether a provider sits between you and the acquirer — though this varies, so treat it as a clue, not proof.

If you can't tell from the marketing, ask the provider directly: "Do I have my own merchant account, or am I processing under yours as a sub-merchant?" The answer tells you which setup you're in.

When the difference matters — and when you can ignore it

Often, it doesn't matter. If you use one all-in-one provider, your volumes are straightforward, and you're happy with the payouts and pricing, you can treat "gateway" and "merchant account" as one box and move on.

It starts to matter when:

- You sell across borders. Where your transactions are acquired — and whether you have an acquiring setup in your customers' regions — can affect approval rates and cost, though the size of any effect depends on your markets, card mix and setup. This is an acquiring-relationship question, which is bound up with the merchant-account side, not the gateway.

- You want more control or better economics at scale. Your own merchant account gives you a direct acquiring relationship, which some businesses prefer as volumes grow.

- You want to change one part without the other. Knowing which provider owns the gateway vs the account is what lets you switch a gateway, or add local acquiring, without ripping everything out.

For the broader context — acquiring banks, processors, payment facilitators, and how merchant accounts and gateways fit the whole acquiring picture — the merchant acquiring guide covers it. This page deliberately stays on the one comparison.

Where HaiPay fits

HaiPay provides acquiring and cross-border payment services, and checkout tools to capture payments at the front end, for businesses that sell into multiple markets. If you're weighing a merchant account vs a payment gateway because you're setting up or expanding card payments internationally, both sides of that setup — where your funds are acquired and how your checkout captures them — are worth understanding clearly.

To see whether it fits your markets, explore HaiPay acquiring and HaiPay checkout, or talk to our team.

FAQ

What is the difference between a merchant account and a payment gateway? A payment gateway is the software that captures your customer's card details at checkout and sends them for authorization. A merchant account is the bank account that receives the card funds once a payment is approved, before they're paid out to your business bank account. The gateway handles the data; the merchant account holds the money.

Do I need a merchant account for a payment gateway? To accept card payments you need both functions — a gateway to capture the card and a merchant account for the funds to settle into. But you don't always open your own merchant account: many all-in-one providers let you process under their master merchant account as a sub-merchant, so the gateway and the account come together in one signup.

What are the disadvantages of a merchant account? Opening your own merchant account usually means more setup than an all-in-one signup: an application and underwriting, possible account or monthly fees, and, for some higher-risk businesses, possible reserves or holds on funds. The trade-off is a more direct acquiring relationship and more control. Whether those downsides matter depends on your volumes and how you sell.

What is a typical merchant account fee? There isn't a single standard figure. What you pay generally combines card-network and interchange costs with the acquirer's or provider's own markup, and can include fixed per-transaction and percentage components, plus possible account or monthly fees. Because it depends on your card mix, region, pricing model and provider, treat any quoted "typical" rate as a starting point and confirm the specifics with your provider.

Is a payment gateway the same as a merchant account? No. A payment gateway is software that captures and transmits card data; a merchant account is a bank account that holds the funds. They're complementary, and the provider of one may be a different company from the provider of the other — or the same provider may give you both.

Sources

- Wikipedia — Merchant account: defines a merchant account as a bank account that allows a business to accept card payments, established under an agreement with an acquiring bank, and notes the merchant account provider is typically a separate company from the payment gateway.

- Stripe — What is a merchant account vs. payment gateway?: public explanation defining each, the transaction flow, and that a provider can give merchant-account functionality without the business opening its own merchant account.

- Wise — Merchant Account vs. Payment Gateway: Do You Need Both?: defines each role and the "you need both" point, including the cashier/till analogy.

- PayPal — Merchant Accounts vs Payment Gateway: describes the merchant account as a bank account and the gateway as a software service, and that a provider can serve as both.

- PCI Security Standards Council — PCI DSS Glossary